Advertisement

- Saudi Arabia

- /

- Wireless Telecom

- /

- SASE:7020

Is Etihad Etisalat Company's (TADAWUL:7020) Recent Stock Performance Influenced By Its Fundamentals In Any Way?

Most readers would already be aware that Etihad Etisalat's (TADAWUL:7020) stock increased significantly by 16% over the past three months. Given that stock prices are usually aligned with a company's financial performance in the long-term, we decided to study its financial indicators more closely to see if they had a hand to play in the recent price move. In this article, we decided to focus on Etihad Etisalat's ROE.

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. In simpler terms, it measures the profitability of a company in relation to shareholder's equity.

How To Calculate Return On Equity?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Etihad Etisalat is:

18% = ر.س3.4b ÷ ر.س19b (Based on the trailing twelve months to June 2025).

The 'return' is the profit over the last twelve months. So, this means that for every SAR1 of its shareholder's investments, the company generates a profit of SAR0.18.

Check out our latest analysis for Etihad Etisalat

What Has ROE Got To Do With Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

A Side By Side comparison of Etihad Etisalat's Earnings Growth And 18% ROE

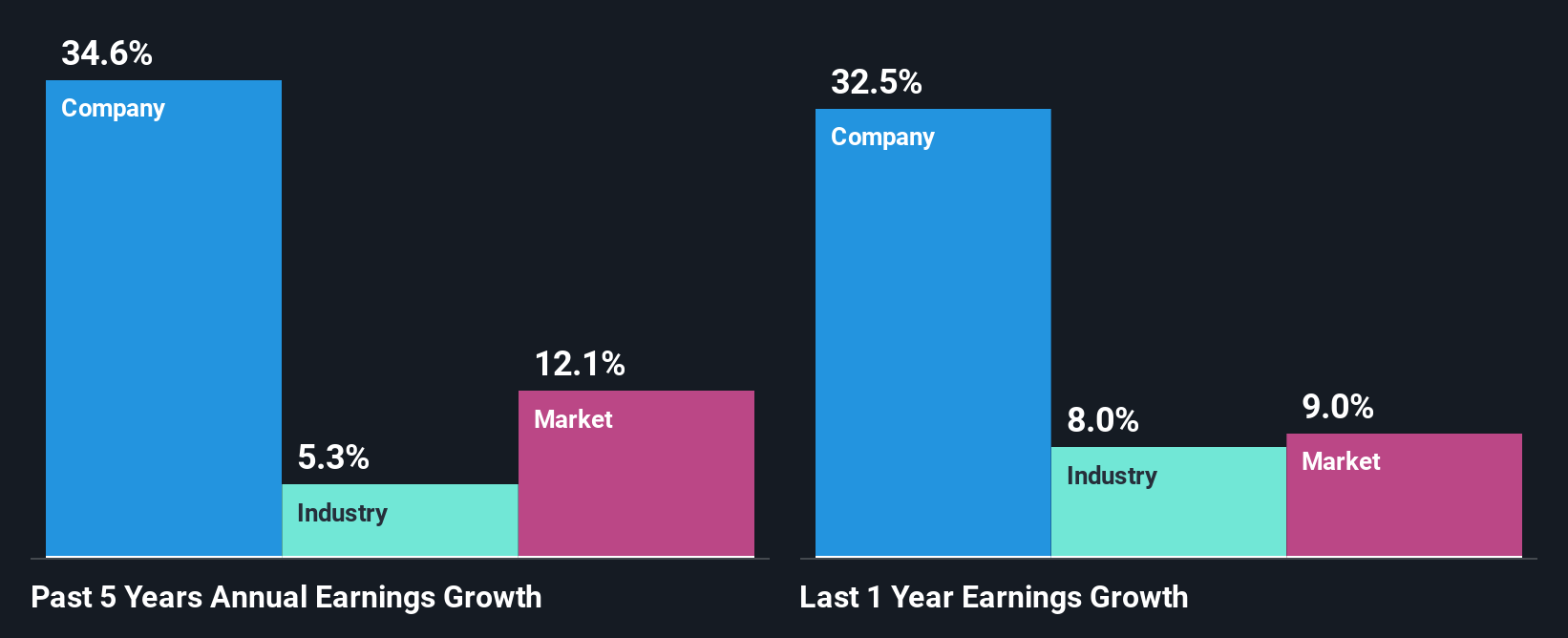

When you first look at it, Etihad Etisalat's ROE doesn't look that attractive. However, the fact that the company's ROE is higher than the average industry ROE of 13%, is definitely interesting. Even more so after seeing Etihad Etisalat's exceptional 35% net income growth over the past five years. That being said, the company does have a slightly low ROE to begin with, just that it is higher than the industry average. So, there might well be other reasons for the earnings to grow. Such as- high earnings retention or the company belonging to a high growth industry.

We then compared Etihad Etisalat's net income growth with the industry and we're pleased to see that the company's growth figure is higher when compared with the industry which has a growth rate of 5.3% in the same 5-year period.

Earnings growth is a huge factor in stock valuation. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. This then helps them determine if the stock is placed for a bright or bleak future. Has the market priced in the future outlook for 7020? You can find out in our latest intrinsic value infographic research report.

Is Etihad Etisalat Using Its Retained Earnings Effectively?

Etihad Etisalat has a significant three-year median payout ratio of 51%, meaning the company only retains 49% of its income. This implies that the company has been able to achieve high earnings growth despite returning most of its profits to shareholders.

Besides, Etihad Etisalat has been paying dividends over a period of five years. This shows that the company is committed to sharing profits with its shareholders. Our latest analyst data shows that the future payout ratio of the company over the next three years is expected to be approximately 60%. As a result, Etihad Etisalat's ROE is not expected to change by much either, which we inferred from the analyst estimate of 18% for future ROE.

Conclusion

Overall, we feel that Etihad Etisalat certainly does have some positive factors to consider. Namely, its significant earnings growth, to which its moderate rate of return likely contributed. While the company is paying out most of its earnings as dividends, it has been able to grow its earnings in spite of it, so that's probably a good sign. With that said, the latest industry analyst forecasts reveal that the company's earnings growth is expected to slow down. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

Valuation is complex, but we're here to simplify it.

Discover if Etihad Etisalat might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SASE:7020

Etihad Etisalat

Through its subsidiaries, establishes and operates mobile wireless telecommunication and fiber optic networks in the Kingdom of Saudi Arabia.

Good value with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.9% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$89.00|21.8% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|40.6% undervalued

TR

Community Contributor