Advertisement

- Malaysia

- /

- Consumer Durables

- /

- KLSE:LIIHEN

Revenue Beat: Lii Hen Industries Bhd Exceeded Revenue Forecasts By 6.2% And Analysts Are Updating Their Estimates

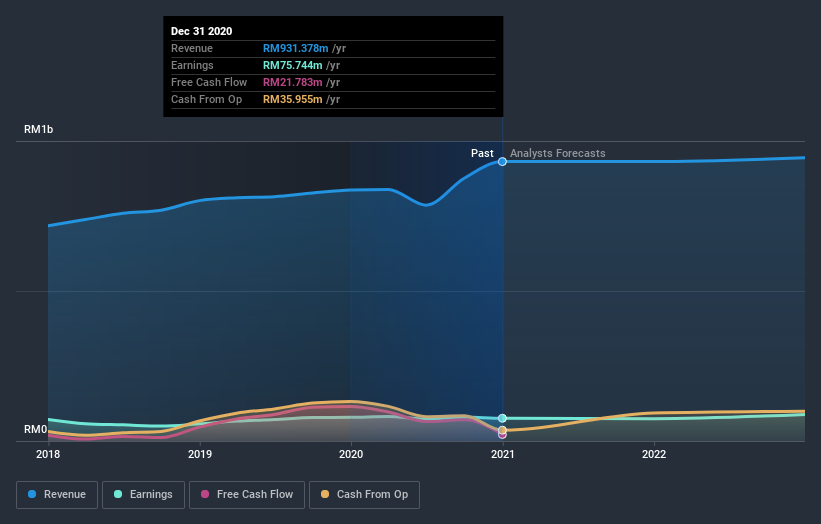

Shareholders might have noticed that Lii Hen Industries Bhd (KLSE:LIIHEN) filed its full-year result this time last week. The early response was not positive, with shares down 7.9% to RM3.74 in the past week. Results overall were respectable, with statutory earnings of RM0.42 per share roughly in line with what the analyst had forecast. Revenues of RM931m came in 6.2% ahead of analyst predictions. The analyst typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. We've gathered the most recent statutory forecasts to see whether the analyst has changed their earnings models, following these results.

Check out our latest analysis for Lii Hen Industries Bhd

Taking into account the latest results, Lii Hen Industries Bhd's sole analyst currently expect revenues in 2021 to be RM931.4m, approximately in line with the last 12 months. Statutory earnings per share are forecast to dip 5.4% to RM0.40 in the same period. In the lead-up to this report, the analyst had been modelling revenues of RM903.5m and earnings per share (EPS) of RM0.47 in 2021. So it's pretty clear the analyst has mixed opinions on Lii Hen Industries Bhd after the latest results; even though they upped their revenue numbers, it came at the cost of a real cut to per-share earnings expectations.

The consensus price target fell 16% to RM4.18, suggesting that the analyst are primarily focused on earnings as the driver of value for this business.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. We would highlight that Lii Hen Industries Bhd's revenue growth is expected to slow, with forecast 0.002% increase next year well below the historical 9.0%p.a. growth over the last five years. Compare this against other companies (with analyst forecasts) in the industry, which are in aggregate expected to see revenue growth of 7.5% next year. Factoring in the forecast slowdown in growth, it seems obvious that Lii Hen Industries Bhd is also expected to grow slower than other industry participants.

The Bottom Line

The most important thing to take away is that the analyst downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. Fortunately, they also upgraded their revenue estimates, although our data indicates sales are expected to perform worse than the wider industry. Furthermore, the analyst also cut their price targets, suggesting that the latest news has led to greater pessimism about the intrinsic value of the business.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At least one analyst has provided forecasts out to 2022, which can be seen for free on our platform here.

Plus, you should also learn about the 3 warning signs we've spotted with Lii Hen Industries Bhd (including 1 which is a bit unpleasant) .

When trading Lii Hen Industries Bhd or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:LIIHEN

Lii Hen Industries Bhd

An investment holding company, manufactures and sells furniture in North America, Asia, Oceania, Africa, and Europe.

Flawless balance sheet established dividend payer.

Market Insights

Advertisement

Community Narratives

RIO is poised to weather a depressed iron ore environment, but commodity diversification comes with lower margins

Fair Value AU$110.51|4.0% overvalued

DU

Community Contributor

The demand for personalized medicine will keep Thermo Fisher Scientific thriving

Fair Value US$540.27|20.1% undervalued

UN

Community Contributor

Silver Play by A Family with 10x Potential

Fair Value UK£24.00|88.5% undervalued

RO

Community Contributor