Advertisement

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. Although, when we looked at MRSO (TSE:5619), it didn't seem to tick all of these boxes.

What Is Return On Capital Employed (ROCE)?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. Analysts use this formula to calculate it for MRSO:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

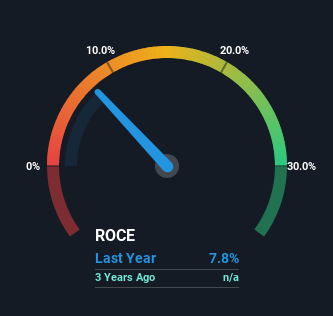

0.078 = JP¥158m ÷ (JP¥2.3b - JP¥234m) (Based on the trailing twelve months to December 2024).

Thus, MRSO has an ROCE of 7.8%. Ultimately, that's a low return and it under-performs the Healthcare Services industry average of 17%.

Check out our latest analysis for MRSO

Historical performance is a great place to start when researching a stock so above you can see the gauge for MRSO's ROCE against it's prior returns. If you're interested in investigating MRSO's past further, check out this free graph covering MRSO's past earnings, revenue and cash flow .

What Can We Tell From MRSO's ROCE Trend?

Over the past , MRSO's ROCE and capital employed have both remained mostly flat. Businesses with these traits tend to be mature and steady operations because they're past the growth phase. So unless we see a substantial change at MRSO in terms of ROCE and additional investments being made, we wouldn't hold our breath on it being a multi-bagger.

The Bottom Line On MRSO's ROCE

In a nutshell, MRSO has been trudging along with the same returns from the same amount of capital over the last . And investors appear hesitant that the trends will pick up because the stock has fallen 41% in the last year. All in all, the inherent trends aren't typical of multi-baggers, so if that's what you're after, we think you might have more luck elsewhere.

If you want to know some of the risks facing MRSO we've found 3 warning signs (1 can't be ignored!) that you should be aware of before investing here.

While MRSO may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:5619

MRSO

Develops and operates medical and health checkup online reservation system for medical facilities in Japan.

Mediocre balance sheet low.

Market Insights

Advertisement

Community Narratives

RIO is poised to weather a depressed iron ore environment, but commodity diversification comes with lower margins

Fair Value AU$110.51|3.0% overvalued

DU

Community Contributor

The demand for personalized medicine will keep Thermo Fisher Scientific thriving

Fair Value US$540.27|19.5% undervalued

UN

Community Contributor

Silver Play by A Family with 10x Potential

Fair Value UK£24.00|88.5% undervalued

RO

Community Contributor