- Sweden

- /

- Commercial Services

- /

- OM:BRAV

Bravida Holding AB (publ)'s (STO:BRAV) CEO Compensation Looks Acceptable To Us And Here's Why

Key Insights

- Bravida Holding to hold its Annual General Meeting on 7th of May

- Salary of kr8.17m is part of CEO Mattias Johansson's total remuneration

- Total compensation is 41% below industry average

- Over the past three years, Bravida Holding's EPS grew by 6.8% and over the past three years, the total loss to shareholders 36%

The performance at Bravida Holding AB (publ) (STO:BRAV) has been rather lacklustre of late and shareholders may be wondering what CEO Mattias Johansson is planning to do about this. One way they can exercise their influence on management is through voting on resolutions, such as executive remuneration at the next AGM, coming up on 7th of May. It has been shown that setting appropriate executive remuneration incentivises the management to act in the interests of shareholders. We think CEO compensation looks appropriate given the data we have put together.

Check out our latest analysis for Bravida Holding

Comparing Bravida Holding AB (publ)'s CEO Compensation With The Industry

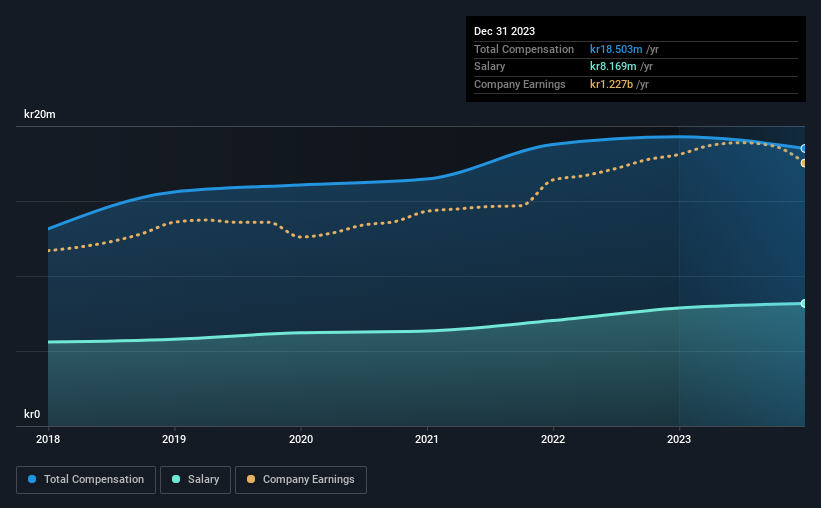

According to our data, Bravida Holding AB (publ) has a market capitalization of kr15b, and paid its CEO total annual compensation worth kr19m over the year to December 2023. That's a slight decrease of 4.1% on the prior year. While we always look at total compensation first, our analysis shows that the salary component is less, at kr8.2m.

On examining similar-sized companies in the Swedish Commercial Services industry with market capitalizations between kr11b and kr35b, we discovered that the median CEO total compensation of that group was kr31m. That is to say, Mattias Johansson is paid under the industry median. What's more, Mattias Johansson holds kr56m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | kr8.2m | kr7.9m | 44% |

| Other | kr10m | kr11m | 56% |

| Total Compensation | kr19m | kr19m | 100% |

On an industry level, around 53% of total compensation represents salary and 47% is other remuneration. In Bravida Holding's case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

Bravida Holding AB (publ)'s Growth

Over the past three years, Bravida Holding AB (publ) has seen its earnings per share (EPS) grow by 6.8% per year. It achieved revenue growth of 12% over the last year.

We think the revenue growth is good. And the improvement in EPSis modest but respectable. Although we'll stop short of calling the stock a top performer, we think the company has potential. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has Bravida Holding AB (publ) Been A Good Investment?

The return of -36% over three years would not have pleased Bravida Holding AB (publ) shareholders. So shareholders would probably want the company to be less generous with CEO compensation.

To Conclude...

The fact that shareholders have earned a negative share price return is certainly disconcerting. The disappointing performance may have something to do with the flat earnings growth. The upcoming AGM will provide shareholders the opportunity to raise their concerns and evaluate if the board’s judgement and decision-making is aligned with their expectations.

CEO compensation can have a massive impact on performance, but it's just one element. That's why we did some digging and identified 1 warning sign for Bravida Holding that you should be aware of before investing.

Important note: Bravida Holding is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

If you're looking to trade Bravida Holding, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Bravida Holding might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:BRAV

Bravida Holding

Provides technical services and installations for buildings and industrial facilities in Sweden, Norway, Denmark, and Finland.

Excellent balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Community Narratives