- Japan

- /

- Entertainment

- /

- TSE:9697

Capcom Co., Ltd. Just Beat Earnings Expectations: Here's What Analysts Think Will Happen Next

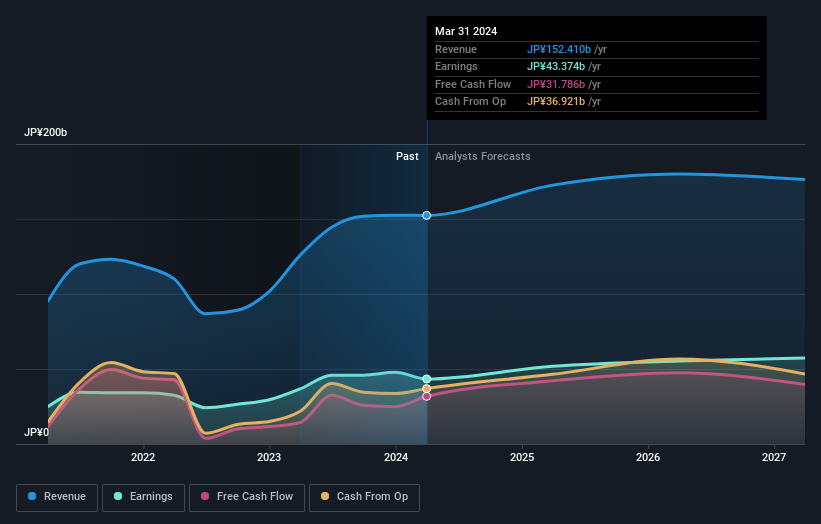

Capcom Co., Ltd. (TSE:9697) just released its latest full-year results and things are looking bullish. It was overall a positive result, with revenues beating expectations by 4.7% to hit JP¥152b. Capcom also reported a statutory profit of JP¥207, which was an impressive 102% above what the analysts had forecast. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

See our latest analysis for Capcom

Taking into account the latest results, the most recent consensus for Capcom from 14 analysts is for revenues of JP¥172.6b in 2025. If met, it would imply a decent 13% increase on its revenue over the past 12 months. Per-share earnings are expected to grow 17% to JP¥122. In the lead-up to this report, the analysts had been modelling revenues of JP¥170.5b and earnings per share (EPS) of JP¥118 in 2025. So the consensus seems to have become somewhat more optimistic on Capcom's earnings potential following these results.

The consensus price target was unchanged at JP¥3,274, implying that the improved earnings outlook is not expected to have a long term impact on value creation for shareholders. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. Currently, the most bullish analyst values Capcom at JP¥3,715 per share, while the most bearish prices it at JP¥2,500. Analysts definitely have varying views on the business, but the spread of estimates is not wide enough in our view to suggest that extreme outcomes could await Capcom shareholders.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. It's clear from the latest estimates that Capcom's rate of growth is expected to accelerate meaningfully, with the forecast 13% annualised revenue growth to the end of 2025 noticeably faster than its historical growth of 10% p.a. over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 4.3% per year. Factoring in the forecast acceleration in revenue, it's pretty clear that Capcom is expected to grow much faster than its industry.

The Bottom Line

The most important thing here is that the analysts upgraded their earnings per share estimates, suggesting that there has been a clear increase in optimism towards Capcom following these results. Fortunately, they also reconfirmed their revenue numbers, suggesting that it's tracking in line with expectations. Additionally, our data suggests that revenue is expected to grow faster than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have estimates - from multiple Capcom analysts - going out to 2027, and you can see them free on our platform here.

You can also see our analysis of Capcom's Board and CEO remuneration and experience, and whether company insiders have been buying stock.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:9697

Capcom

Plans, develops, manufactures, sells, and distributes home video games, online games, mobile games, and arcade games in Japan and internationally.

Outstanding track record with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Stride Stock: Online Education Finds Its Second Act

CS Disco Stock: Legal AI Is Moving From Efficiency Tool to Competitive Necessity

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)