Billerud AB (publ) (STO:BILL) Just Released Its Third-Quarter Earnings: Here's What Analysts Think

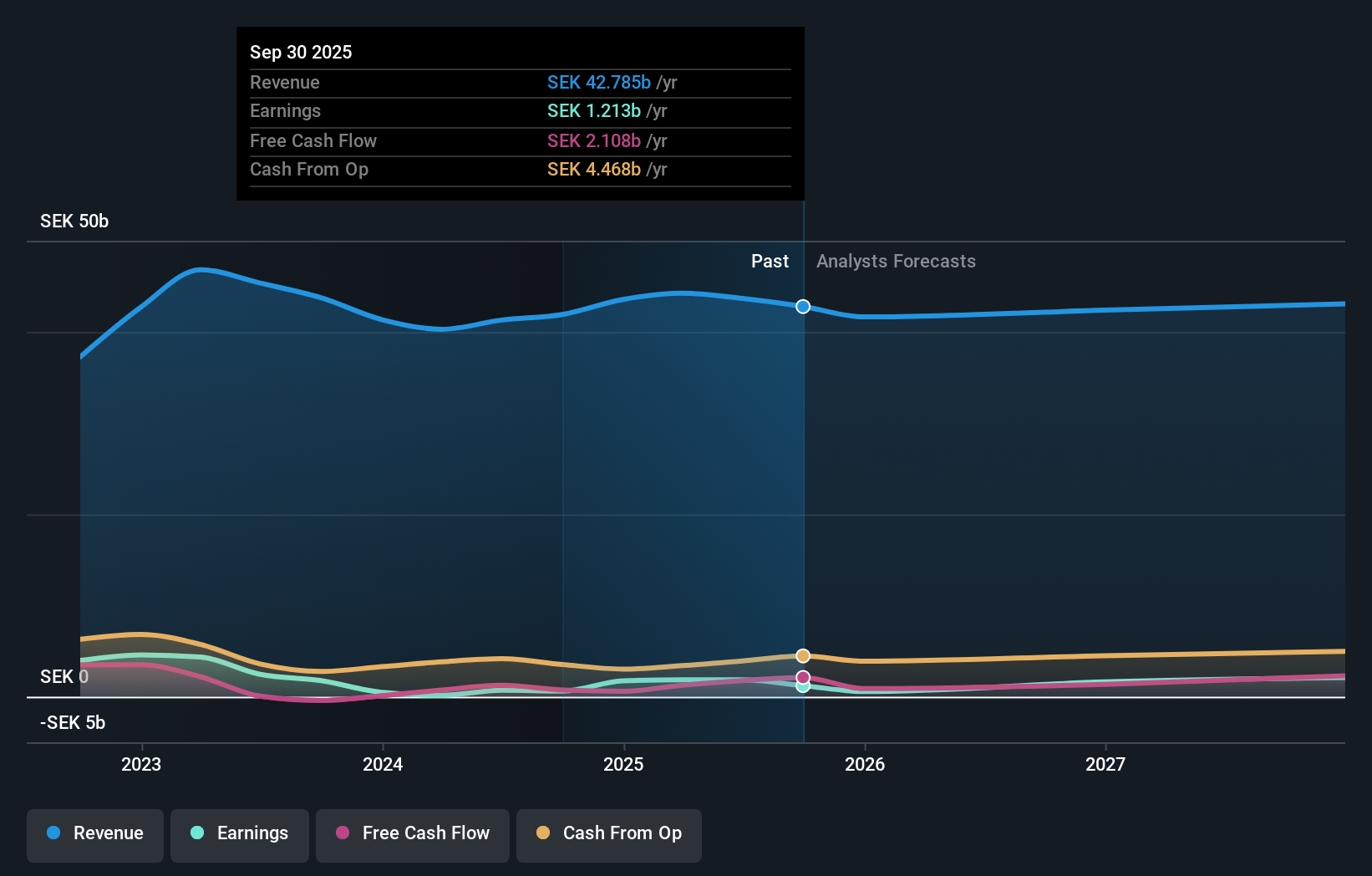

Investors in Billerud AB (publ) (STO:BILL) had a good week, as its shares rose 7.0% to close at kr89.85 following the release of its third-quarter results. Revenues of kr9.9b came in a modest 2.8% below forecasts. Statutory losses were a relative bright spot though, with a per-share loss of kr0.25 coming in a substantial 51% smaller than what the analysts had expected. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

Following last week's earnings report, Billerud's six analysts are forecasting 2026 revenues to be kr42.4b, approximately in line with the last 12 months. Per-share earnings are expected to surge 32% to kr6.43. Before this earnings report, the analysts had been forecasting revenues of kr43.3b and earnings per share (EPS) of kr6.03 in 2026. So it's pretty clear that while sentiment around revenues has declined following the latest results, the analysts are now more bullish on the company's earnings power.

See our latest analysis for Billerud

There's been no real change to the average price target of kr103, with the lower revenue and higher earnings forecasts not expected to meaningfully impact the company's valuation over a longer timeframe. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. There are some variant perceptions on Billerud, with the most bullish analyst valuing it at kr119 and the most bearish at kr80.00 per share. Analysts definitely have varying views on the business, but the spread of estimates is not wide enough in our view to suggest that extreme outcomes could await Billerud shareholders.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. We would highlight that revenue is expected to reverse, with a forecast 0.7% annualised decline to the end of 2026. That is a notable change from historical growth of 13% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 2.7% per year. It's pretty clear that Billerud's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The biggest takeaway for us is the consensus earnings per share upgrade, which suggests a clear improvement in sentiment around Billerud's earnings potential next year. Unfortunately, they also downgraded their revenue estimates, and our data indicates underperformance compared to the wider industry. Even so, earnings per share are more important to the intrinsic value of the business. Even so, long term profitability is more important for the value creation process. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

With that in mind, we wouldn't be too quick to come to a conclusion on Billerud. Long-term earnings power is much more important than next year's profits. At Simply Wall St, we have a full range of analyst estimates for Billerud going out to 2027, and you can see them free on our platform here..

It is also worth noting that we have found 2 warning signs for Billerud that you need to take into consideration.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Billerud might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:BILL

Flawless balance sheet average dividend payer.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)