Advertisement

- Poland

- /

- Entertainment

- /

- WSE:PLW

Don't Buy PlayWay S.A. (WSE:PLW) For Its Next Dividend Without Doing These Checks

PlayWay S.A. (WSE:PLW) is about to trade ex-dividend in the next four days. The ex-dividend date is one business day before a company's record date, which is the date on which the company determines which shareholders are entitled to receive a dividend. It is important to be aware of the ex-dividend date because any trade on the stock needs to have been settled on or before the record date. Accordingly, PlayWay investors that purchase the stock on or after the 2nd of July will not receive the dividend, which will be paid on the 10th of July.

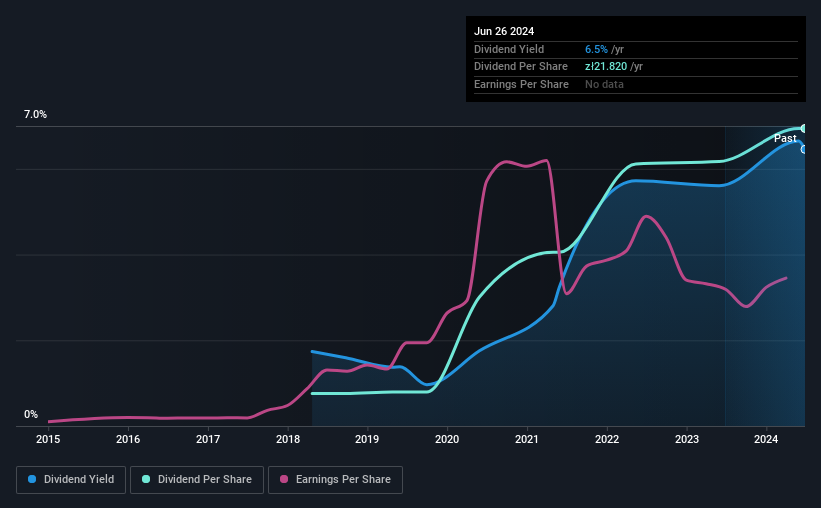

The company's next dividend payment will be zł21.82 per share, on the back of last year when the company paid a total of zł21.82 to shareholders. Based on the last year's worth of payments, PlayWay stock has a trailing yield of around 6.5% on the current share price of zł338.00. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. We need to see whether the dividend is covered by earnings and if it's growing.

View our latest analysis for PlayWay

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. PlayWay paid out 126% of profit in the past year, which we think is typically not sustainable unless there are mitigating characteristics such as unusually strong cash flow or a large cash balance. Yet cash flows are even more important than profits for assessing a dividend, so we need to see if the company generated enough cash to pay its distribution. It paid out 105% of its free cash flow in the form of dividends last year, which is outside the comfort zone for most businesses. Cash flows are usually much more volatile than earnings, so this could be a temporary effect - but we'd generally want to look more closely here.

PlayWay does have a large net cash position on the balance sheet, which could fund large dividends for a time, if the company so chose. Still, smart investors know that it is better to assess dividends relative to the cash and profit generated by the business. Paying dividends out of cash on the balance sheet is not long-term sustainable.

Cash is slightly more important than profit from a dividend perspective, but given PlayWay's payouts were not well covered by either earnings or cash flow, we would be concerned about the sustainability of this dividend.

Click here to see how much of its profit PlayWay paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Businesses with strong growth prospects usually make the best dividend payers, because it's easier to grow dividends when earnings per share are improving. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. For this reason, we're glad to see PlayWay's earnings per share have risen 19% per annum over the last five years. We're a bit put out by the fact that PlayWay paid out virtually all of its earnings and cashflow as dividends over the last year. Earnings are growing at a decent clip, so this payout ratio may prove sustainable, but it's not great to see.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. In the last six years, PlayWay has lifted its dividend by approximately 45% a year on average. Both per-share earnings and dividends have both been growing rapidly in recent times, which is great to see.

To Sum It Up

Is PlayWay an attractive dividend stock, or better left on the shelf? Earnings per share have been growing, despite the company paying out a concerningly high percentage of its earnings and cashflow. We struggle to see how a company paying out so much of its earnings and cash flow will be able to sustain its dividend in a downturn, or reinvest enough into its business to continue growing earnings without borrowing heavily. It's not that we think PlayWay is a bad company, but these characteristics don't generally lead to outstanding dividend performance.

So if you're still interested in PlayWay despite it's poor dividend qualities, you should be well informed on some of the risks facing this stock. Our analysis shows 3 warning signs for PlayWay that we strongly recommend you have a look at before investing in the company.

If you're in the market for strong dividend payers, we recommend checking our selection of top dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About WSE:PLW

Very undervalued with solid track record.

Market Insights

Advertisement

Community Narratives

RIO is poised to weather a depressed iron ore environment, but commodity diversification comes with lower margins

Fair Value AU$110.51|3.0% overvalued

DU

Community Contributor

The demand for personalized medicine will keep Thermo Fisher Scientific thriving

Fair Value US$540.27|19.5% undervalued

UN

Community Contributor

Silver Play by A Family with 10x Potential

Fair Value UK£24.00|88.5% undervalued

RO

Community Contributor