Advertisement

- Netherlands

- /

- Banks

- /

- ENXTAM:INGA

Is ING Groep (ENXTAM:INGA) Still Undervalued After Its Strong Recent Share Price Run?

Simply Wall St

Reviewed by Simply Wall St

ING Groep (ENXTAM:INGA) has quietly extended its strong run, with the share price up about 3% over the past month and roughly 10% in the past 3 months, outpacing many European peers.

See our latest analysis for ING Groep.

The latest move takes ING Groep’s share price to $22.71, and sits on top of a powerful year to date, with a roughly 50% share price return and an even stronger one year total shareholder return, suggesting momentum is still building as investors reassess its growth and risk profile.

If ING’s run has you thinking about what else could surprise on the upside, this might be a good moment to explore fast growing stocks with high insider ownership.

With earnings still growing solidly and the shares trading only slightly below analyst targets, yet at a steep discount to some intrinsic estimates, is ING still a compelling buy, or is the market already pricing in its future growth?

Most Popular Narrative Narrative: 18.7% Undervalued

At a last close of €22.71 versus a narrative fair value near €27.92, the story paints ING Groep as meaningfully mispriced, setting up a bolder thesis.

Additionally, ING is among the sector leaders when it comes to try and pivot away from NII as the predominant factor of profits. Instead, the industry in general and the Dutch bankers in particular aim to reap an ever higher share of income from fees for various services, be it client wealth management, M&A activities, debt underwriting etc. The past quarter demonstrates that ING has made ground in this effort at exactly the right time, while still standing to profit from the aforementioned EU investment initiative.

According to PittTheYounger, this valuation leans on a powerful mix of faster revenue expansion, rising profitability, and a richer earnings multiple than typical European banks. Want to see the exact levers behind that price?

Result: Fair Value of €27.92 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, several risks could challenge this view, including a sharper than expected rate cutting cycle and political or regulatory shocks that compress bank profitability.

Find out about the key risks to this ING Groep narrative.

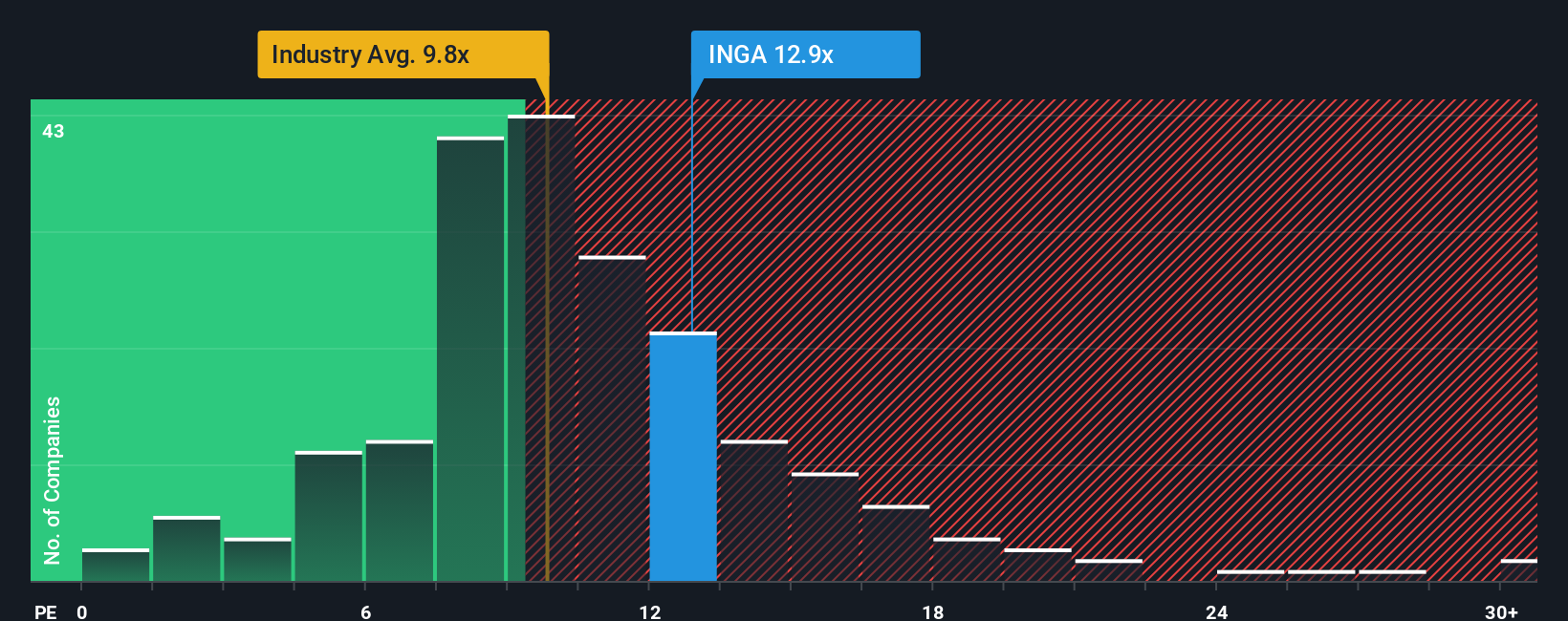

Another View: Earnings Multiple Sends a Caution Flag

On earnings, the picture is less generous. ING trades at about 13.2 times profits versus roughly 10.3 for European banks and a fair ratio of 13. This suggests the share price already bakes in better performance and leaves less room for error if growth cools.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own ING Groep Narrative

If you see the story differently or prefer hands-on analysis, you can quickly build a personalized take in just a few minutes: Do it your way.

A great starting point for your ING Groep research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for your next smart move?

Do not stop with a single idea when you can scan powerful opportunities using the Simply Wall Street Screener, tailored to the themes serious investors actually care about.

- Secure your income goals by reviewing these 15 dividend stocks with yields > 3% that could strengthen your portfolio’s cash flow in the years ahead.

- Ride structural growth trends by focusing on these 30 healthcare AI stocks positioned at the intersection of medicine and cutting edge technology.

- Position yourself early in emerging themes by monitoring these 81 cryptocurrency and blockchain stocks shaping the future of digital assets and blockchain infrastructure.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTAM:INGA

ING Groep

Provides various banking products and services in the Netherlands, Belgium, Germany, rest of Europe, and internationally.

Solid track record with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

44 followersusers have followed this narrative

6 commentsusers have commented on this narrative

15 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.8% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$247.5% overvalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.8% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.8% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Alphabet ·

Positioned globally, partnered locally

Fair Value:US$390.1918.6% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.7% undervalued

956 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

AN

AnalystConsensusTarget on Alphabet ·

GOOGL: AI Platform Expansion And Cloud Demand Will Support Durable Performance Amid Competitive Pressures

Fair Value:US$323.71.9% undervalued

1342 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative