Advertisement

- United States

- /

- Auto

- /

- NYSE:NIO

Is NIO Stock a Bargain After Its 88.6% Five Year Slide?

Simply Wall St

Reviewed by Bailey Pemberton

- If you are wondering whether NIO at around $5 a share is a bargain in disguise or a value trap, you are not alone. This is exactly the question we are going to unpack.

- The stock is up 10.5% year to date and 9.3% over the past year, but those gains come after a steep slide of 32.2% over the last month and a bruising 88.6% drop over five years.

- Recent headlines have focused on NIO's ongoing push to expand its EV lineup and ecosystem, as well as its efforts to shore up its balance sheet and secure strategic partnerships in a fiercely competitive Chinese EV market. Together, these developments have fueled shifting expectations around the company’s growth prospects and risk profile, which helps explain the stock’s sharp swings.

- Our initial valuation checks give NIO a 3/6 value score. This suggests there are some signs of undervaluation but also clear red flags. We will break these down using multiple valuation methods, before ending with a more intuitive way to think about what the market might really be pricing in.

Find out why NIO's 9.3% return over the last year is lagging behind its peers.

Approach 1: NIO Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth by projecting the cash it can generate in the future and then discounting those cash flows back to today’s value. For NIO, the model used is a 2 Stage Free Cash Flow to Equity approach, built in CN¥.

NIO’s latest twelve month free cash flow is deeply negative at roughly CN¥19.7 billion, highlighting how cash hungry the business still is. Analysts expect free cash flow to improve over the next few years and Simply Wall St then extrapolates those forecasts further out, with projections rising to around CN¥21.2 billion by 2035. This path includes years of both negative and positive cash flow as the business scales.

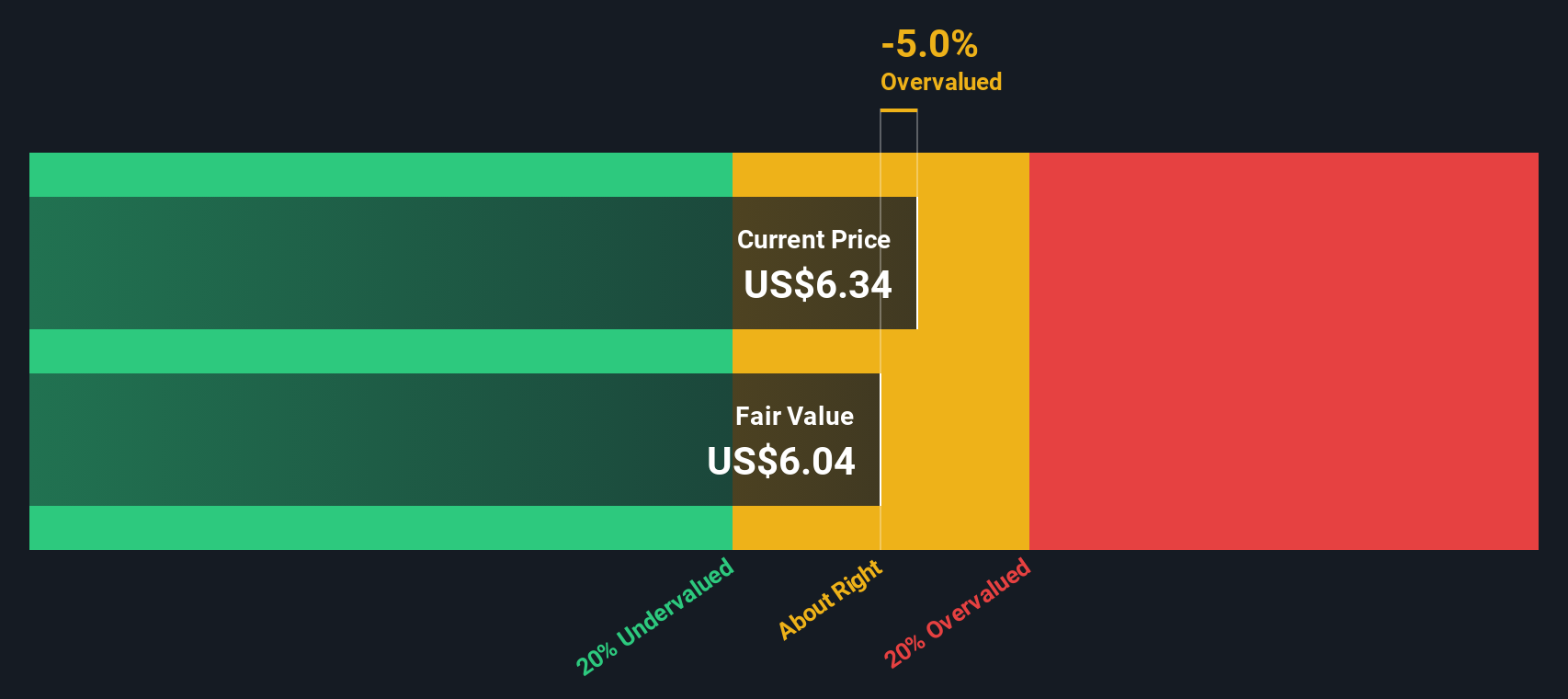

When these projected cash flows are discounted back, the model arrives at an intrinsic value of about $6.95 per share. Compared with the current market price near $5, this implies NIO is around 27.6% undervalued. This suggests investors are being compensated for taking on execution and funding risk.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests NIO is undervalued by 27.6%. Track this in your watchlist or portfolio, or discover 925 more undervalued stocks based on cash flows.

Approach 2: NIO Price vs Sales

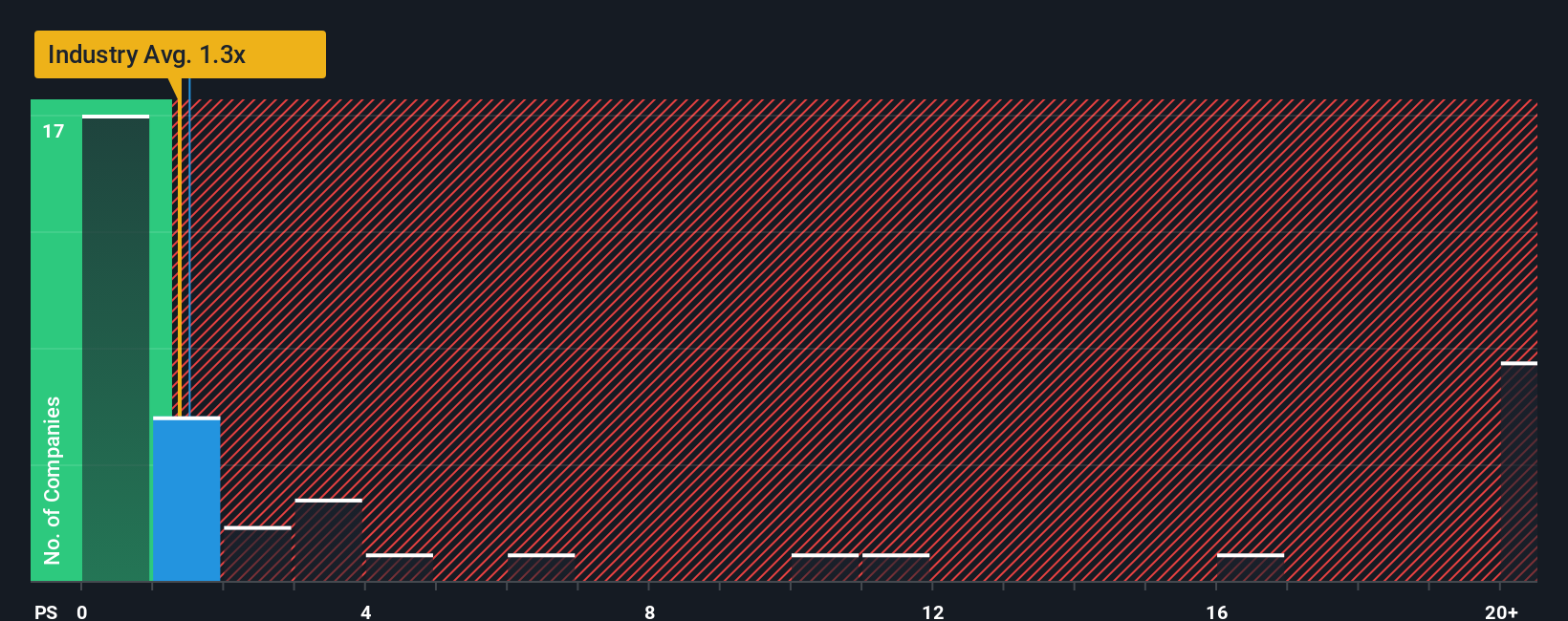

Price to Sales is a useful yardstick for growth oriented or unprofitable companies because it values the business on the revenue it is already generating, rather than earnings that can swing with heavy investment and accounting charges. For fast growing, higher risk names like NIO, investors typically accept a higher multiple if they believe strong top line growth will eventually translate into sustainable profits.

NIO currently trades on a Price to Sales ratio of about 1.21x, which sits above the Auto industry average of roughly 0.89x but below the peer group average of around 1.76x. Simply Wall St’s proprietary Fair Ratio for NIO, which blends in factors like its growth outlook, profit margins, industry, market cap and risk profile, sits at about 1.11x. This Fair Ratio is more informative than a simple peer or industry comparison because it is tailored to NIO’s specific fundamentals rather than assuming all EV makers deserve the same multiple.

Comparing NIO’s actual 1.21x Price to Sales with the 1.11x Fair Ratio suggests the stock is modestly expensive on this metric, but not by a wide margin.

Result: OVERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1441 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your NIO Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. This is a simple tool on Simply Wall St’s Community page that lets you attach your own story about NIO’s future to the numbers by linking what you believe about its revenue growth, margins and execution to a concrete forecast and Fair Value. You can then compare that Fair Value to today’s share price to consider whether to buy, hold or sell, while the platform keeps your Narrative updated automatically as new news or earnings arrive.

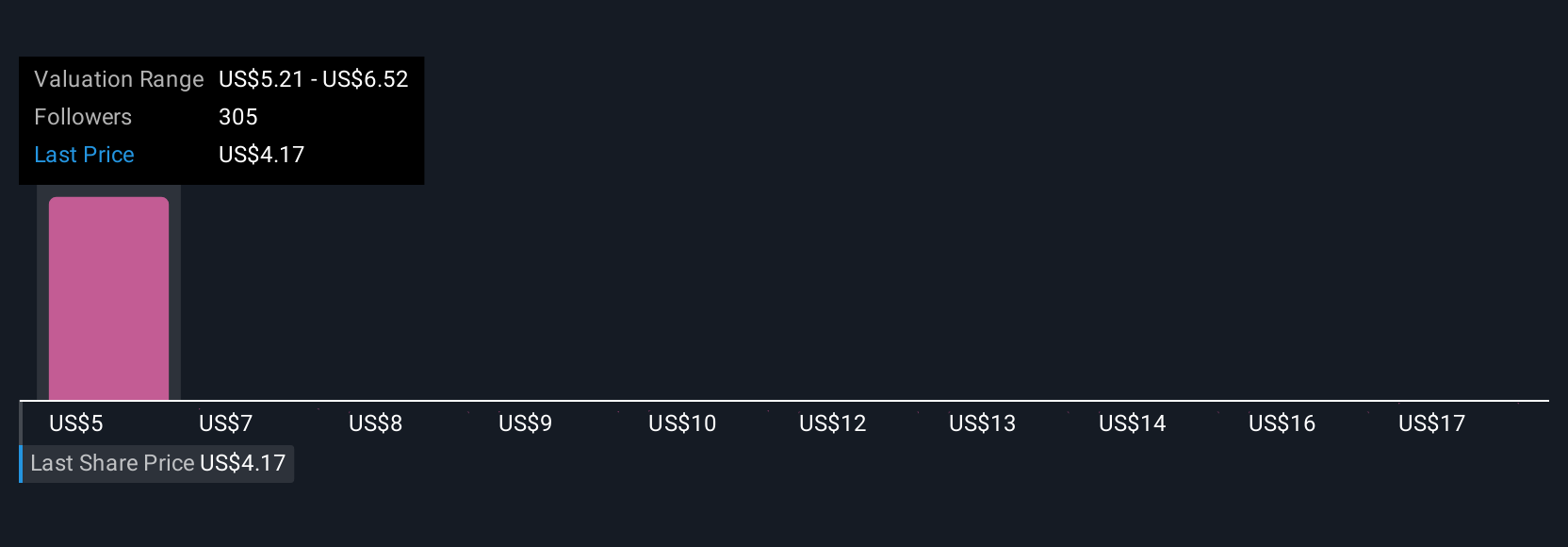

For example, a bullish investor might build a Narrative where NIO’s premium brand, battery swap network and multi brand strategy support revenue growth above 30% a year, margins near 6%, and a Fair Value closer to the most optimistic analyst target around $9. A more cautious investor might create a Narrative that assumes slower growth, thinner margins closer to 5%, and a Fair Value nearer the most pessimistic target around $3. Both perspectives can coexist side by side so you can quickly see which story, and which valuation, feels more realistic to you.

Do you think there's more to the story for NIO? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if NIO might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:NIO

NIO

Designs, develops, manufactures, and sells smart electric vehicles in China, Europe, and internationally.

High growth potential and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

18 followersusers have followed this narrative

5 commentsusers have commented on this narrative

5 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.1% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

MA

MarkoVT on Alphabet ·

Positioned globally, partnered locally

Fair Value:US$390.1919.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

JohnJ on Worldline ·

When will fraudsters be investigated in depth. Fraud was ongoing in France too.

Fair Value:€0.5200.8% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Applied Digital ·

Staggered by dilution; positions for growth

Fair Value:US$35.4520.9% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

112 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.5% undervalued

948 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.1% undervalued

148 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative