- New Zealand

- /

- Healthcare Services

- /

- NZSE:RYM

Insiders Could Have Profited By Holding onto Ryman Healthcare Shares Despite 29% Drop

Ryman Healthcare Limited's (NZSE:RYM) stock price has dropped 29% in the previous week, but insiders who sold NZ$926k in stock over the past year have had less luck. Insiders might have been better off holding onto their shares, given that the average selling price of NZ$4.33 is still below the current share price.

Although we don't think shareholders should simply follow insider transactions, we would consider it foolish to ignore insider transactions altogether.

Check out our latest analysis for Ryman Healthcare

Ryman Healthcare Insider Transactions Over The Last Year

In the last twelve months, the biggest single sale by an insider was when the insider, David Bennett, sold NZ$612k worth of shares at a price of NZ$4.45 per share. While insider selling is a negative, to us, it is more negative if the shares are sold at a lower price. The silver lining is that this sell-down took place above the latest price (NZ$3.08). So it is hard to draw any strong conclusion from it.

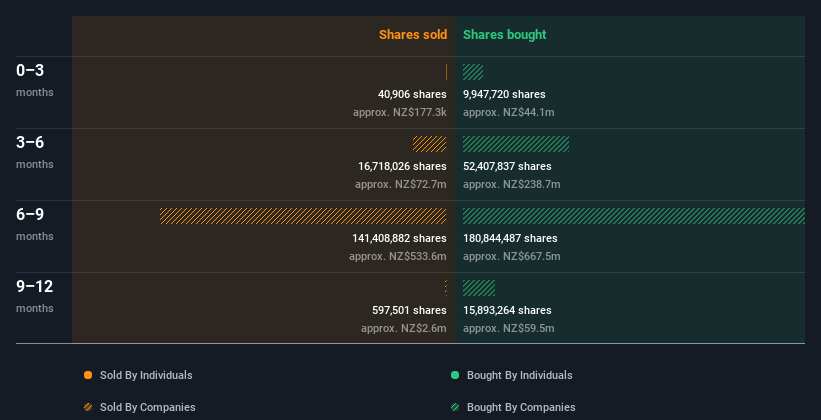

Over the last year, we can see that insiders have bought 146.27k shares worth NZ$583k. But they sold 213.96k shares for NZ$926k. Over the last year we saw more insider selling of Ryman Healthcare shares, than buying. The average sell price was around NZ$4.33. We are not joyful about insider selling. But the selling was at much higher prices than the current share price (NZ$3.08), so it probably doesn't tell us a lot about the value on offer today. You can see a visual depiction of insider transactions (by companies and individuals) over the last 12 months, below. By clicking on the graph below, you can see the precise details of each insider transaction!

If you are like me, then you will not want to miss this free list of small cap stocks that are not only being bought by insiders but also have attractive valuations.

Have Ryman Healthcare Insiders Traded Recently?

In the last three months, insiders sold NZ$175k. That's only a tiny bit more than the purchases, worth NZ$167k. The net selling is so small that it's hard to draw any conclusions from these recent transactions.

Insider Ownership

Looking at the total insider shareholdings in a company can help to inform your view of whether they are well aligned with common shareholders. Usually, the higher the insider ownership, the more likely it is that insiders will be incentivised to build the company for the long term. Ryman Healthcare insiders own about NZ$104m worth of shares. That equates to 4.9% of the company. We've certainly seen higher levels of insider ownership elsewhere, but these holdings are enough to suggest alignment between insiders and the other shareholders.

So What Does This Data Suggest About Ryman Healthcare Insiders?

Our data shows a little more insider selling than buying in the last three months. But the difference isn't enough to have us worried. It's great to see high levels of insider ownership, but looking back over the last year, we'd need to see more buying to gain confidence from the Ryman Healthcare insider transactions. So while it's helpful to know what insiders are doing in terms of buying or selling, it's also helpful to know the risks that a particular company is facing. For example - Ryman Healthcare has 2 warning signs we think you should be aware of.

If you would prefer to check out another company -- one with potentially superior financials -- then do not miss this free list of interesting companies, that have HIGH return on equity and low debt.

For the purposes of this article, insiders are those individuals who report their transactions to the relevant regulatory body. We currently account for open market transactions and private dispositions of direct interests only, but not derivative transactions or indirect interests.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NZSE:RYM

Ryman Healthcare

Develops, owns, and operates integrated retirement villages, rest homes, and hospitals for the elderly people in New Zealand and Australia.

Reasonable growth potential and fair value.

Similar Companies

Market Insights

Community Narratives