Is Rhone Ma Holdings Berhad (KLSE:RHONEMA) A Risky Investment?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Rhone Ma Holdings Berhad (KLSE:RHONEMA) makes use of debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Rhone Ma Holdings Berhad

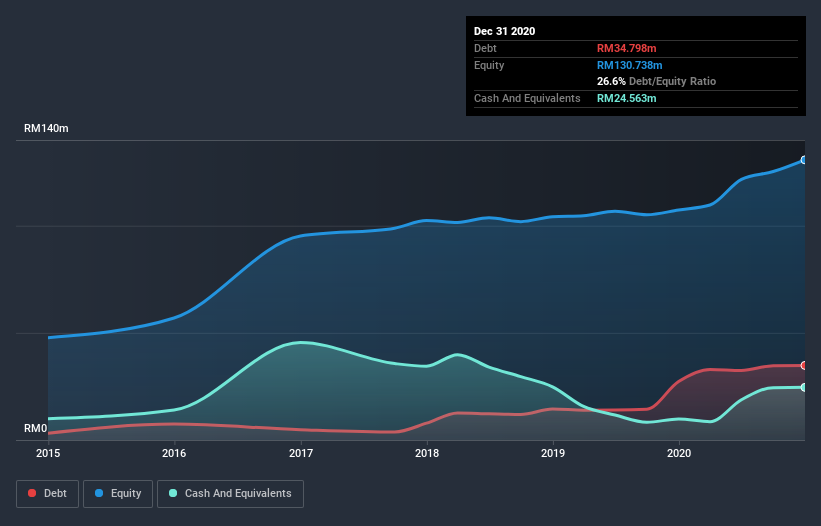

How Much Debt Does Rhone Ma Holdings Berhad Carry?

As you can see below, at the end of December 2020, Rhone Ma Holdings Berhad had RM34.8m of debt, up from RM27.3m a year ago. Click the image for more detail. However, it also had RM24.6m in cash, and so its net debt is RM10.2m.

How Strong Is Rhone Ma Holdings Berhad's Balance Sheet?

We can see from the most recent balance sheet that Rhone Ma Holdings Berhad had liabilities of RM23.9m falling due within a year, and liabilities of RM31.5m due beyond that. Offsetting this, it had RM24.6m in cash and RM33.4m in receivables that were due within 12 months. So it actually has RM2.58m more liquid assets than total liabilities.

Having regard to Rhone Ma Holdings Berhad's size, it seems that its liquid assets are well balanced with its total liabilities. So it's very unlikely that the RM142.6m company is short on cash, but still worth keeping an eye on the balance sheet.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

With net debt sitting at just 0.64 times EBITDA, Rhone Ma Holdings Berhad is arguably pretty conservatively geared. And it boasts interest cover of 9.8 times, which is more than adequate. Also good is that Rhone Ma Holdings Berhad grew its EBIT at 11% over the last year, further increasing its ability to manage debt. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Rhone Ma Holdings Berhad will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we always check how much of that EBIT is translated into free cash flow. During the last three years, Rhone Ma Holdings Berhad burned a lot of cash. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

Based on what we've seen Rhone Ma Holdings Berhad is not finding it easy, given its conversion of EBIT to free cash flow, but the other factors we considered give us cause to be optimistic. There's no doubt that its ability to to cover its interest expense with its EBIT is pretty flash. Considering this range of data points, we think Rhone Ma Holdings Berhad is in a good position to manage its debt levels. Having said that, the load is sufficiently heavy that we would recommend any shareholders keep a close eye on it. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 5 warning signs for Rhone Ma Holdings Berhad (1 is a bit concerning) you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you decide to trade Rhone Ma Holdings Berhad, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:RHONEMA

Rhone Ma Holdings Berhad

An investment holding company, engages in the manufacture, trading, marketing, and distribution of biotechnology and animal health products primarily in Malaysia.

Flawless balance sheet with proven track record.

Similar Companies

Market Insights

Community Narratives