Shareholders May Be More Conservative With Atea ASA's (OB:ATEA) CEO Compensation For Now

Key Insights

- Atea will host its Annual General Meeting on 25th of April

- CEO Steinar Sonsteby's total compensation includes salary of kr5.50m

- Total compensation is 59% above industry average

- Atea's EPS grew by 10% over the past three years while total shareholder loss over the past three years was 5.1%

In the past three years, shareholders of Atea ASA (OB:ATEA) have seen a loss on their investment. What is concerning is that despite positive EPS growth, the share price has not tracked the trend in fundamentals. Shareholders may want to question the board on the future direction of the company at the upcoming AGM on 25th of April. Voting on resolutions such as executive remuneration and other matters could also be a way to influence management. Here's our take on why we think shareholders may want to be cautious of approving a raise for the CEO at the moment.

View our latest analysis for Atea

Comparing Atea ASA's CEO Compensation With The Industry

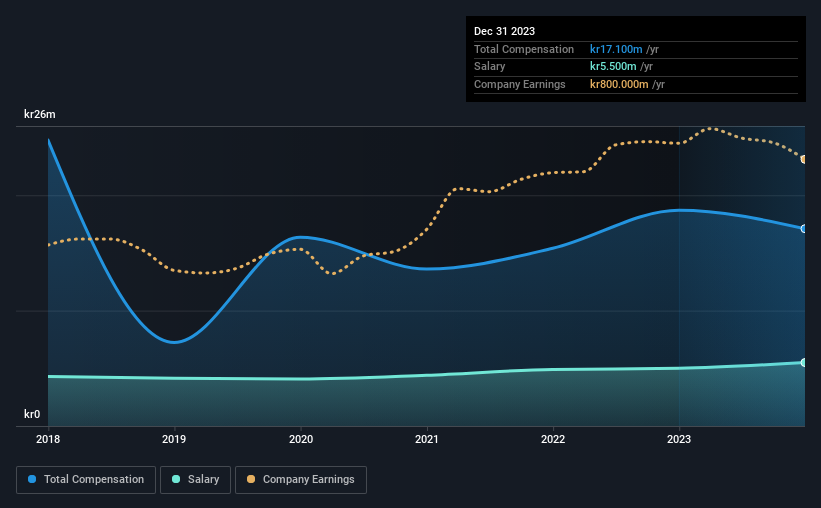

At the time of writing, our data shows that Atea ASA has a market capitalization of kr15b, and reported total annual CEO compensation of kr17m for the year to December 2023. We note that's a decrease of 8.6% compared to last year. We think total compensation is more important but our data shows that the CEO salary is lower, at kr5.5m.

On examining similar-sized companies in the Norwegian IT industry with market capitalizations between kr11b and kr35b, we discovered that the median CEO total compensation of that group was kr11m. Hence, we can conclude that Steinar Sonsteby is remunerated higher than the industry median. Furthermore, Steinar Sonsteby directly owns kr16m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | kr5.5m | kr5.0m | 32% |

| Other | kr12m | kr14m | 68% |

| Total Compensation | kr17m | kr19m | 100% |

On an industry level, roughly 71% of total compensation represents salary and 29% is other remuneration. Atea sets aside a smaller share of compensation for salary, in comparison to the overall industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

Atea ASA's Growth

Atea ASA's earnings per share (EPS) grew 10% per year over the last three years. In the last year, its revenue is up 7.1%.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's good to see a bit of revenue growth, as this suggests the business is able to grow sustainably. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Atea ASA Been A Good Investment?

Since shareholders would have lost about 5.1% over three years, some Atea ASA investors would surely be feeling negative emotions. So shareholders would probably want the company to be less generous with CEO compensation.

In Summary...

The fact that shareholders are sitting on a loss on the value of their shares in the past few years is certainly disconcerting. A huge lag in share price growth when earnings have grown may indicate there could be other issues that are affecting the company at the moment that the market is focused on. If there are some unknown variables that are influencing the stock's price, surely shareholders would have some concerns. These concerns should be addressed at the upcoming AGM, where shareholders can question the board and evaluate if their judgement and decision making is still in line with their expectations.

CEO compensation can have a massive impact on performance, but it's just one element. That's why we did some digging and identified 1 warning sign for Atea that investors should think about before committing capital to this stock.

Important note: Atea is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OB:ATEA

Atea

Provides IT infrastructure and related solutions for businesses and public sector organizations in the Nordic countries and Baltic regions.

High growth potential, good value and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)