Advertisement

- United States

- /

- Auto

- /

- NasdaqGS:LCID

Lucid Group (LCID): Assessing Valuation After Record Q3 Deliveries Miss Wall Street Targets and Forecast Narrows

Simply Wall St

Reviewed by Kshitija Bhandaru

Lucid Group (LCID) just posted record third-quarter deliveries, coming in higher than last year but slightly below what investors were hoping for. A wave of buyers rushed to beat the expiring federal EV tax credit, which added an extra boost.

See our latest analysis for Lucid Group.

Even with Lucid’s record Q3 deliveries and a high-profile robotaxi partnership, shares have been volatile. After a recent bump, the share price is now down about 31% year-to-date and the one-year total shareholder return sits at -38%, reflecting persistent worries about demand and production targets as federal incentives wane. Momentum has faded considerably from last year, with ongoing challenges putting longer-term growth potential under the spotlight.

If Lucid’s wild ride has you rethinking your own watchlist, now might be the perfect moment to explore See the full list for free.

After such a turbulent stretch, does Lucid’s recent selloff present a clear buying opportunity for value-seeking investors, or is the market already factoring in all the company’s risks and future growth prospects?

Most Popular Narrative: 11.8% Undervalued

Lucid’s fair value, as estimated by the most popular narrative, sits at $23.79, which is higher than the last close of $20.98. This hints at unrealized potential if key strategic moves bear fruit.

The newly announced Uber and Nuro partnership, including a planned $300 million Uber investment and a commitment to deploy at least 20,000 Lucid Gravity vehicles as robotaxis over six years, is expected to open a large and fast-growing autonomous fleet market to Lucid, driving significant revenue expansion and potential margin improvement via technology licensing and high-volume fleet sales.

Want the full playbook? This narrative builds its bullish stance on aggressive expansion, vertical integration, and a bold shift in Lucid’s business model. The underlying financial assumptions could surprise you. Peek inside to discover how projections for rapid scaling and premium positioning form the core of this value thesis.

Result: Fair Value of $23.79 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent negative gross margins and ongoing dilution risk from capital raises could quickly undermine the narrative, especially if manufacturing or demand challenges become more severe.

Find out about the key risks to this Lucid Group narrative.

Another View: Looking at Sales Ratios

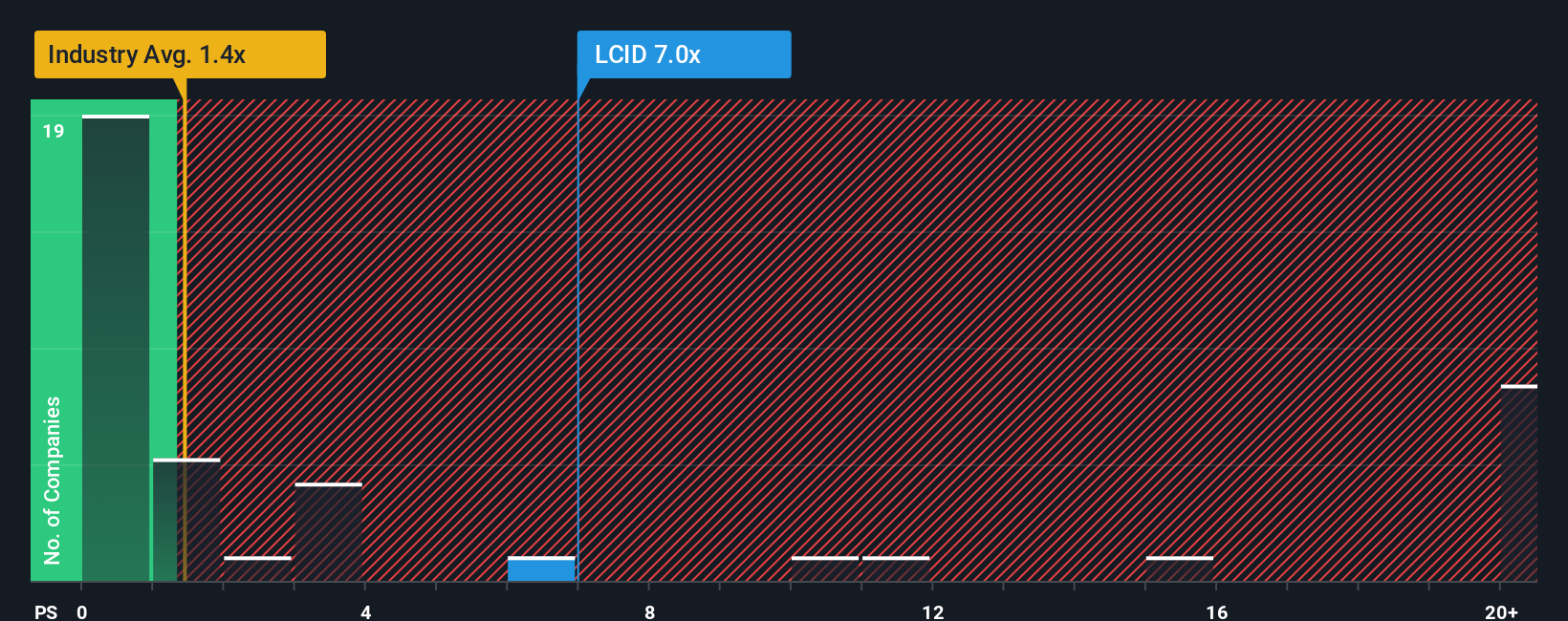

While analyst narratives point to upside, the actual price-to-sales ratio may raise eyebrows. Lucid trades at 6.9 times sales, which is far steeper than the US Auto industry average of 1.3 and the peer average of 2. This premium leaves little room for error, especially since the fair ratio could be as low as 0.1. Does the market believe Lucid's growth story, or is it setting up high expectations?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Lucid Group Narrative

If you think the numbers tell a different story, or want to dive in and craft your own perspective, you can build a narrative in just a few minutes: Do it your way

A great starting point for your Lucid Group research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

Looking for More Smart Investment Ideas?

Don’t let your next opportunity pass you by. Get ahead of the curve and spot companies that fit your strategy using these specialized lists:

- Spot unique growth opportunities by checking out these 24 AI penny stocks with the potential to shape the future through artificial intelligence innovation.

- Tap into regular income streams and strong yields by scanning these 19 dividend stocks with yields > 3% offering compelling dividend potential above 3%.

- Capitalize on fast-moving opportunities by reviewing these 3585 penny stocks with strong financials combining solid fundamentals with the agility to outperform in today’s volatile market.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:LCID

Lucid Group

A technology company, designs, engineers, manufactures, and sells electric vehicles (EV), EV powertrains, and battery systems.

Flawless balance sheet with low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|10.9% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|12.0% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor