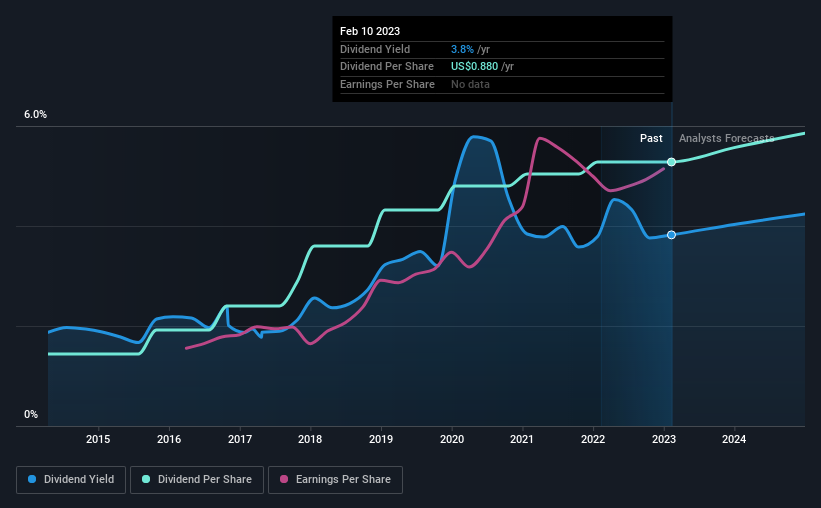

The board of Independent Bank Corporation (NASDAQ:IBCP) has announced that it will be increasing its dividend by 4.5% on the 24th of February to $0.23, up from last year's comparable payment of $0.22. This makes the dividend yield 3.8%, which is above the industry average.

Check out our latest analysis for Independent Bank

Independent Bank's Dividend Forecasted To Be Well Covered By Earnings

Impressive dividend yields are good, but this doesn't matter much if the payments can't be sustained.

Independent Bank has a good history of paying out dividends, with its current track record at 9 years. Taking data from its last earnings report, calculating for the company's payout ratio of 29%shows that Independent Bank would be able to pay its last dividend without pressure on the balance sheet.

Over the next 3 years, EPS is forecast to fall by 20.0%. Fortunately, analysts forecast the future payout ratio to be 37% over the same time horizon, which is in the range that makes us comfortable with the sustainability of the dividend.

Independent Bank Doesn't Have A Long Payment History

Independent Bank's dividend has been pretty stable for a little while now, but we will continue to be cautious until it has been demonstrated for a few more years. Since 2014, the annual payment back then was $0.24, compared to the most recent full-year payment of $0.88. This means that it has been growing its distributions at 16% per annum over that time. The dividend has been growing rapidly, however with such a short payment history we can't know for sure if payment can continue to grow over the long term, so caution may be warranted.

The Dividend Looks Likely To Grow

Some investors will be chomping at the bit to buy some of the company's stock based on its dividend history. It's encouraging to see that Independent Bank has been growing its earnings per share at 26% a year over the past five years. A low payout ratio gives the company a lot of flexibility, and growing earnings also make it very easy for it to grow the dividend.

Independent Bank Looks Like A Great Dividend Stock

Overall, we think this could be an attractive income stock, and it is only getting better by paying a higher dividend this year. The company is generating plenty of cash, and the earnings also quite easily cover the distributions. We should point out that the earnings are expected to fall over the next 12 months, which won't be a problem if this doesn't become a trend, but could cause some turbulence in the next year. All in all, this checks a lot of the boxes we look for when choosing an income stock.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. However, there are other things to consider for investors when analysing stock performance. For example, we've identified 2 warning signs for Independent Bank (1 doesn't sit too well with us!) that you should be aware of before investing. Is Independent Bank not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:IBCP

Independent Bank

Operates as the bank holding company for Independent Bank that provides banking services in the United States.

Very undervalued with flawless balance sheet and pays a dividend.