Market Cool On Xbrane Biopharma AB (publ)'s (STO:XBRANE) Revenues Pushing Shares 34% Lower

Xbrane Biopharma AB (publ) (STO:XBRANE) shareholders won't be pleased to see that the share price has had a very rough month, dropping 34% and undoing the prior period's positive performance. For any long-term shareholders, the last month ends a year to forget by locking in a 100% share price decline.

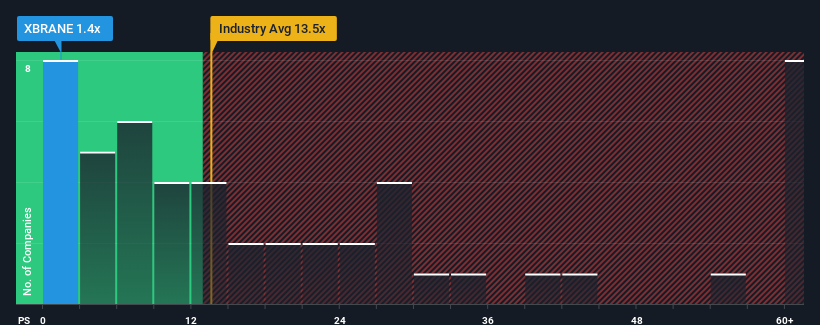

Following the heavy fall in price, Xbrane Biopharma may look like a strong buying opportunity at present with its price-to-sales (or "P/S") ratio of 1.4x, considering almost half of all companies in the Biotechs industry in Sweden have P/S ratios greater than 13.5x and even P/S higher than 30x aren't out of the ordinary. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/S.

View our latest analysis for Xbrane Biopharma

What Does Xbrane Biopharma's Recent Performance Look Like?

Recent times haven't been great for Xbrane Biopharma as its revenue has been rising slower than most other companies. Perhaps the market is expecting the current trend of poor revenue growth to continue, which has kept the P/S suppressed. If you still like the company, you'd be hoping revenue doesn't get any worse and that you could pick up some stock while it's out of favour.

Want the full picture on analyst estimates for the company? Then our free report on Xbrane Biopharma will help you uncover what's on the horizon.Do Revenue Forecasts Match The Low P/S Ratio?

There's an inherent assumption that a company should far underperform the industry for P/S ratios like Xbrane Biopharma's to be considered reasonable.

If we review the last year of revenue growth, the company posted a terrific increase of 70%. Spectacularly, three year revenue growth has ballooned by several orders of magnitude, thanks in part to the last 12 months of revenue growth. So we can start by confirming that the company has done a tremendous job of growing revenue over that time.

Shifting to the future, estimates from the dual analysts covering the company suggest revenue should grow by 123% over the next year. Meanwhile, the rest of the industry is forecast to only expand by 49%, which is noticeably less attractive.

In light of this, it's peculiar that Xbrane Biopharma's P/S sits below the majority of other companies. Apparently some shareholders are doubtful of the forecasts and have been accepting significantly lower selling prices.

The Bottom Line On Xbrane Biopharma's P/S

Having almost fallen off a cliff, Xbrane Biopharma's share price has pulled its P/S way down as well. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

A look at Xbrane Biopharma's revenues reveals that, despite glowing future growth forecasts, its P/S is much lower than we'd expect. There could be some major risk factors that are placing downward pressure on the P/S ratio. At least price risks look to be very low, but investors seem to think future revenues could see a lot of volatility.

And what about other risks? Every company has them, and we've spotted 4 warning signs for Xbrane Biopharma (of which 2 are concerning!) you should know about.

If these risks are making you reconsider your opinion on Xbrane Biopharma, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:XBRANE

Xbrane Biopharma

A biotechnology company, engages in the development, manufacture, and sale of biosimilars.

Exceptional growth potential slight.