- South Korea

- /

- Chemicals

- /

- KOSDAQ:A005290

Exploring Three Undiscovered Gems with Promising Potential

Reviewed by Simply Wall St

As global markets navigate a landscape marked by accelerating U.S. inflation and small-cap stocks lagging behind their larger counterparts, investors are keenly observing the shifting dynamics that could present new opportunities. In this environment, identifying stocks with strong fundamentals, innovative potential, and resilience to economic fluctuations can be crucial for uncovering promising investment prospects.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Sugar Terminals | NA | 3.14% | 3.53% | ★★★★★★ |

| Yuen Foong Yu Consumer Products | 27.23% | 0.46% | -3.46% | ★★★★★★ |

| Wilson Bank Holding | NA | 7.87% | 8.22% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Sonix TechnologyLtd | NA | -10.07% | -16.54% | ★★★★★★ |

| Pacific Construction | 21.40% | -3.50% | 26.25% | ★★★★★★ |

| First Copper Technology | 17.03% | 3.07% | 19.66% | ★★★★★★ |

| Ve Wong | 11.84% | 0.61% | 3.56% | ★★★★★☆ |

| Steamships Trading | 33.60% | 4.17% | 3.90% | ★★★★★☆ |

| Huang Hsiang Construction | 266.70% | 13.12% | 15.19% | ★★★★☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

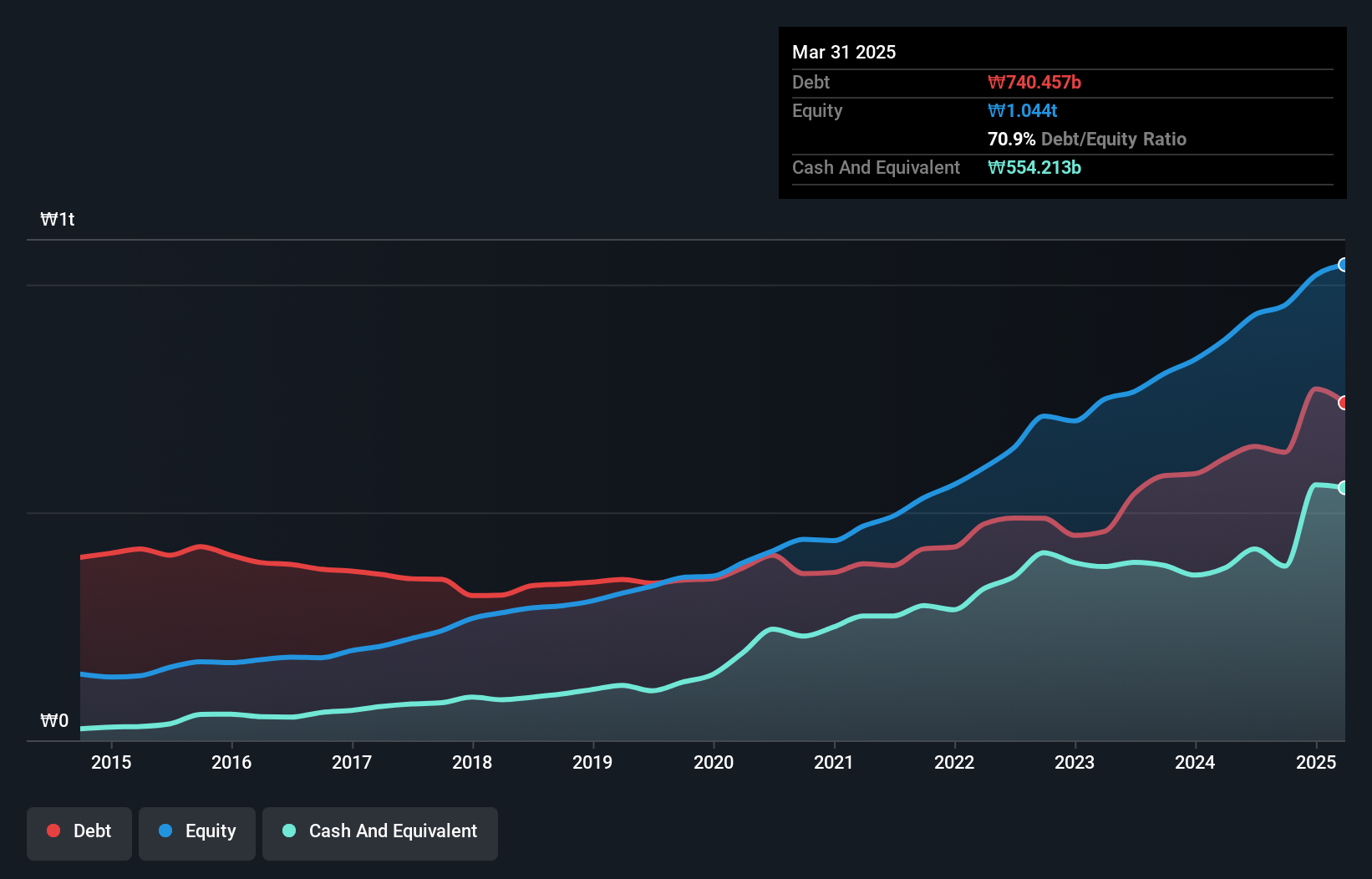

Dongjin Semichem (KOSDAQ:A005290)

Simply Wall St Value Rating: ★★★★★★

Overview: Dongjin Semichem Co., Ltd. manufactures and supplies electronic materials and foaming agents, with a market capitalization of ₩1.41 trillion.

Operations: Dongjin Semichem's primary revenue streams are from South Korea's electronic materials segment, generating ₩949.60 billion, and overseas electronics materials at ₩478.00 billion. The South Korean blowing agent segment contributes ₩93.80 billion, while refined oil in South Korea adds ₩18.12 billion to the revenue mix.

Dongjin Semichem, a nimble player in the chemicals sector, has shown notable financial resilience. Over the past five years, its earnings have grown at an annual rate of 17.1%, although last year's growth of 9.5% lagged behind the industry's 20.9%. The company's debt-to-equity ratio has improved significantly from 98.4% to 66.2%, reflecting prudent financial management. Despite not being free cash flow positive recently, Dongjin's interest payments are well-covered by EBIT at a comfortable 11.6x coverage ratio, and it trades at a substantial discount of about 63% below its estimated fair value, suggesting potential upside for investors seeking undervalued opportunities in this space.

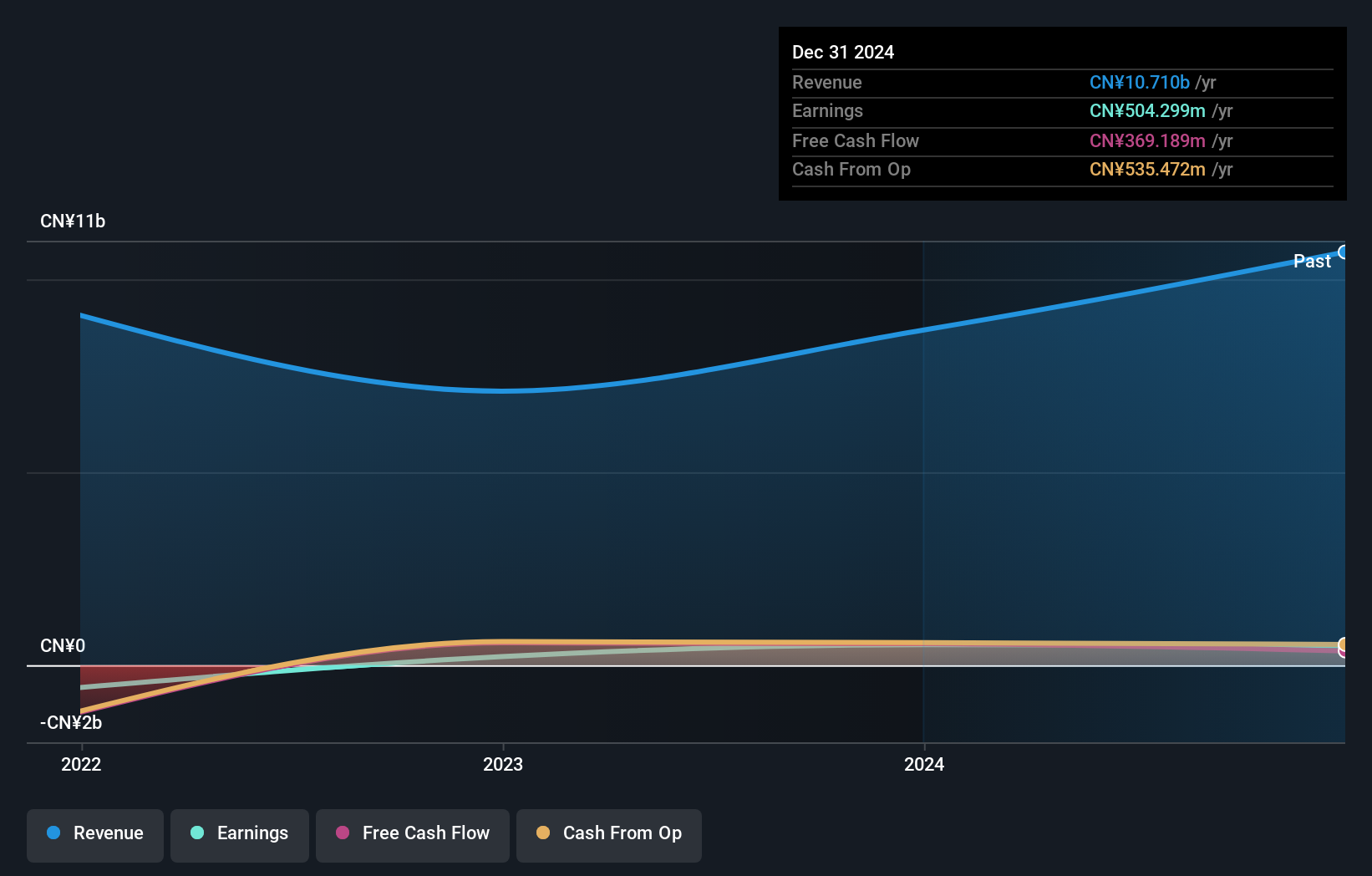

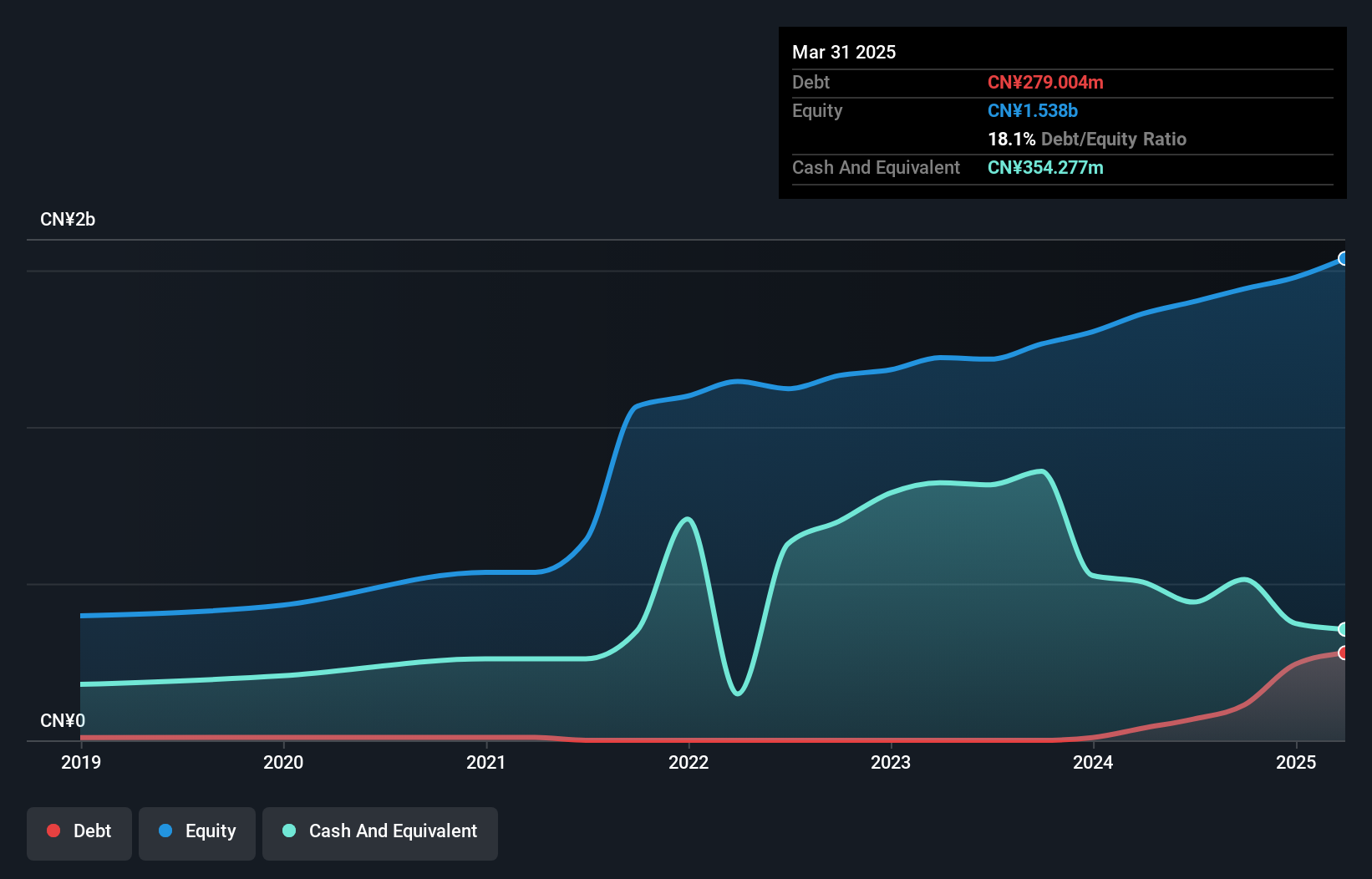

AuGroup (SHENZHEN) Cross-Border Business (SEHK:2519)

Simply Wall St Value Rating: ★★★★★★

Overview: AuGroup (SHENZHEN) Cross-Border Business Co., Ltd. operates in the cross-border trade sector and logistics services, with a market capitalization of approximately HK$5.02 billion.

Operations: The company generates revenue primarily from sales of goods amounting to CN¥7.03 billion and logistic services contributing CN¥2.42 billion.

AuGroup (SHENZHEN) Cross-Border Business has shown impressive growth, with earnings surging by 143% over the past year, significantly outpacing the Specialty Retail industry's -22% performance. The company's financial health appears robust, as its debt-to-equity ratio decreased from 54 to 29 over five years and its interest payments are well-covered by EBIT at an 11.6x coverage. Recently, AuGroup announced a special dividend of RMB 0.25 per share, highlighting shareholder returns. Trading at a notable discount of 41% below estimated fair value, this company seems poised for continued attention in its sector.

- Take a closer look at AuGroup (SHENZHEN) Cross-Border Business' potential here in our health report.

Xiamen East Asia Machinery Industrial (SZSE:301028)

Simply Wall St Value Rating: ★★★★★☆

Overview: Xiamen East Asia Machinery Industrial Co., Ltd. operates in the machinery and industrial equipment sector, with a market capitalization of CN¥4.46 billion.

Operations: The company's revenue primarily stems from the machinery and industrial equipment segment, amounting to CN¥1.12 billion.

Xiamen East Asia Machinery Industrial showcases potential with a price-to-earnings ratio of 20.8x, significantly under the CN market average of 37.4x, indicating a favorable valuation. The company has seen robust earnings growth of 43% over the past year, outpacing its industry peers who experienced minimal change at -0.06%. Despite this positive trajectory, its debt-to-equity ratio has climbed from 2.1% to 7.8% over five years, suggesting increased leverage but is offset by having more cash than total debt and strong interest coverage capability due to earnings exceeding interest obligations comfortably.

Summing It All Up

- Investigate our full lineup of 4711 Undiscovered Gems With Strong Fundamentals right here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSDAQ:A005290

Dongjin Semichem

Manufactures and supplies electronic materials and foaming agents.

Flawless balance sheet with limited growth.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)