- United States

- /

- Banks

- /

- NasdaqCM:EGBN

Eagle Bancorp, Inc. Just Beat EPS By 64%: Here's What Analysts Think Will Happen Next

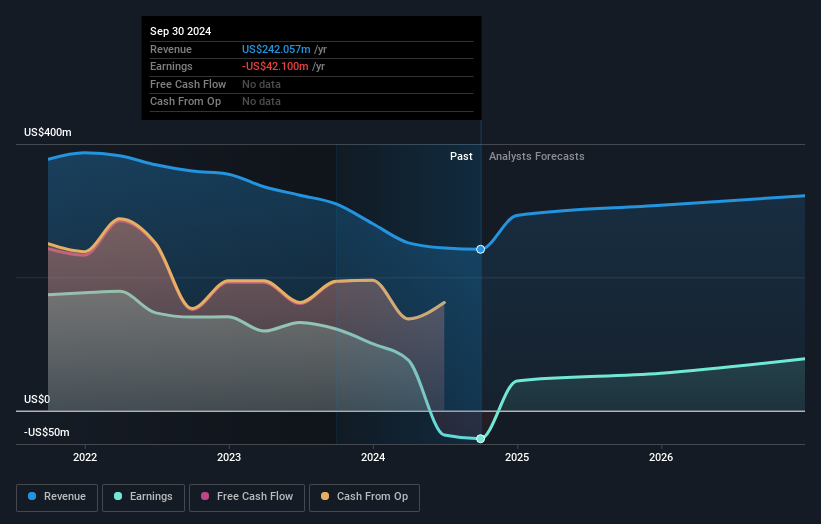

Investors in Eagle Bancorp, Inc. (NASDAQ:EGBN) had a good week, as its shares rose 7.0% to close at US$26.17 following the release of its quarterly results. Revenues of US$72m fell slightly short of expectations, but earnings were a definite bright spot, with statutory per-share profits of US$0.72 an impressive 64% ahead of estimates. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

See our latest analysis for Eagle Bancorp

Taking into account the latest results, the most recent consensus for Eagle Bancorp from three analysts is for revenues of US$308.0m in 2025. If met, it would imply a sizeable 27% increase on its revenue over the past 12 months. Eagle Bancorp is also expected to turn profitable, with statutory earnings of US$2.24 per share. In the lead-up to this report, the analysts had been modelling revenues of US$311.1m and earnings per share (EPS) of US$1.85 in 2025. Although the revenue estimates have not really changed, we can see there's been a considerable lift to earnings per share expectations, suggesting that the analysts have become more bullish after the latest result.

The consensus price target rose 8.7% to US$25.00, suggesting that higher earnings estimates flow through to the stock's valuation as well. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. The most optimistic Eagle Bancorp analyst has a price target of US$29.00 per share, while the most pessimistic values it at US$22.00. Even so, with a relatively close grouping of estimates, it looks like the analysts are quite confident in their valuations, suggesting Eagle Bancorp is an easy business to forecast or the the analysts are all using similar assumptions.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. One thing stands out from these estimates, which is that Eagle Bancorp is forecast to grow faster in the future than it has in the past, with revenues expected to display 21% annualised growth until the end of 2025. If achieved, this would be a much better result than the 4.4% annual decline over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in the industry are forecast to see their revenue grow 6.7% per year. So it looks like Eagle Bancorp is expected to grow faster than its competitors, at least for a while.

The Bottom Line

The biggest takeaway for us is the consensus earnings per share upgrade, which suggests a clear improvement in sentiment around Eagle Bancorp's earnings potential next year. Happily, there were no major changes to revenue forecasts, with the business still expected to grow faster than the wider industry. We note an upgrade to the price target, suggesting that the analysts believes the intrinsic value of the business is likely to improve over time.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. We have forecasts for Eagle Bancorp going out to 2026, and you can see them free on our platform here.

You still need to take note of risks, for example - Eagle Bancorp has 1 warning sign we think you should be aware of.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Eagle Bancorp might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:EGBN

Eagle Bancorp

Operates as the bank holding company for EagleBank that provides commercial and consumer banking services primarily in the United States.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Hitit Bilgisayar Hizmetleri will achieve a 19.7% revenue boost in the next five years

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)