- Sweden

- /

- Hospitality

- /

- OM:EVO

Evolution (OM:EVO) Announces €346M Share Buyback

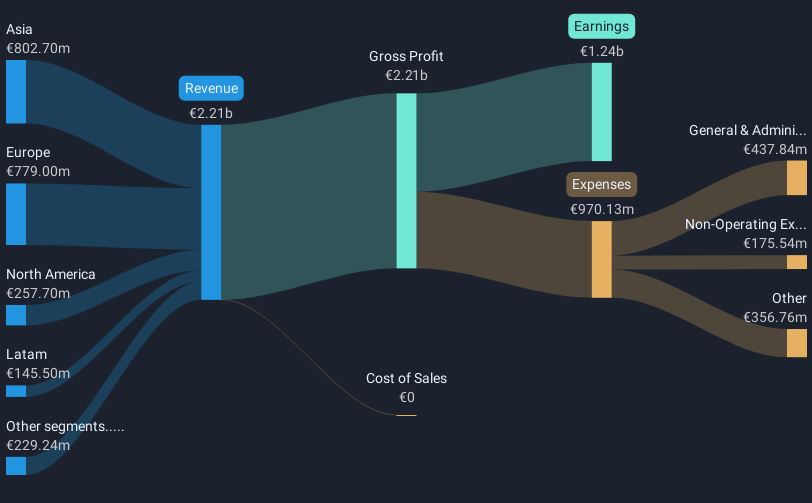

Evolution (OM:EVO) recently initiated a share buyback program on May 15, 2025, aimed at optimizing shareholder value and improving its capital structure, financed by up to €346 million. This move likely bolstered investor confidence, contributing to the company’s 11% stock price increase over the past week. Despite broader market challenges, such as rising oil prices and geopolitical tensions involving Israel and Iran, Evolution's targeted financial strategies appeared to enhance its market performance. The overall flat market conditions serve as a contrasting backdrop, emphasizing Evolution's significant individual gains linked to its strategic repurchase efforts.

Buy, Hold or Sell Evolution? View our complete analysis and fair value estimate and you decide.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Over a five-year period, Evolution AB's total shareholder return, including share price and dividends, was 35.27%. This performance has outpaced the broader Swedish market, which showed a 3.1% decline over the past year, although it fell short of the Swedish Hospitality industry's more dramatic 20.2% drop in the same timeframe. This indicates that the company's long-term growth trajectory remains robust despite recent challenges.

The company's share buyback initiative and sustained dividend payments could positively influence future revenue and earnings forecasts by attracting further investor interest. However, the high Basic EPS of €1.24 in Q1 2025 suggests a 2.36% decline from the previous year, indicating potential near-term pressures. Despite these factors, the recent share price increase of 11% still supports its margin against a consensus analyst price target, suggesting that Evolution AB remains undervalued at its current trading price. Analysts have not reached a statistically confident consensus, but the target price remains more than 20% higher than the current price, highlighting potential upside potential. These figures indicate that Evolution's financial strategies may continue to support its share value amid broader market challenges.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Evolution might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:EVO

Evolution

Develops, produces, markets, and licenses live casino and slots solutions to gaming operators in Europe, Asia, North America, Latin America, and internationally.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Weekly Picks

When GPS fails: this small cap is fixing a $54B drone problem

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

The Architecture Layer of AI Computing - But Priced Like the Future Already Arrived?

Temporary "perfect storm" leads to opportunity to buy financial services leader for less than 5x long-term earnings

Recently Updated Narratives

Investor Thesis: Why XPLR Infrastructure Could Be Deeply Undervalued in an AI Power Cycle

Netflix - A Fundamental Valuation

Reddit's Discount Is Big Enough to Make Me Suspicious. Here's What I Found When I Went Looking for the Reason.

Popular Narratives

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

A wonderful business at reasonable price.

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Trending Discussion