- Taiwan

- /

- Electronic Equipment and Components

- /

- TWSE:2360

3 Growth Companies Insiders Are Banking On

Reviewed by Simply Wall St

As global markets navigate a landscape of easing core inflation and strong bank earnings, major U.S. stock indexes have rebounded, with value stocks notably outperforming growth shares. In this environment, insider ownership in growth companies can signal confidence from those who know the business best, making them intriguing prospects for investors looking to capitalize on potential market opportunities.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Duc Giang Chemicals Group (HOSE:DGC) | 31.4% | 23.8% |

| Kirloskar Pneumatic (BSE:505283) | 30.3% | 26.3% |

| Seojin SystemLtd (KOSDAQ:A178320) | 30.9% | 39.9% |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 41.2% |

| Clinuvel Pharmaceuticals (ASX:CUV) | 10.4% | 26.2% |

| SKS Technologies Group (ASX:SKS) | 29.7% | 24.8% |

| Brightstar Resources (ASX:BTR) | 16.2% | 84.3% |

| Fine M-TecLTD (KOSDAQ:A441270) | 17.2% | 135% |

| Fulin Precision (SZSE:300432) | 13.6% | 71% |

| Findi (ASX:FND) | 35.8% | 110.7% |

Here's a peek at a few of the choices from the screener.

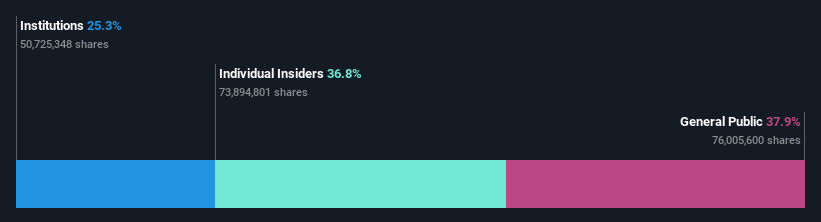

Pansoft (SZSE:300996)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Pansoft Company Limited offers enterprise management information solutions and IT integrated services in China, with a market cap of CN¥3.45 billion.

Operations: The company's revenue segments include enterprise management information solutions and IT integrated services in China.

Insider Ownership: 38.7%

Earnings Growth Forecast: 27.8% p.a.

Pansoft demonstrates strong growth potential with expected revenue and earnings growth rates of 22.2% and 27.8% annually, respectively, outpacing both industry and market averages in China. Recent amendments to the company's articles of association suggest proactive governance adjustments to support this growth trajectory. Despite a low forecasted return on equity of 13.1%, Pansoft's price-to-earnings ratio of 38.3x remains attractive compared to the software industry's higher average, indicating potential value for investors seeking growth opportunities with substantial insider ownership influence.

- Click here and access our complete growth analysis report to understand the dynamics of Pansoft.

- Our comprehensive valuation report raises the possibility that Pansoft is priced higher than what may be justified by its financials.

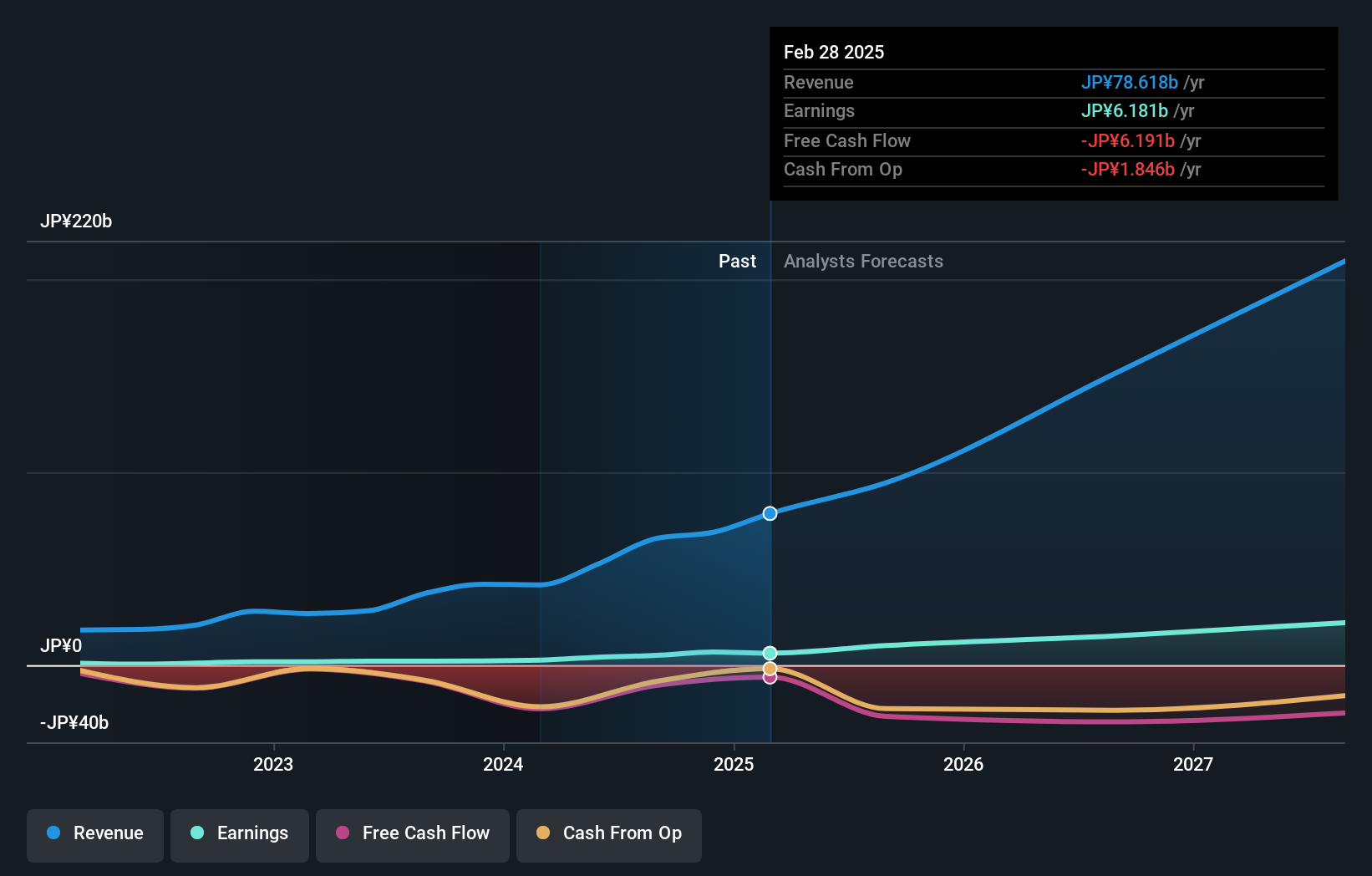

Kasumigaseki CapitalLtd (TSE:3498)

Simply Wall St Growth Rating: ★★★★★★

Overview: Kasumigaseki Capital Co., Ltd. operates in the real estate consulting sector in Japan and has a market capitalization of ¥146.23 billion.

Operations: Kasumigaseki Capital Co., Ltd.'s revenue is derived from its operations in the real estate consulting sector within Japan.

Insider Ownership: 33.8%

Earnings Growth Forecast: 33.5% p.a.

Kasumigaseki Capital Ltd. is poised for significant growth, with earnings projected to increase by 33.5% annually, outpacing the broader Japanese market's 8.1%. Revenue growth is also strong at 30.4%, surpassing market expectations of 4.3%. However, despite these promising forecasts, the company's debt coverage by operating cash flow remains a concern and its share price has been highly volatile recently. Upcoming Q1 results on January 14 may provide further insights into its financial trajectory.

- Dive into the specifics of Kasumigaseki CapitalLtd here with our thorough growth forecast report.

- Upon reviewing our latest valuation report, Kasumigaseki CapitalLtd's share price might be too optimistic.

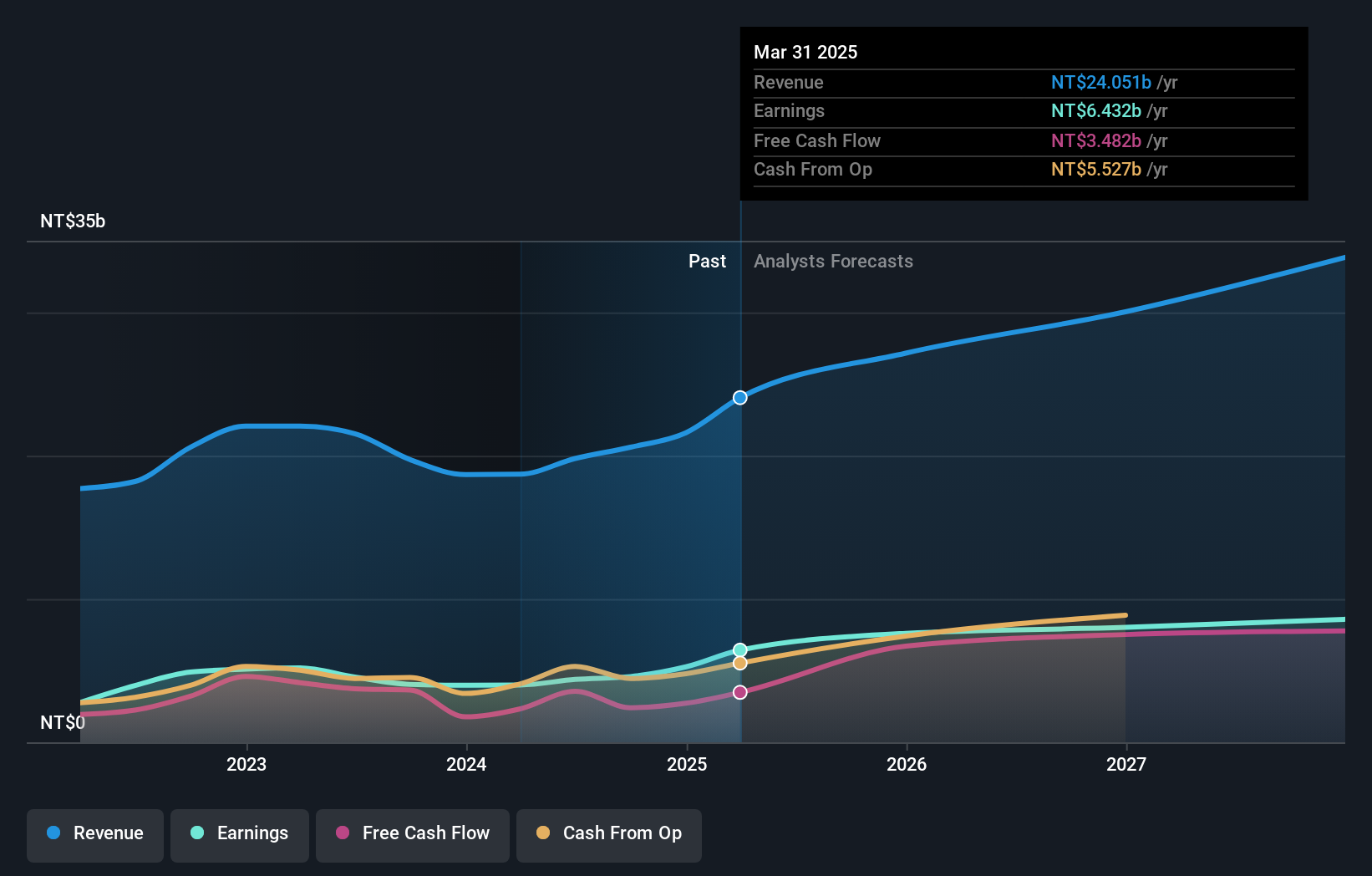

Chroma ATE (TWSE:2360)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Chroma ATE Inc. is engaged in the design, assembly, manufacturing, sales, repair, and maintenance of software/hardware for computers and peripherals as well as various electronic testing systems and instruments across Taiwan, China, the United States, and internationally with a market cap of NT$157.60 billion.

Operations: The company's revenue segments include NT$30.84 billion from the Measuring Instruments Business and NT$1.69 billion from Automated Transport Engineering.

Insider Ownership: 14.5%

Earnings Growth Forecast: 26.7% p.a.

Chroma ATE is experiencing robust growth, with earnings forecasted to rise significantly at 26.7% annually, outpacing the Taiwanese market's 17.3%. Revenue is expected to grow at a solid rate of 17.1% per year, though below the 20% benchmark for high growth. The stock trades at a substantial discount to its estimated fair value and analysts predict a potential price increase of 22.3%. Recent earnings showed strong performance with increased revenue and net income figures.

- Delve into the full analysis future growth report here for a deeper understanding of Chroma ATE.

- The analysis detailed in our Chroma ATE valuation report hints at an deflated share price compared to its estimated value.

Key Takeaways

- Click this link to deep-dive into the 1466 companies within our Fast Growing Companies With High Insider Ownership screener.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:2360

Chroma ATE

Designs, assembles, manufactures, sells, repairs, and maintains software/hardware for computers and peripherals, computerized automatic test systems, electronic test instruments, signal generators, power supplies, and telecom power supplies in Taiwan, China, the United States, and internationally.

Flawless balance sheet with high growth potential.