Advertisement

- Japan

- /

- Electronic Equipment and Components

- /

- TSE:3323

Weak Financial Prospects Seem To Be Dragging Down Recomm Co., Ltd. (TSE:3323) Stock

With its stock down 11% over the past month, it is easy to disregard Recomm (TSE:3323). We decided to study the company's financials to determine if the downtrend will continue as the long-term performance of a company usually dictates market outcomes. Specifically, we decided to study Recomm's ROE in this article.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

How Do You Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Recomm is:

2.2% = JP¥116m ÷ JP¥5.4b (Based on the trailing twelve months to December 2024).

The 'return' is the amount earned after tax over the last twelve months. So, this means that for every ¥1 of its shareholder's investments, the company generates a profit of ¥0.02.

See our latest analysis for Recomm

What Has ROE Got To Do With Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

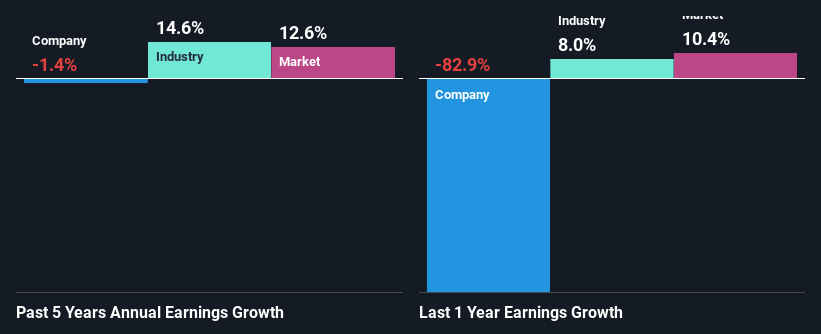

A Side By Side comparison of Recomm's Earnings Growth And 2.2% ROE

It is hard to argue that Recomm's ROE is much good in and of itself. Even when compared to the industry average of 8.2%, the ROE figure is pretty disappointing. As a result, Recomm's flat earnings over the past five years doesn't come as a surprise given its lower ROE.

Next, on comparing with the industry net income growth, we found that the industry grew its earnings by 15% over the last few years.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. This then helps them determine if the stock is placed for a bright or bleak future. If you're wondering about Recomm's's valuation, check out this gauge of its price-to-earnings ratio , as compared to its industry.

Is Recomm Using Its Retained Earnings Effectively?

The high three-year median payout ratio of 54% (meaning, the company retains only 46% of profits) for Recomm suggests that the company's earnings growth was miniscule as a result of paying out a majority of its earnings.

Moreover, Recomm has been paying dividends for nine years, which is a considerable amount of time, suggesting that management must have perceived that the shareholders prefer dividends over earnings growth.

Summary

On the whole, Recomm's performance is quite a big let-down. As a result of its low ROE and lack of much reinvestment into the business, the company has seen a disappointing earnings growth rate. So far, we've only made a quick discussion around the company's earnings growth. You can do your own research on Recomm and see how it has performed in the past by looking at this FREE detailed graph of past earnings, revenue and cash flows.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:3323

Recomm

Recomm Co., Ltd. leases and sells information and communication equipment in Japan and internationally.

Moderate with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

RIO is poised to weather a depressed iron ore environment, but commodity diversification comes with lower margins

Fair Value AU$110.51|4.0% overvalued

DU

Community Contributor

The demand for personalized medicine will keep Thermo Fisher Scientific thriving

Fair Value US$540.27|21.5% undervalued

UN

Community Contributor

Silver Play by A Family with 10x Potential

Fair Value UK£24.00|88.8% undervalued

RO

Community Contributor