- Taiwan

- /

- Electronic Equipment and Components

- /

- TWSE:2360

High Growth Tech Stocks To Watch For Potential Portfolio Boost

Reviewed by Simply Wall St

Amidst a backdrop of mixed global market performance, the Nasdaq Composite has reached a new milestone, driven by gains in technology stocks, while small-cap indices like the Russell 2000 have struggled to keep pace with larger counterparts. In this environment of shifting economic indicators and anticipated interest rate adjustments, identifying high-growth tech stocks can be crucial for investors seeking potential portfolio enhancement.

Top 10 High Growth Tech Companies

| Name | Revenue Growth | Earnings Growth | Growth Rating |

|---|---|---|---|

| Yggdrazil Group | 30.20% | 87.10% | ★★★★★★ |

| Seojin SystemLtd | 35.41% | 39.86% | ★★★★★★ |

| eWeLLLtd | 27.24% | 28.74% | ★★★★★★ |

| Ascelia Pharma | 76.15% | 47.16% | ★★★★★★ |

| Mental Health TechnologiesLtd | 25.83% | 113.12% | ★★★★★★ |

| Pharma Mar | 25.43% | 56.19% | ★★★★★★ |

| Fine M-TecLTD | 36.52% | 131.08% | ★★★★★★ |

| Alkami Technology | 21.94% | 98.60% | ★★★★★★ |

| JNTC | 29.48% | 104.37% | ★★★★★★ |

| Travere Therapeutics | 31.70% | 72.51% | ★★★★★★ |

Click here to see the full list of 1287 stocks from our High Growth Tech and AI Stocks screener.

Underneath we present a selection of stocks filtered out by our screen.

Shenzhen Fortune Trend technology (SHSE:688318)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shenzhen Fortune Trend Technology Co., Ltd. operates in the technology sector and has a market capitalization of CN¥33.88 billion.

Operations: Fortune Trend Technology focuses on providing comprehensive software solutions and services, primarily targeting the financial industry. Its revenue streams are largely driven by its software licensing and maintenance services. The company has demonstrated a gross profit margin of 60%, reflecting its ability to effectively manage costs relative to revenue generation.

Shenzhen Fortune Trend Technology, amidst a challenging year with a 15.4% drop in revenue to CNY 210.28 million, still showcases resilience with notable R&D commitments and an aggressive growth forecast. The company's R&D expenses are pivotal, reflecting its drive for innovation despite short-term earnings pressures—evident from the recent earnings results where net income slid to CNY 144.01 million from CNY 198.18 million previously. Looking ahead, Shenzhen Fortune Trend is poised for recovery with expected annual revenue and earnings growth rates of 34.9% and 39.2%, respectively, outpacing the broader Chinese market projections of 13.7% and 25.8%. This robust outlook is anchored in strategic expansions and technological advancements that could redefine its market standing.

Bitfarms (TSX:BITF)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Bitfarms Ltd. is involved in cryptocurrency mining operations across Canada, the United States, Paraguay, and Argentina, with a market cap of CA$1.30 billion.

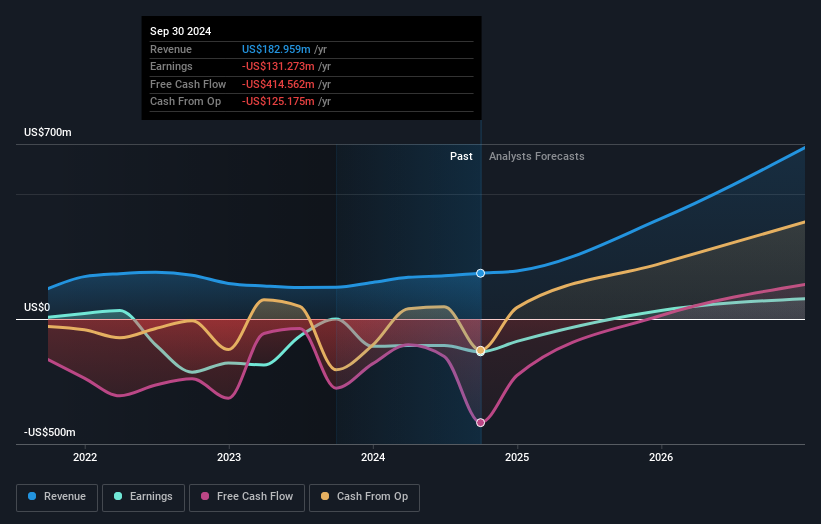

Operations: Bitfarms Ltd. generates revenue primarily through cryptocurrency mining, with reported earnings of $182.96 million from this segment. The company operates across several countries, leveraging its infrastructure to mine digital currencies efficiently.

Bitfarms, navigating through a volatile market, reported a significant uptick in revenue growth at 58.9% annually, outpacing the Canadian market's average of 7.5%. Despite current unprofitability, projections indicate an impressive earnings surge of 121.75% per year as the firm strides towards profitability within three years. This growth trajectory is underpinned by strategic R&D investments which are crucial for sustaining innovation and competitiveness in the rapidly evolving tech landscape. Recent operational adjustments include a new miner hosting agreement with Stronghold Digital Mining Hosting, reflecting proactive management in optimizing resource allocation and enhancing operational efficiency amidst challenging conditions.

- Click here and access our complete health analysis report to understand the dynamics of Bitfarms.

Gain insights into Bitfarms' past trends and performance with our Past report.

Chroma ATE (TWSE:2360)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Chroma ATE Inc. is involved in the design, assembly, manufacturing, sales, repair, and maintenance of software/hardware for computers and peripherals as well as computerized automatic test systems and electronic test instruments across Taiwan, China, the United States, and other international markets with a market capitalization of NT$171.59 billion.

Operations: Chroma ATE generates revenue primarily from its Measuring Instruments Business, which accounts for NT$30.84 billion, and Automated Transport Engineering, contributing NT$1.69 billion. The company operates in various international markets including Taiwan, China, and the United States.

Chroma ATE has demonstrated robust financial performance with a 16.3% annual revenue growth, outpacing the TW market's average of 12.1%. This growth is supported by significant R&D investments, which accounted for a substantial portion of their revenue, aligning with their strategic focus on innovation and market expansion in electronic testing solutions. The company's recent presentations at major global conferences underscore its proactive approach to capturing emerging tech trends and expanding its industry footprint. With earnings projected to surge by 24.9% annually, Chroma ATE is strategically positioned to leverage its technological advancements and strong market presence for sustained growth.

- Click here to discover the nuances of Chroma ATE with our detailed analytical health report.

Explore historical data to track Chroma ATE's performance over time in our Past section.

Make It Happen

- Get an in-depth perspective on all 1287 High Growth Tech and AI Stocks by using our screener here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:2360

Chroma ATE

Designs, assembles, manufactures, sells, repairs, and maintains software/hardware for computers and peripherals, computerized automatic test systems, electronic test instruments, signal generators, power supplies, and telecom power supplies in Taiwan, China, the United States, and internationally.

Flawless balance sheet with high growth potential.