Advertisement

Many investors consider it preferable to invest in profitable companies over unprofitable ones, because profitability suggests a business is sustainable. However, sometimes companies receive a one-off boost (or reduction) to their profit, and it's not always clear whether statutory profits are a good guide, going forward. This article will consider whether Comp's (WSE:CMP) statutory profits are a good guide to its underlying earnings.

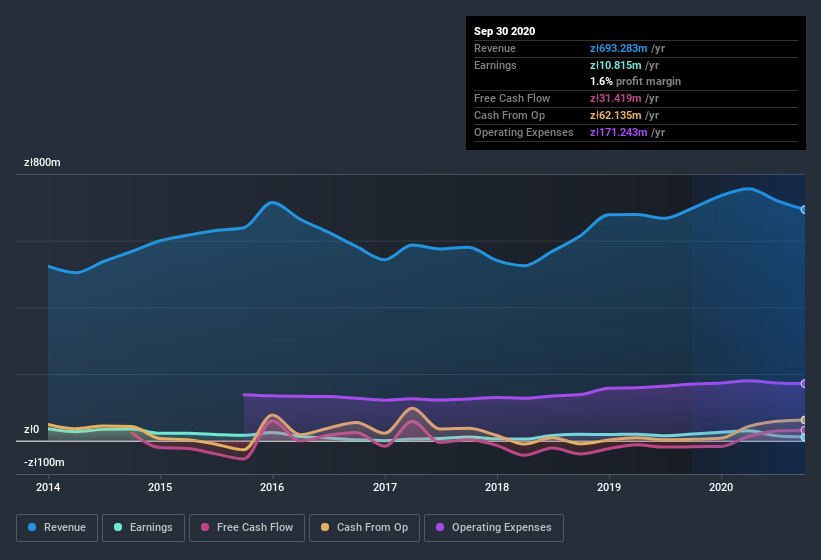

We like the fact that Comp made a profit of zł10.8m on its revenue of zł693.3m, in the last year. As you can see in the chart below, its profit has declined over the last three years, even though its revenue has increased.

View our latest analysis for Comp

Importantly, statutory profits are not always the best tool for understanding a company's true earnings power, so it's well worth examining profits in a little more detail. This article will discuss how unusual items have impacted Comp's most recent profit results. Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Comp.

The Impact Of Unusual Items On Profit

Importantly, our data indicates that Comp's profit was reduced by zł3.2m, due to unusual items, over the last year. It's never great to see unusual items costing the company profits, but on the upside, things might improve sooner rather than later. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And, after all, that's exactly what the accounting terminology implies. If Comp doesn't see those unusual expenses repeat, then all else being equal we'd expect its profit to increase over the coming year.

Our Take On Comp's Profit Performance

Because unusual items detracted from Comp's earnings over the last year, you could argue that we can expect an improved result in the current quarter. Because of this, we think Comp's earnings potential is at least as good as it seems, and maybe even better! On the other hand, its EPS actually shrunk in the last twelve months. Of course, we've only just scratched the surface when it comes to analysing its earnings; one could also consider margins, forecast growth, and return on investment, among other factors. With this in mind, we wouldn't consider investing in a stock unless we had a thorough understanding of the risks. You'd be interested to know, that we found 3 warning signs for Comp and you'll want to know about these.

Today we've zoomed in on a single data point to better understand the nature of Comp's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

If you’re looking to trade Comp, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About WSE:CMP

Comp

A technology firm, provides IT security and network security services and solutions in Poland.

Flawless balance sheet with solid track record.

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Optimi Health ·

OPTH: A licensed manufacturer already selling MDMA while peers still wait on trials

Fair Value:US$1257.9% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HA

HarishPK on Amdocs ·

Why Amdocs is a high conviction Buy for me?

Fair Value:US$82.0328.6% undervalued

36 followersusers have followed this narrative

3 commentsusers have commented on this narrative

12 likesusers have liked this narrative

IV

Ivoed on SBM Offshore ·

Why SBM Offshore’s €30 Share Price May Be Too Harsh On Its Backlog

Fair Value:€44.524.7% undervalued

22 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

CL

Clive_Thompson on Green Tea Group ·

One of China's Fastest-Growing Restaurant Chains Trades on Just 7x Earnings and an 8% Dividend

Fair Value:HK$8.719.3% undervalued

47 followersusers have followed this narrative

3 commentsusers have commented on this narrative

20 likesusers have liked this narrative

Recently Updated Narratives

AS

AstrisCorporateAdvisory on Rigaku Holdings ·

Capitalizing on rising semiconductor complexity

Fair Value:JP¥2.52k22.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

UM

UmarHashmi on Lucky Cement ·

Lucky Cement expected to bloom with 12% revenue growth

Fair Value:PK₨64029.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Denarius Metals ·

558% IRR Gold Project Already in Production, Colombia’s Next Major Producer

Fair Value:CA$110.1399.5% undervalued

26 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28020.0% undervalued

286 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9119.1% overvalued

149 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

KI

KiwiInvest on Amazon.com ·

Amazon's high growth, high tech segments propel its profits, while traditional segments plod along

Fair Value:US$475.0942.2% undervalued

171 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

Trending Discussion

IA

ian_oii7z on Woodside Energy Group ·

Hey James! Thank you but I am not sure if I am reading this correctly as your analysis opens with "At A$36.602 per share, Woodside Energy Group (ASX: WDS) appears reasonably valued based on its existing operations and near-term production growth." I would like to say that the last time that WDS was above $36.00 per share was in October 2023, so I am a little confused by your statement w.r.t. current prices etc . Can you please explain?

1

|0

YA

Yash_Upadhyaya on Reddit ·

Steve blamed "choppy" Google referral traffic for the miss on US daily active user (DAU) WHILST being in a standoff with Google on the AI licensing deal... hmm 🤔 One way or another a deal is happening. What's gonna be interesting is to see how good or bad (which the market is pricing in) would it be. PS - I don't own the stock but like the company.

1

|0