Advertisement

- China

- /

- Electrical

- /

- SHSE:688032

3 Growth Companies With High Insider Ownership And Earnings Growth Up To 62%

Simply Wall St

Reviewed by Simply Wall St

In a week marked by global economic shifts, including rate cuts from the ECB and SNB, the Nasdaq Composite stood out by reaching a record high amidst broader market declines. As growth stocks continue to outperform value stocks, driven in part by notable gains in technology giants like Tesla and Alphabet, investors are increasingly focused on companies demonstrating robust insider ownership alongside significant earnings growth. In this context, identifying companies with strong internal stakeholder commitment can be a key indicator of potential resilience and performance amid fluctuating market conditions.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| SKS Technologies Group (ASX:SKS) | 27% | 24.8% |

| On Holding (NYSE:ONON) | 19.1% | 29.4% |

| Medley (TSE:4480) | 34% | 31.7% |

| CD Projekt (WSE:CDR) | 29.7% | 27% |

| Plenti Group (ASX:PLT) | 12.8% | 120.1% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81.5% |

| Brightstar Resources (ASX:BTR) | 16.2% | 84.5% |

| Fine M-TecLTD (KOSDAQ:A441270) | 17.2% | 131.1% |

| Elliptic Laboratories (OB:ELABS) | 26.8% | 111.4% |

| Findi (ASX:FND) | 34.8% | 112.9% |

Here's a peek at a few of the choices from the screener.

i-SENS (KOSDAQ:A099190)

Simply Wall St Growth Rating: ★★★★☆☆

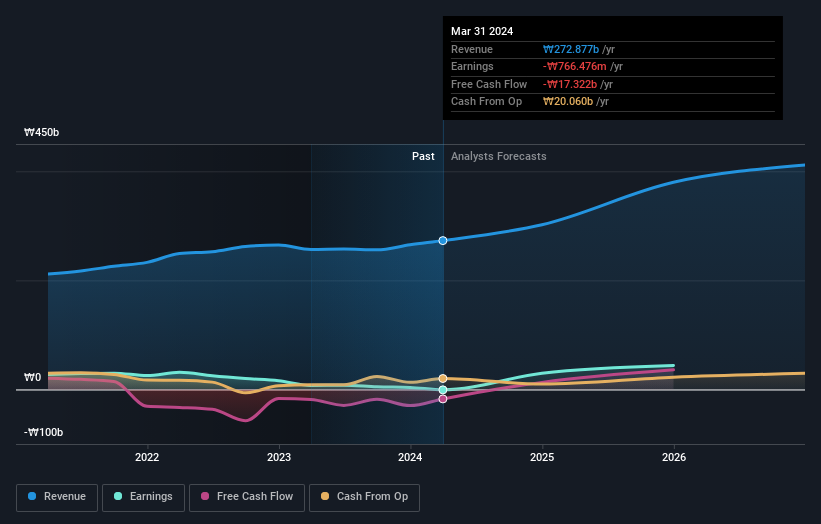

Overview: i-SENS, Inc. develops, manufactures, and sells chemical and biosensors in South Korea and internationally, with a market cap of ₩466.46 billion.

Operations: The company's revenue is primarily derived from its Diagnostic Kits / Equipment segment, totaling ₩284.77 billion.

Insider Ownership: 25%

Earnings Growth Forecast: 62.1% p.a.

i-SENS demonstrates potential as a growth company with high insider ownership, reflected in its recent turnaround from a net loss to a net income of KRW 850.26 million for the third quarter. Despite its low forecasted return on equity (2.9%), earnings are expected to grow significantly at 62.13% annually, with revenue growth projected at 17.9% per year, outpacing the market average of 9%. The stock is trading at good value relative to peers and industry standards.

- Click here to discover the nuances of i-SENS with our detailed analytical future growth report.

- Insights from our recent valuation report point to the potential undervaluation of i-SENS shares in the market.

NOTE (OM:NOTE)

Simply Wall St Growth Rating: ★★★★☆☆

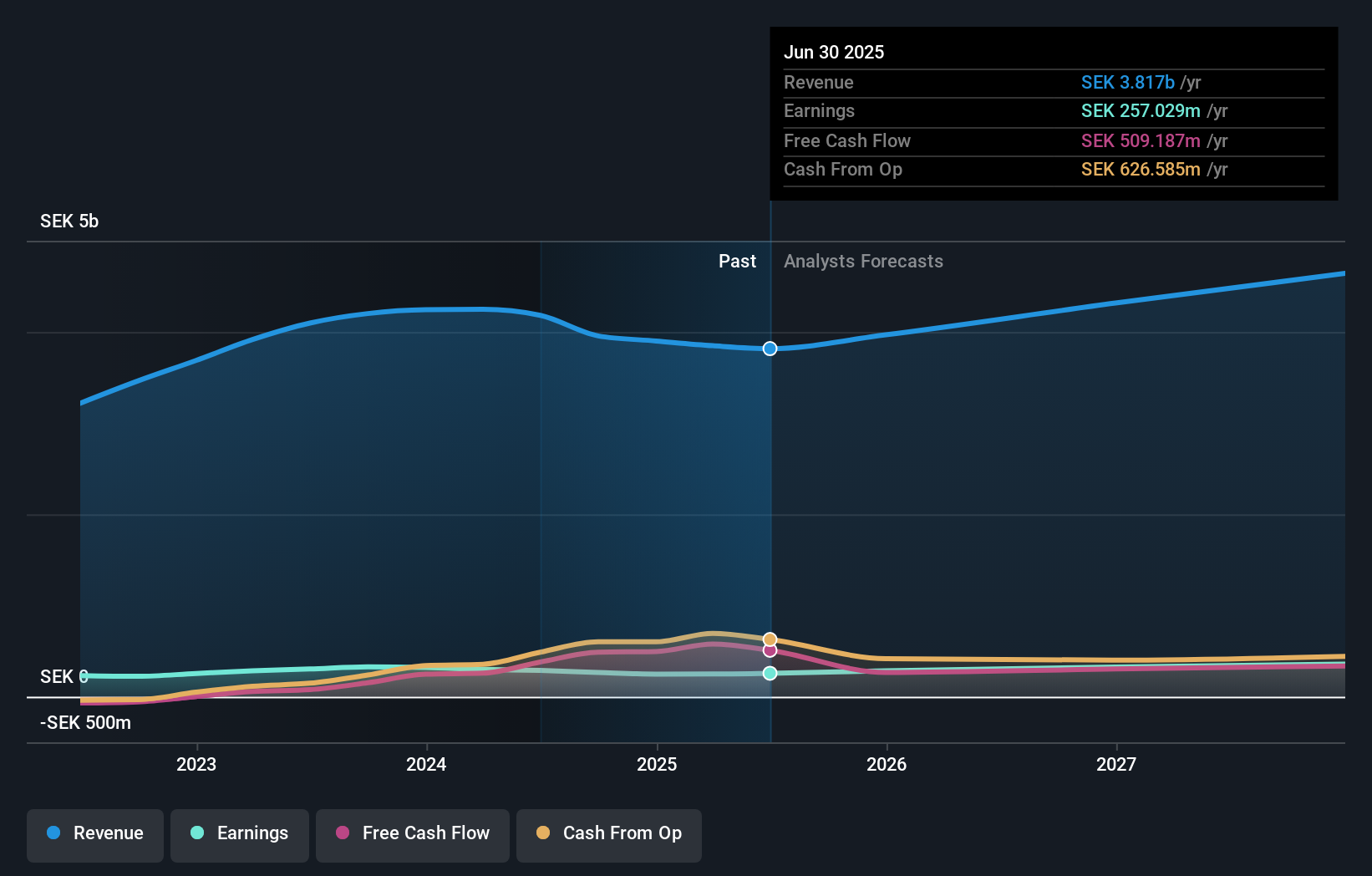

Overview: NOTE AB (publ) is a company that offers electronics manufacturing services across Sweden, Finland, the United Kingdom, Bulgaria, Estonia, China, and internationally with a market cap of SEK4.25 billion.

Operations: The company's revenue segments include SEK988.44 million from the Rest of World and SEK3.02 billion from Western Europe.

Insider Ownership: 25.6%

Earnings Growth Forecast: 20% p.a.

NOTE insiders have shown confidence by purchasing more shares than they sold in the past three months. The company's earnings are expected to grow significantly at 20% annually, outpacing the Swedish market's 15.3% growth rate, despite a forecasted low return on equity of 18.3%. While revenue is projected to grow slower than desired at 11.6%, it still surpasses the Swedish market average of 1.3%. NOTE trades at a good value, being priced below its estimated fair value.

- Delve into the full analysis future growth report here for a deeper understanding of NOTE.

- Our valuation report unveils the possibility NOTE's shares may be trading at a discount.

Hoymiles Power Electronics (SHSE:688032)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Hoymiles Power Electronics Inc. manufactures and sells module level power electronics solutions in China and internationally, with a market cap of CN¥14.74 billion.

Operations: Hoymiles Power Electronics Inc. generates revenue through the production and distribution of module level power electronics solutions both domestically and abroad.

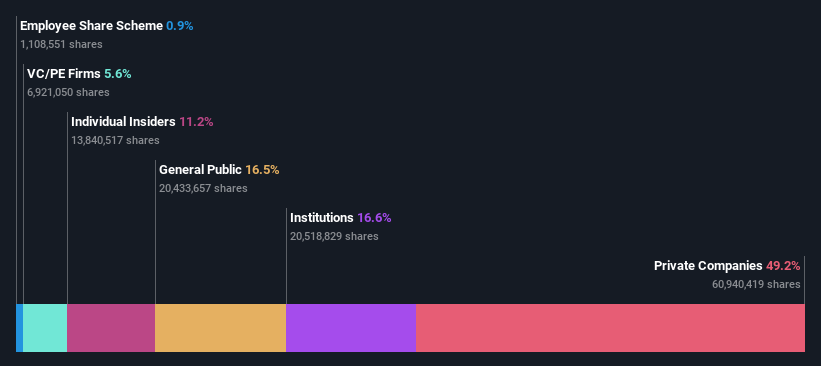

Insider Ownership: 11.2%

Earnings Growth Forecast: 43.1% p.a.

Hoymiles Power Electronics demonstrates potential as a growth company with high insider ownership, despite recent challenges. The company's earnings and revenue are forecast to grow significantly, at 43.1% and 38.2% per year respectively, outpacing the Chinese market averages. However, recent financial results show declining net income and profit margins compared to last year. Analysts generally agree that the stock price will rise by 33.2%, though it remains highly volatile in the short term.

- Get an in-depth perspective on Hoymiles Power Electronics' performance by reading our analyst estimates report here.

- Our valuation report unveils the possibility Hoymiles Power Electronics' shares may be trading at a premium.

Taking Advantage

- Reveal the 1519 hidden gems among our Fast Growing Companies With High Insider Ownership screener with a single click here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Hoymiles Power Electronics might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688032

Hoymiles Power Electronics

Engages in the manufacture and sale of module level power electronics (MLPE) solutions in China and internationally.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

RIO is poised to weather a depressed iron ore environment, but commodity diversification comes with lower margins

Fair Value AU$110.51|3.0% overvalued

DU

Community Contributor

The demand for personalized medicine will keep Thermo Fisher Scientific thriving

Fair Value US$540.27|20.1% undervalued

UN

Community Contributor

Silver Play by A Family with 10x Potential

Fair Value UK£24.00|88.5% undervalued

RO

Community Contributor