As global markets continue to navigate the complexities of political developments and economic shifts, major indices like the S&P 500 have reached record highs, driven by optimism surrounding potential trade deals and AI investments. In this environment, identifying stocks that may be undervalued becomes particularly compelling for investors looking to capitalize on market opportunities. A good stock in today's market is one that not only shows potential for growth but also offers value relative to its current price, making it a candidate for being considered undervalued.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Türkiye Sise Ve Cam Fabrikalari (IBSE:SISE) | TRY38.86 | TRY77.57 | 49.9% |

| Fevertree Drinks (AIM:FEVR) | £6.58 | £13.12 | 49.9% |

| Atea (OB:ATEA) | NOK139.40 | NOK278.37 | 49.9% |

| PDS (NSEI:PDSL) | ₹492.20 | ₹983.09 | 49.9% |

| East Side Games Group (TSX:EAGR) | CA$0.57 | CA$1.14 | 50% |

| Kinaxis (TSX:KXS) | CA$170.04 | CA$339.70 | 49.9% |

| GemPharmatech (SHSE:688046) | CN¥13.06 | CN¥26.03 | 49.8% |

| IDP Education (ASX:IEL) | A$13.18 | A$26.30 | 49.9% |

| Shinko Electric Industries (TSE:6967) | ¥5856.00 | ¥11685.73 | 49.9% |

| Cavotec (OM:CCC) | SEK20.00 | SEK39.88 | 49.8% |

Let's review some notable picks from our screened stocks.

EQT (OM:EQT)

Overview: EQT AB (publ) is a global private equity firm focusing on private capital and real asset segments, with a market cap of approximately SEK416.06 billion.

Operations: The company's revenue segments include €0.04 billion from Central, €0.95 billion from Real Assets, and €1.36 billion from Private Capital.

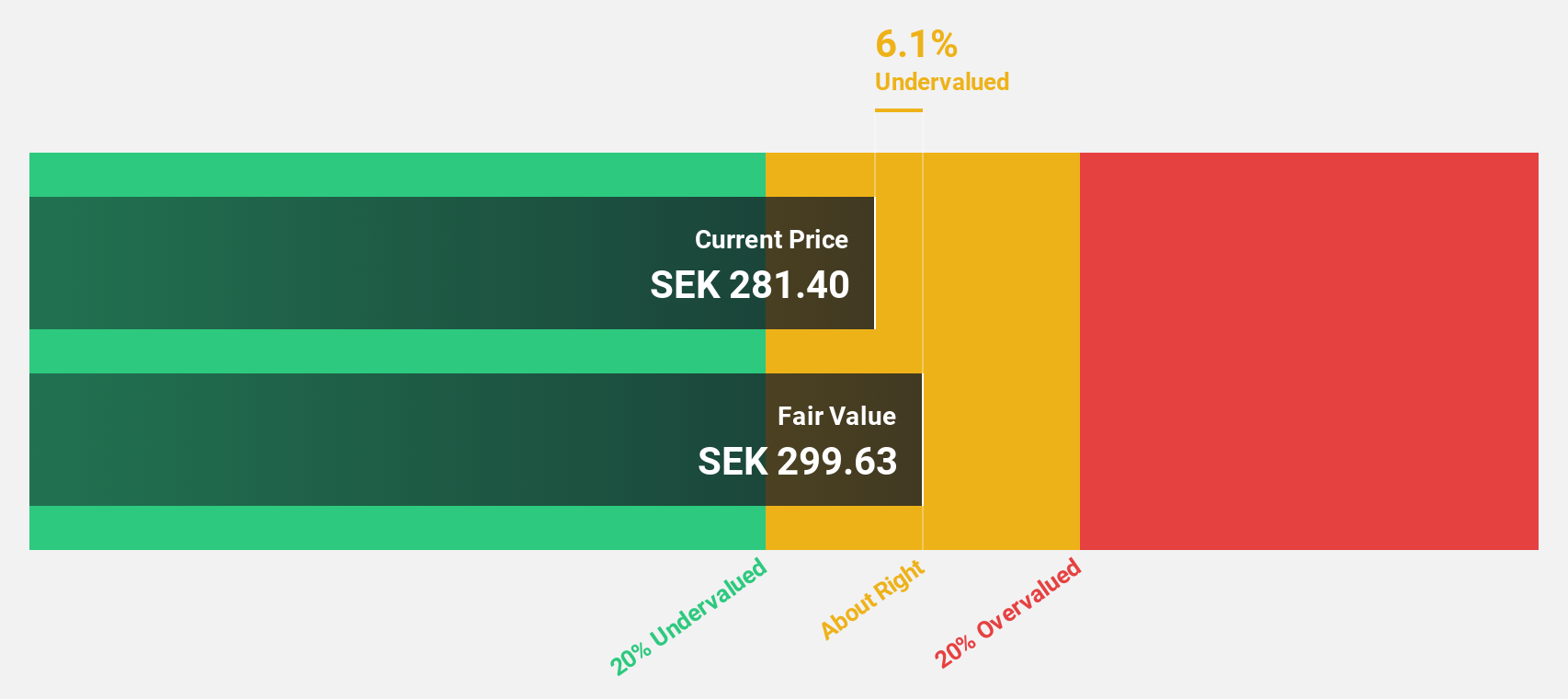

Estimated Discount To Fair Value: 14.0%

EQT is trading at SEK352.2, below its fair value estimate of SEK409.49, indicating potential undervaluation based on cash flows. The company's earnings grew significantly last year and are expected to continue growing at 27.7% annually over the next three years, outpacing the Swedish market's growth rate. Despite recent insider selling, EQT's high forecasted return on equity and revenue growth prospects suggest strong underlying fundamentals amidst ongoing M&A activities and strategic expansions.

- The analysis detailed in our EQT growth report hints at robust future financial performance.

- Click here and access our complete balance sheet health report to understand the dynamics of EQT.

HMS Networks (OM:HMS)

Overview: HMS Networks AB (publ) provides products that facilitate communication and information sharing for industrial equipment globally, with a market cap of SEK26.39 billion.

Operations: The company's revenue segment includes Wireless Communications Equipment, generating SEK3.06 billion.

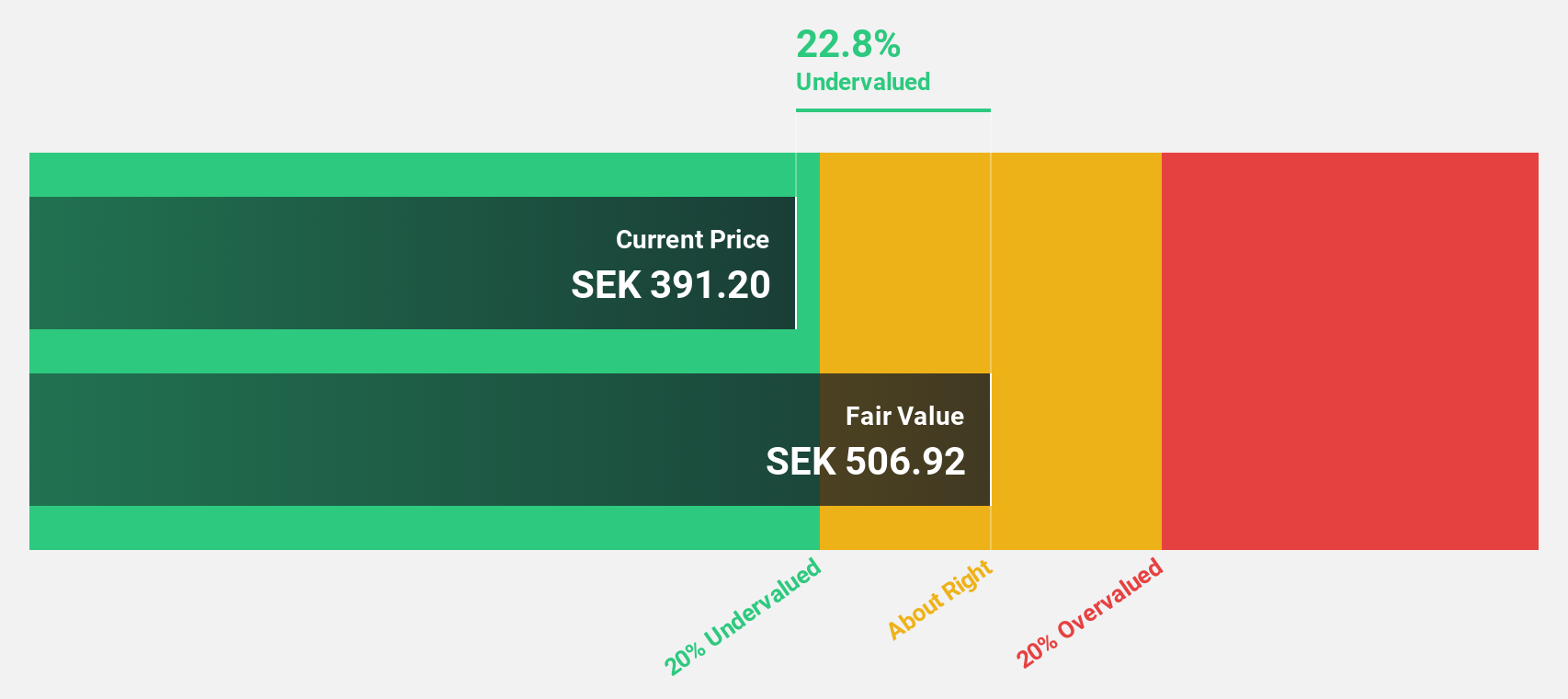

Estimated Discount To Fair Value: 12.1%

HMS Networks is trading at SEK526, below its fair value estimate of SEK598.43, reflecting potential undervaluation based on cash flows. Despite a decrease in profit margins and net income over the past year, HMS's earnings are projected to grow significantly at 31.9% annually, surpassing the Swedish market average. The company anticipates improved sales in late 2025 and has made strategic acquisitions, although no dividend is proposed due to these investments.

- Our growth report here indicates HMS Networks may be poised for an improving outlook.

- Navigate through the intricacies of HMS Networks with our comprehensive financial health report here.

NIBE Industrier (OM:NIBE B)

Overview: NIBE Industrier AB (publ) is a company that develops, manufactures, markets, and sells energy-efficient solutions for indoor climate comfort and intelligent heating control across the Nordic countries, Europe, North America, and internationally; it has a market cap of approximately SEK89.35 billion.

Operations: The company's revenue segments are comprised of Climate Solutions at SEK33.89 billion, Element at SEK13.24 billion, and Stoves at SEK5.08 billion.

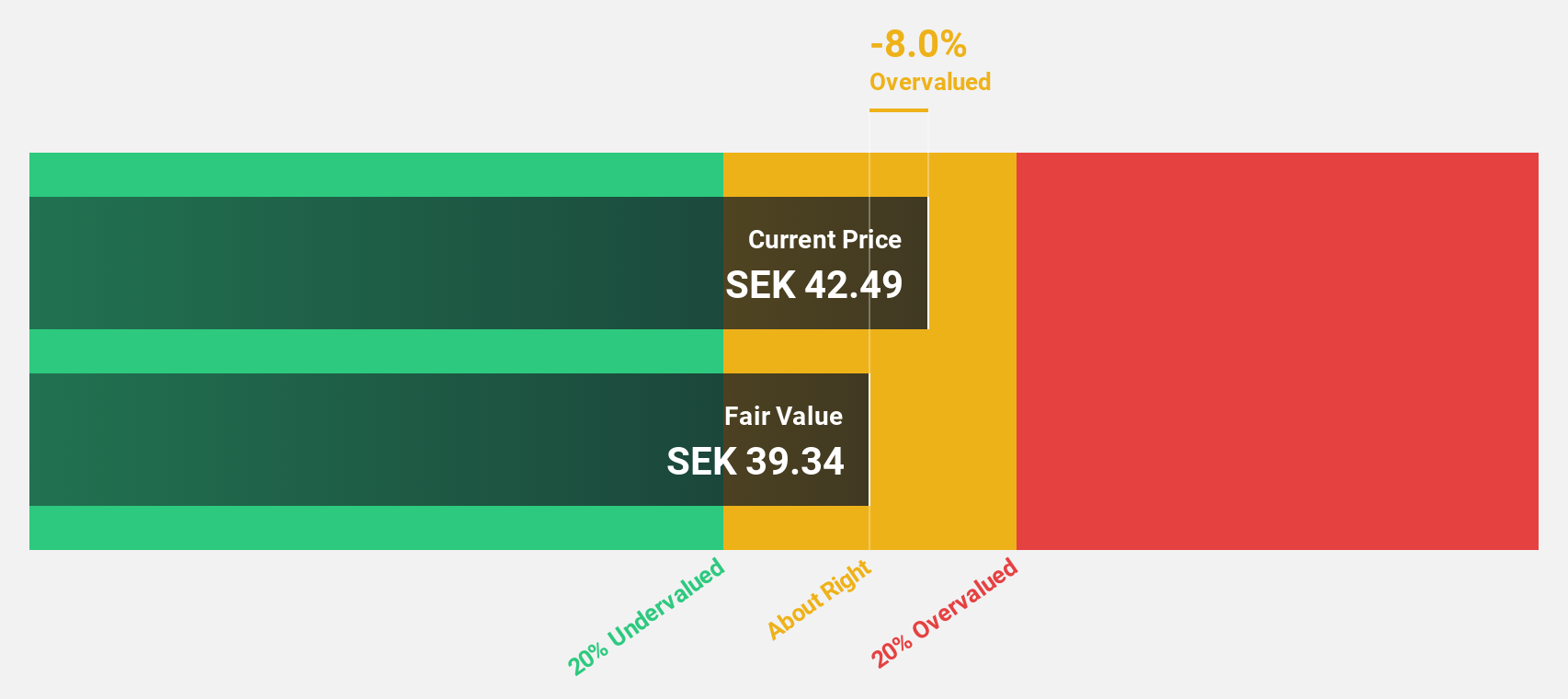

Estimated Discount To Fair Value: 16.9%

NIBE Industrier, trading at SEK44.32, is undervalued relative to its fair value of SEK53.32 based on cash flow analysis. Despite a decline in profit margins and net income over the past year, earnings are expected to grow significantly at 58.42% annually, outpacing the Swedish market's growth rate. However, interest payments remain inadequately covered by earnings and revenue growth is projected at a modest 7% per year compared to historical performance.

- Our expertly prepared growth report on NIBE Industrier implies its future financial outlook may be stronger than recent results.

- Dive into the specifics of NIBE Industrier here with our thorough financial health report.

Taking Advantage

- Click here to access our complete index of 893 Undervalued Stocks Based On Cash Flows.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if NIBE Industrier might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:NIBE B

NIBE Industrier

Develops, manufactures, markets, and sells energy-efficient solutions for indoor climate comfort, and components and solutions for intelligent heating and control.

Fair value with moderate growth potential.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)