Advertisement

- United States

- /

- Auto

- /

- NasdaqGM:PSNY

Polestar (PSNY) Is Down 9.0% After Reporting 13% Third Quarter Sales Growth – What's Changed

Simply Wall St

Reviewed by Sasha Jovanovic

- Polestar announced that retail sales for the third quarter of 2025 reached an estimated 14,192 cars, marking a 13% increase compared to the same period in 2024, with sales for the first nine months totaling approximately 44,482 cars, up 36% year over year.

- This sales growth underscores strong consumer demand and hints at Polestar’s operational momentum within a rapidly evolving electric vehicle landscape.

- We'll explore how robust retail sales growth in the past quarter could reshape Polestar's investment narrative and future guidance.

The end of cancer? These 28 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

Polestar Automotive Holding UK Investment Narrative Recap

To be a shareholder in Polestar Automotive, you need to believe that rapid consumer adoption of electric vehicles and expansion into new markets will allow the company to grow sales volumes fast enough to offset ongoing losses and operational challenges. The recent announcement of a 13% increase in Q3 2025 retail sales is encouraging, but it does not address the company’s biggest near-term risk: persistent unprofitability and a short cash runway. In the short term, these results may build confidence ahead of upcoming quarterly earnings, but their effect on the profit outlook appears limited.

Of recent announcements, the most relevant is Polestar’s upcoming Q3 2025 results release on November 12. This event will see the company provide more color on margins, cash position, and forward guidance, which are key short-term catalysts for investor sentiment and for evaluating whether sales momentum translates to financial improvements. With increasing retail sales reported, many investors will be looking to this earnings release for signs that cost reductions and efficiency gains are supporting a path to profitability.

By contrast, investors should be mindful that solid sales growth does not always resolve underlying concerns about...

Read the full narrative on Polestar Automotive Holding UK (it's free!)

Polestar Automotive Holding UK's outlook anticipates $11.0 billion in revenue and $559.6 million in earnings by 2028. This outcome is based on an annual revenue growth rate of 63.1% and a $3.26 billion improvement in earnings from current earnings of -$2.7 billion.

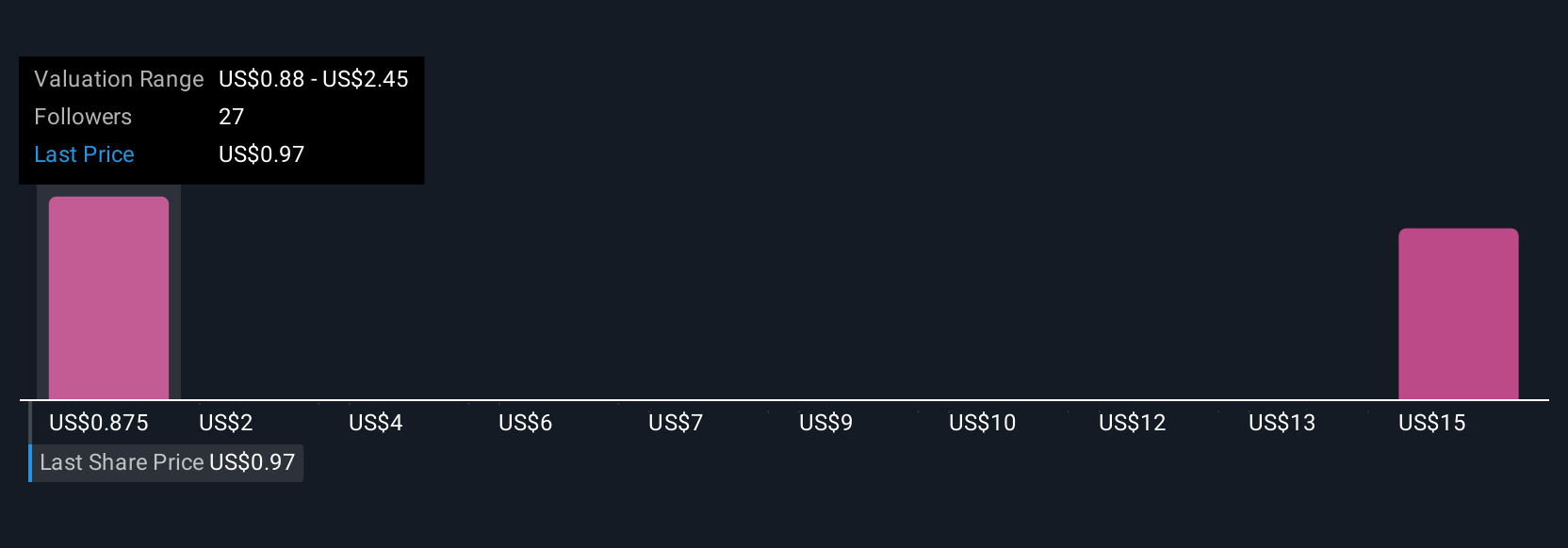

Uncover how Polestar Automotive Holding UK's forecasts yield a $1.00 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Nine members of the Simply Wall St Community believe Polestar's fair value lies between US$1.00 and US$16.60 per share. With unprofitability persisting despite recent sales growth, these differing views signal a broad range of expectations for the business, see how others are weighing the upside and risks.

Explore 9 other fair value estimates on Polestar Automotive Holding UK - why the stock might be a potential multi-bagger!

Build Your Own Polestar Automotive Holding UK Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Polestar Automotive Holding UK research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

- Our free Polestar Automotive Holding UK research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Polestar Automotive Holding UK's overall financial health at a glance.

Ready For A Different Approach?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- These 10 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGM:PSNY

Polestar Automotive Holding UK

Engages in the research and development, marketing, commercialization, and sale of battery electric vehicles and related technology solutions.

Low risk and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|10.9% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|12.0% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor