- United States

- /

- Banks

- /

- NasdaqGS:FRME

Why You Might Be Interested In First Merchants Corporation (NASDAQ:FRME) For Its Upcoming Dividend

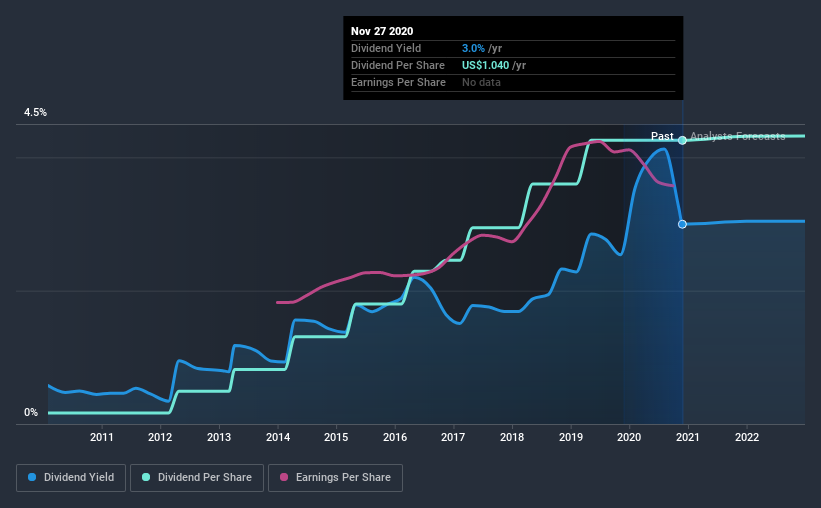

Readers hoping to buy First Merchants Corporation (NASDAQ:FRME) for its dividend will need to make their move shortly, as the stock is about to trade ex-dividend. Investors can purchase shares before the 3rd of December in order to be eligible for this dividend, which will be paid on the 18th of December.

First Merchants's next dividend payment will be US$0.26 per share. Last year, in total, the company distributed US$1.04 to shareholders. Based on the last year's worth of payments, First Merchants stock has a trailing yield of around 3.0% on the current share price of $34.71. If you buy this business for its dividend, you should have an idea of whether First Merchants's dividend is reliable and sustainable. As a result, readers should always check whether First Merchants has been able to grow its dividends, or if the dividend might be cut.

See our latest analysis for First Merchants

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. Fortunately First Merchants's payout ratio is modest, at just 37% of profit.

When a company paid out less in dividends than it earned in profit, this generally suggests its dividend is affordable. The lower the % of its profit that it pays out, the greater the margin of safety for the dividend if the business enters a downturn.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Stocks in companies that generate sustainable earnings growth often make the best dividend prospects, as it is easier to lift the dividend when earnings are rising. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. Fortunately for readers, First Merchants's earnings per share have been growing at 11% a year for the past five years.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. Since the start of our data, 10 years ago, First Merchants has lifted its dividend by approximately 39% a year on average. Both per-share earnings and dividends have both been growing rapidly in recent times, which is great to see.

To Sum It Up

Has First Merchants got what it takes to maintain its dividend payments? When companies are growing rapidly and retaining a majority of the profits within the business, it's usually a sign that reinvesting earnings creates more value than paying dividends to shareholders. This is one of the most attractive investment combinations under this analysis, as it can create substantial value for investors over the long run. First Merchants ticks a lot of boxes for us from a dividend perspective, and we think these characteristics should mark the company as deserving of further attention.

On that note, you'll want to research what risks First Merchants is facing. We've identified 2 warning signs with First Merchants (at least 1 which is a bit unpleasant), and understanding these should be part of your investment process.

If you're in the market for dividend stocks, we recommend checking our list of top dividend stocks with a greater than 2% yield and an upcoming dividend.

If you’re looking to trade First Merchants, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

If you're looking to trade First Merchants, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NasdaqGS:FRME

First Merchants

Operates as the financial holding company for First Merchants Bank that provides commercial and consumer banking services.

Very undervalued with flawless balance sheet and pays a dividend.

Market Insights

Community Narratives