Hokuetsu Corporation's (TSE:3865) investors are due to receive a payment of ¥11.00 per share on 30th of June. Despite this raise, the dividend yield of 1.4% is only a modest boost to shareholder returns.

View our latest analysis for Hokuetsu

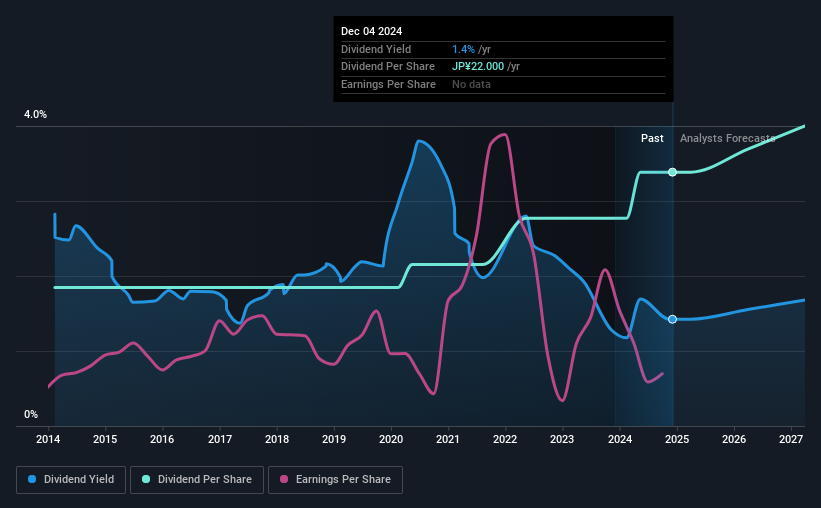

Hokuetsu's Payment Could Potentially Have Solid Earnings Coverage

If it is predictable over a long period, even low dividend yields can be attractive. Before making this announcement, Hokuetsu was easily earning enough to cover the dividend. As a result, a large proportion of what it earned was being reinvested back into the business.

Over the next year, EPS is forecast to expand by 26.2%. If the dividend continues on this path, the payout ratio could be 58% by next year, which we think can be pretty sustainable going forward.

Hokuetsu Has A Solid Track Record

The company has been paying a dividend for a long time, and it has been quite stable which gives us confidence in the future dividend potential. The dividend has gone from an annual total of ¥12.00 in 2014 to the most recent total annual payment of ¥22.00. This works out to be a compound annual growth rate (CAGR) of approximately 6.2% a year over that time. The dividend has been growing very nicely for a number of years, and has given its shareholders some nice income in their portfolios.

The Dividend Has Limited Growth Potential

Some investors will be chomping at the bit to buy some of the company's stock based on its dividend history. However, things aren't all that rosy. Hokuetsu's earnings per share has shrunk at 15% a year over the past five years. This steep decline can indicate that the business is going through a tough time, which could constrain its ability to pay a larger dividend each year in the future. On the bright side, earnings are predicted to gain some ground over the next year, but until this turns into a pattern we wouldn't be feeling too comfortable.

In Summary

In summary, it's great to see that the company can raise the dividend and keep it in a sustainable range. The earnings coverage is acceptable for now, but with earnings on the decline we would definitely keep an eye on the payout ratio. The dividend looks okay, but there have been some issues in the past, so we would be a little bit cautious.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. However, there are other things to consider for investors when analysing stock performance. As an example, we've identified 3 warning signs for Hokuetsu that you should be aware of before investing. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if Hokuetsu might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:3865

Hokuetsu

Manufactures and sells paper products in Japan, the United State, China, rest of Asia, and internationally.

Flawless balance sheet average dividend payer.