- Saudi Arabia

- /

- Healthcare Services

- /

- SASE:4009

Middle East Healthcare First Quarter 2025 Earnings: Revenues Beat Expectations, EPS Lags

Middle East Healthcare (TADAWUL:4009) First Quarter 2025 Results

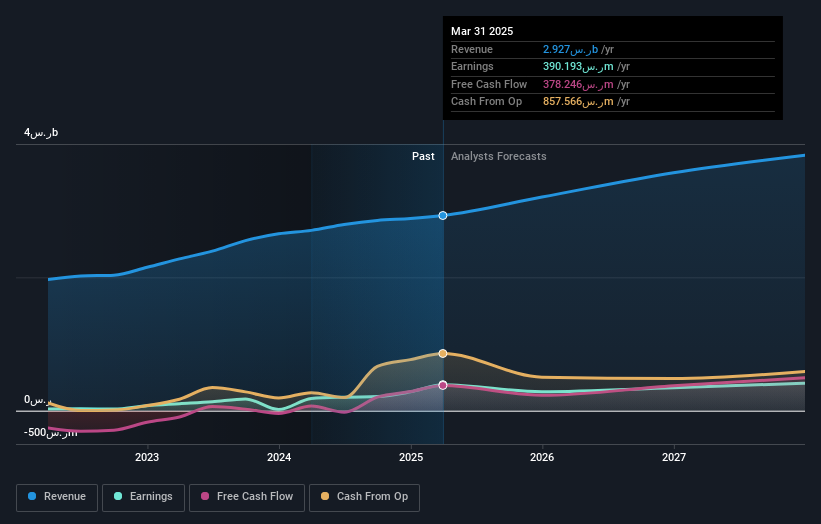

Key Financial Results

- Revenue: ر.س733.7m (up 6.5% from 1Q 2024).

- Net income: ر.س160.1m (up 208% from 1Q 2024).

- Profit margin: 22% (up from 7.5% in 1Q 2024). The increase in margin was primarily driven by lower expenses.

- EPS: ر.س1.74 (up from ر.س0.56 in 1Q 2024).

All figures shown in the chart above are for the trailing 12 month (TTM) period

Middle East Healthcare Revenues Beat Expectations, EPS Falls Short

Revenue exceeded analyst estimates by 4.4%. Earnings per share (EPS) missed analyst estimates by 4.4%.

Looking ahead, revenue is forecast to grow 8.4% p.a. on average during the next 3 years, compared to a 12% growth forecast for the Healthcare industry in Saudi Arabia.

Performance of the Saudi Healthcare industry.

The company's shares are down 6.7% from a week ago.

Valuation

Following the latest earnings results, Middle East Healthcare may be undervalued based on 6 different valuation benchmarks we assess. Discover what analysts are forecasting and how the current share price shapes up by clicking here.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SASE:4009

Middle East Healthcare

A healthcare provider, owns and operates a network of hospitals under the Saudi German Hospital name in the Middle East and North Africa.

Very undervalued with proven track record.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)