- Turkey

- /

- Capital Markets

- /

- IBSE:OYYAT

Uncovering None And Two Other Promising Small Caps For Your Portfolio

Reviewed by Simply Wall St

In a week where the Nasdaq Composite reached a new milestone while most other major indices, including the Russell 2000, saw declines, small-cap stocks have been under pressure amid broader economic uncertainties and rate cut expectations. As investors navigate these volatile conditions, identifying promising small-cap opportunities can be crucial for diversifying portfolios and potentially capitalizing on undervalued assets that may thrive despite market headwinds.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Sugar Terminals | NA | 3.14% | 3.53% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Citra Tubindo | NA | 11.06% | 31.01% | ★★★★★★ |

| Prima Andalan Mandiri | 0.94% | 20.24% | 15.28% | ★★★★★★ |

| Cardig Aero Services | NA | 6.60% | 69.79% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| CTCI Advanced Systems | 30.56% | 24.10% | 29.97% | ★★★★★☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Chongqing Machinery & Electric | 27.77% | 8.82% | 11.12% | ★★★★☆☆ |

| Bank MNC Internasional | 18.72% | 4.80% | 43.63% | ★★★★☆☆ |

Below we spotlight a couple of our favorites from our exclusive screener.

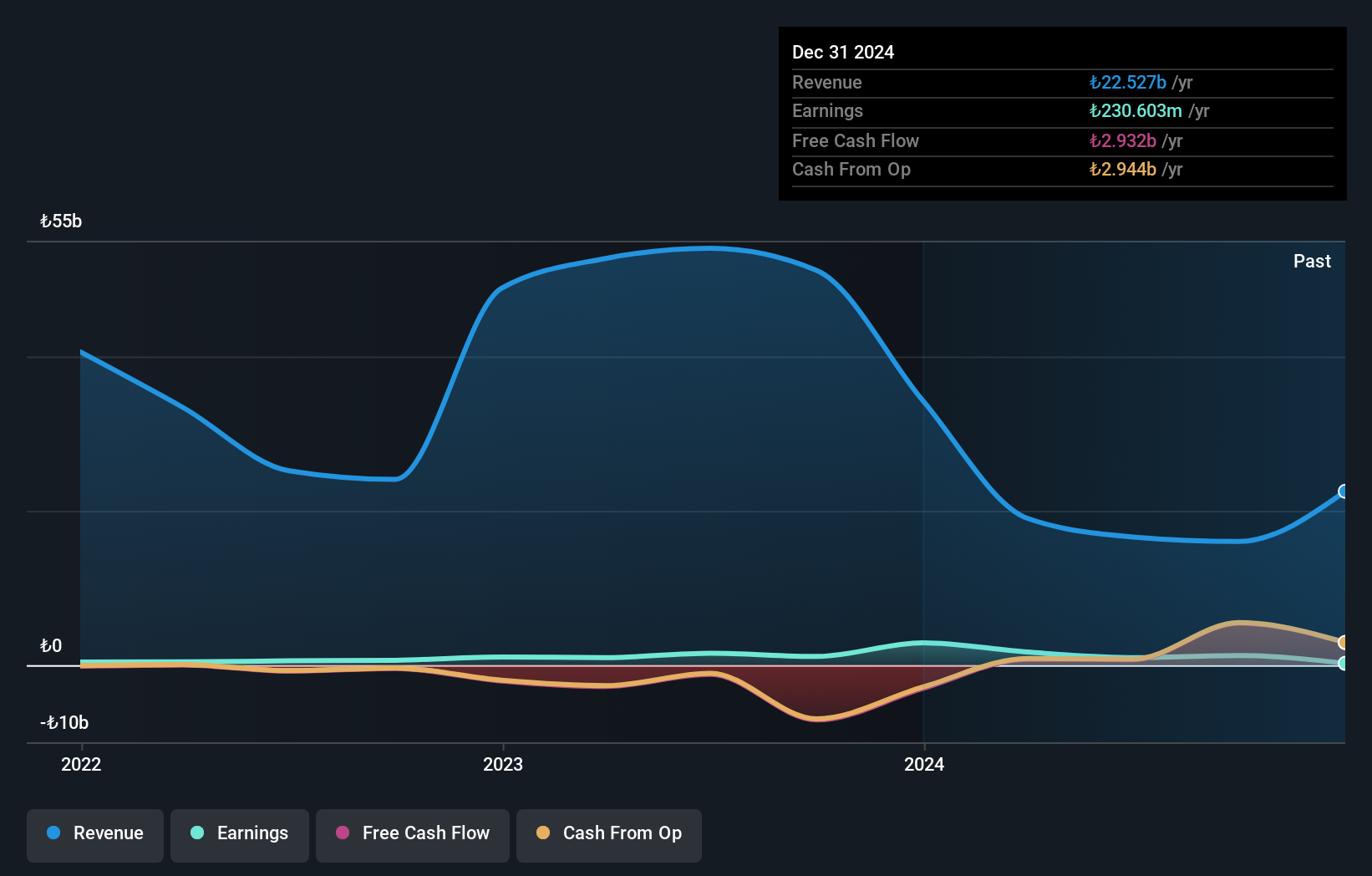

Oyak Yatirim Menkul Degerler (IBSE:OYYAT)

Simply Wall St Value Rating: ★★★★★☆

Overview: Oyak Yatirim Menkul Degerler A.S. offers research, brokerage, portfolio management, corporate finance, and fund operation services for capital market instruments in Turkey with a market cap of TRY10.19 billion.

Operations: Oyak Yatirim derives its revenue primarily from services related to research, brokerage, portfolio management, corporate finance, and fund operations. The company's financial performance is reflected in its market capitalization of TRY10.19 billion.

Oyak Yatirim Menkul Degerler showcases a compelling profile with its debt-to-equity ratio improving from 137.7% to 98.1% over five years, indicating better financial health. Despite having more cash than total debt, recent earnings reports highlight challenges, with a net loss of TRY 6.48 million in Q3 2024 compared to TRY 290.94 million profit last year and a nine-month net loss of TRY 284.01 million against last year's income of TRY 479.28 million. The price-to-earnings ratio stands at an attractive 8.2x versus the market's 16.3x, suggesting potential undervaluation amidst industry outperformance in earnings growth at 11%.

- Navigate through the intricacies of Oyak Yatirim Menkul Degerler with our comprehensive health report here.

Understand Oyak Yatirim Menkul Degerler's track record by examining our Past report.

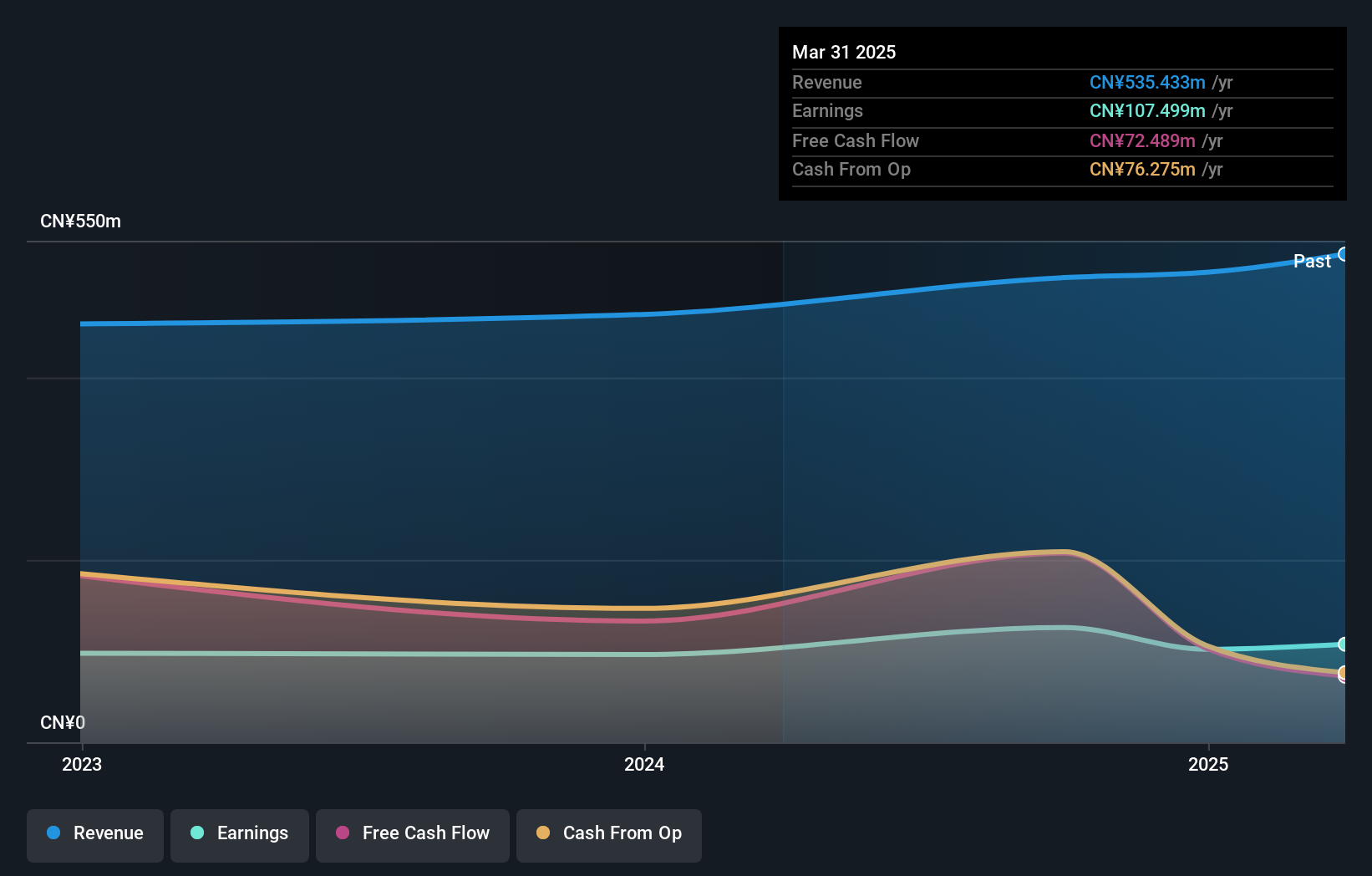

BBK Test Systems (SZSE:301598)

Simply Wall St Value Rating: ★★★★★★

Overview: BBK Test Systems Co., Ltd. specializes in the manufacturing and sale of automotive and structural testing equipment, serving both domestic and international markets, with a market capitalization of CN¥2.27 billion.

Operations: BBK Test Systems generates revenue primarily from its Solution of Automobile Test and Test System segment, contributing CN¥279.76 million, followed by the Solution of Servo Hydraulic Test System at CN¥225.29 million. The company also earns a smaller amount from Agency Services, totaling CN¥4.51 million.

BBK Test Systems, a nimble player in the machinery sector, recently completed an IPO raising CNY 566.30 million. The company is trading significantly below its estimated fair value by 63.3%, suggesting potential undervaluation. Over the past year, BBK's earnings have surged by 30.3%, outpacing industry averages and highlighting robust growth dynamics. For the nine months ending September 2024, sales climbed to CNY 322.15 million from CNY 281.77 million last year, while net income jumped to CNY 65.2 million from CNY 35.53 million previously, illustrating strong financial performance and high-quality earnings without debt burdens or interest concerns.

- Click here to discover the nuances of BBK Test Systems with our detailed analytical health report.

Assess BBK Test Systems' past performance with our detailed historical performance reports.

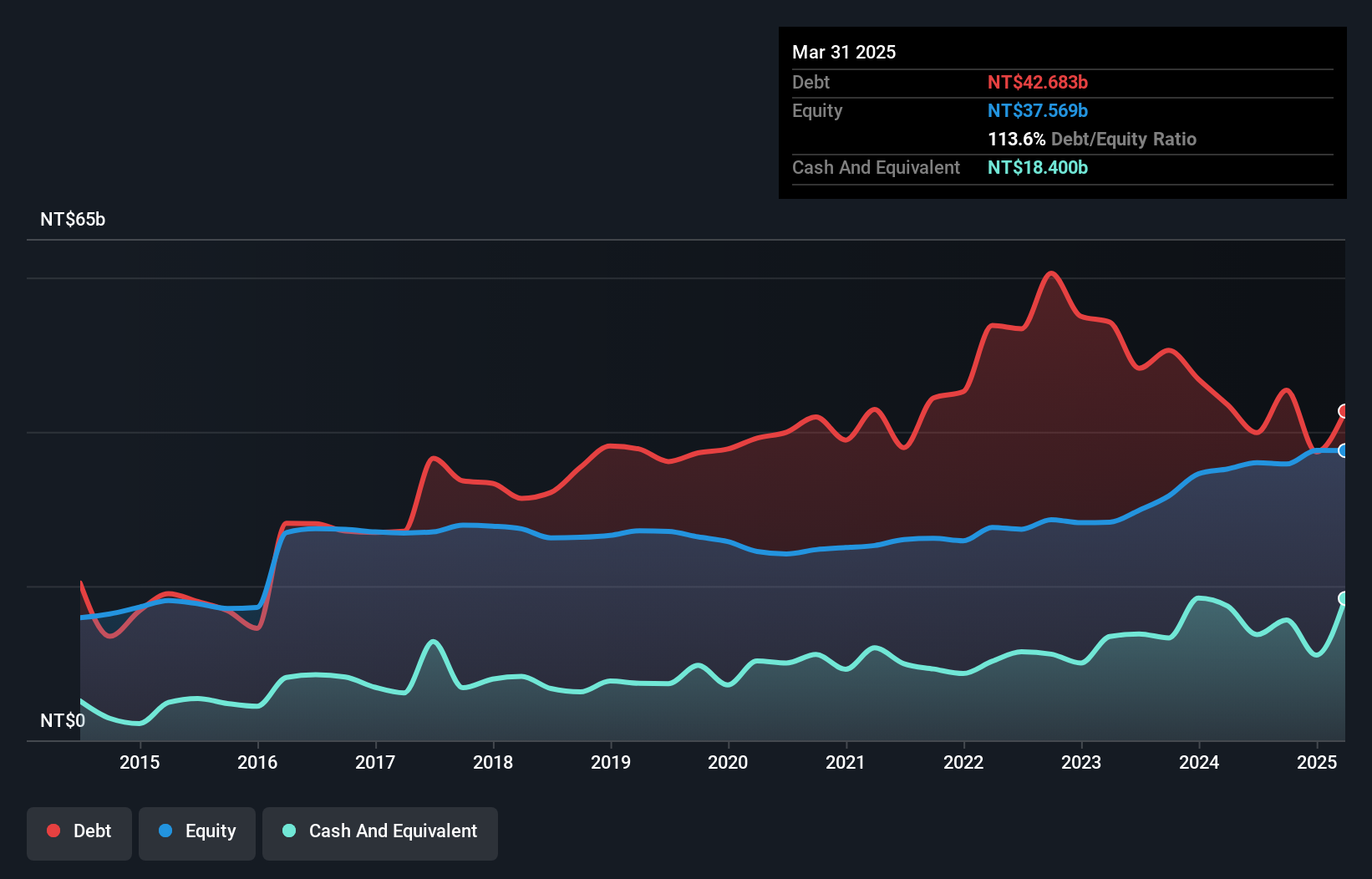

Kinpo Electronics (TWSE:2312)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Kinpo Electronics, Inc. is involved in the design, manufacture, and sale of consumer electronics, web-based communications, computer peripherals, and storage products across Taiwan and globally with a market cap of NT$40.67 billion.

Operations: Kinpo Electronics generates significant revenue from its Consumer Electronics Manufacturing Sector, amounting to NT$158.68 billion.

Kinpo Electronics has been making waves with impressive earnings growth of 97.9% over the past year, outpacing the tech industry average of 2.3%. Despite this growth, its net debt to equity ratio sits at a high 83.1%, which could be a point of concern for potential investors. However, interest payments are well covered by EBIT at 5.3 times coverage, providing some financial stability. Recent results show increased sales in Q3 to TWD 46 billion from TWD 39 billion last year and net income rising to TWD 523 million from TWD 356 million, indicating strong operational performance despite market volatility.

Key Takeaways

- Click through to start exploring the rest of the 597 Undiscovered Gems With Strong Fundamentals now.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About IBSE:OYYAT

Oyak Yatirim Menkul Degerler

Provides research, brokerage, portfolio management, corporate finance, and fund operation services for the capital market instruments in Turkey.

Excellent balance sheet with questionable track record.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)