3 Japanese Stocks With High Insider Ownership Growing Earnings Up To 79%

Reviewed by Simply Wall St

Japan's stock markets have recently experienced volatility, influenced by political changes and evolving monetary policy stances. Despite these fluctuations, the country's economic landscape continues to present opportunities for growth companies with high insider ownership, as such firms often demonstrate strong alignment between management and shareholder interests—a key factor in navigating uncertain market conditions.

Top 10 Growth Companies With High Insider Ownership In Japan

| Name | Insider Ownership | Earnings Growth |

| Micronics Japan (TSE:6871) | 15.3% | 31.5% |

| Hottolink (TSE:3680) | 26.1% | 61.5% |

| Kasumigaseki CapitalLtd (TSE:3498) | 34.7% | 40.2% |

| Medley (TSE:4480) | 34% | 30.4% |

| Inforich (TSE:9338) | 19.1% | 29.8% |

| Kanamic NetworkLTD (TSE:3939) | 25% | 28.3% |

| ExaWizards (TSE:4259) | 22% | 75.2% |

| Money Forward (TSE:3994) | 21.4% | 68.1% |

| Loadstar Capital K.K (TSE:3482) | 33.8% | 24.3% |

| freee K.K (TSE:4478) | 23.9% | 74.1% |

Let's dive into some prime choices out of the screener.

freee K.K (TSE:4478)

Simply Wall St Growth Rating: ★★★★★☆

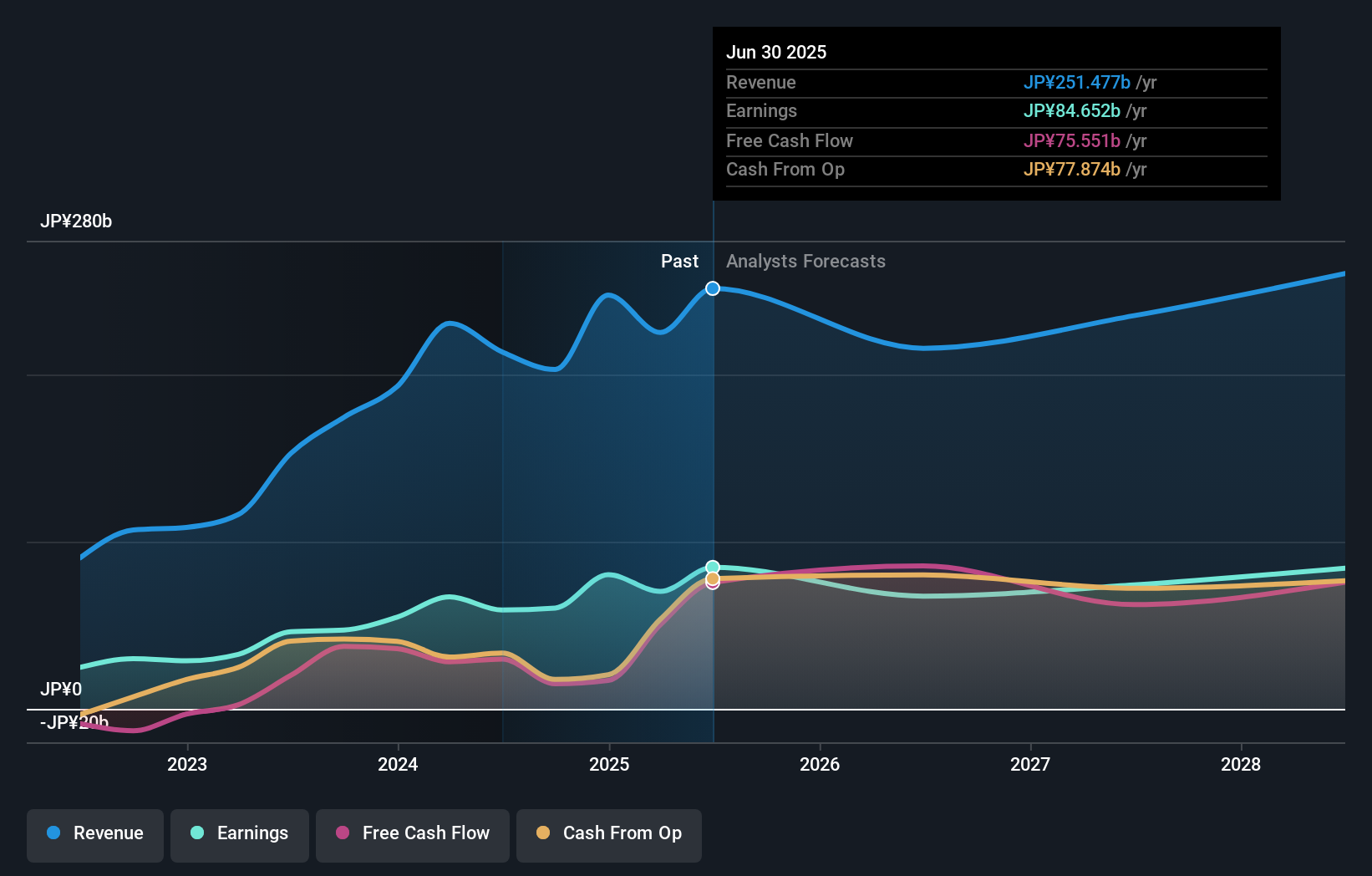

Overview: freee K.K. provides cloud-based accounting and HR software solutions in Japan with a market cap of ¥188.99 billion.

Operations: Revenue Segments (in millions of ¥): The company generates revenue through its cloud-based accounting and HR software solutions in Japan.

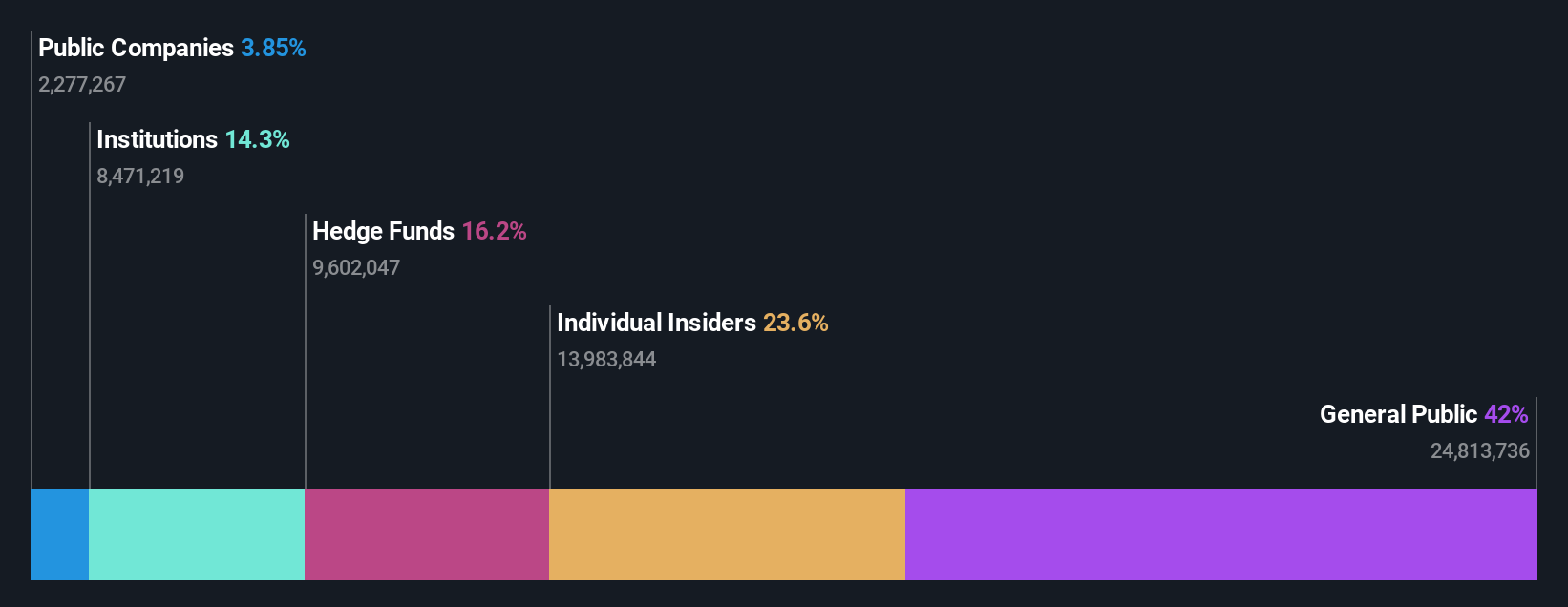

Insider Ownership: 23.9%

Earnings Growth Forecast: 74.1% p.a.

freee K.K. is positioned for significant growth, with earnings projected to increase by 74.08% annually and revenue expected to outpace the Japanese market at 18.2% per year. The stock trades at a substantial discount of 46.8% below its estimated fair value, suggesting potential undervaluation. Recent executive changes include Yasuhiro Kimura's appointment as CPO, indicating strategic shifts in leadership aimed at enhancing product strategies amidst high volatility in share price over the past three months.

- Get an in-depth perspective on freee K.K's performance by reading our analyst estimates report here.

- Upon reviewing our latest valuation report, freee K.K's share price might be too pessimistic.

Rakuten Group (TSE:4755)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Rakuten Group, Inc. operates in e-commerce, fintech, digital content, and communications both in Japan and internationally with a market cap of ¥2.04 trillion.

Operations: The company's revenue is primarily derived from its Internet Services segment at ¥1.24 billion, followed by the Fin Tech segment at ¥772.29 million and the Mobile segment at ¥382.95 million.

Insider Ownership: 17.3%

Earnings Growth Forecast: 79.3% p.a.

Rakuten Group is poised for substantial growth, with earnings forecasted to rise by 79.35% annually and profitability expected within three years, surpassing average market growth. The stock trades at a significant discount of 90.2% below its estimated fair value, indicating potential undervaluation despite recent share price volatility. Revenue is projected to grow at 7.5% per year, faster than the Japanese market's 4.2%, though insider trading activity remains minimal over the past three months.

- Dive into the specifics of Rakuten Group here with our thorough growth forecast report.

- Our valuation report here indicates Rakuten Group may be undervalued.

Lasertec (TSE:6920)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Lasertec Corporation designs, manufactures, and sells inspection and measurement equipment both in Japan and internationally, with a market cap of ¥2.19 trillion.

Operations: Revenue Segments (in millions of ¥): Semiconductor-related products: ¥96,000; Flat panel display-related products: ¥3,500; Other precision equipment: ¥2,500. Lasertec's revenue is primarily derived from semiconductor-related products at ¥96 billion, followed by flat panel display-related products at ¥3.5 billion and other precision equipment at ¥2.5 billion.

Insider Ownership: 11.1%

Earnings Growth Forecast: 15.8% p.a.

Lasertec is experiencing robust growth, with earnings projected to increase by 15.8% annually, outpacing the Japanese market's average. The company recently launched SICA108, enhancing its SiC wafer inspection capabilities crucial for industries like electric vehicles and solar cells. Despite a volatile share price and no recent insider trading activity, Lasertec's high expected return on equity of 41.4% in three years underscores its strong financial performance potential amidst board changes and dividend increases.

- Take a closer look at Lasertec's potential here in our earnings growth report.

- Our valuation report unveils the possibility Lasertec's shares may be trading at a premium.

Next Steps

- Click here to access our complete index of 101 Fast Growing Japanese Companies With High Insider Ownership.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

If you're looking to trade freee K.K, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if freee K.K might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:4478

freee K.K

Engages in the provision of cloud-based accounting and HR software solutions in Japan.

Reasonable growth potential with adequate balance sheet.