- Japan

- /

- Food and Staples Retail

- /

- TSE:141A

Global Market's Top 3 Stocks Estimated Below Intrinsic Value

Reviewed by Simply Wall St

Amid ongoing trade policy uncertainties and fluctuating economic indicators, global markets have experienced notable volatility, with major indices like the S&P 500 and Nasdaq Composite seeing significant declines. In this climate of cautious investor sentiment, identifying stocks that are trading below their intrinsic value can offer potential opportunities for those seeking to navigate these challenging market conditions.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Laboratorios Farmaceuticos Rovi (BME:ROVI) | €53.80 | €107.22 | 49.8% |

| Absolent Air Care Group (OM:ABSO) | SEK258.00 | SEK510.61 | 49.5% |

| Hyosung Heavy Industries (KOSE:A298040) | ₩422500.00 | ₩844530.57 | 50% |

| Hugel (KOSDAQ:A145020) | ₩322000.00 | ₩641563.00 | 49.8% |

| Storytel (OM:STORY B) | SEK89.70 | SEK177.35 | 49.4% |

| BalnibarbiLtd (TSE:3418) | ¥1090.00 | ¥2172.97 | 49.8% |

| Sung Kwang BendLtd (KOSDAQ:A014620) | ₩27700.00 | ₩55174.11 | 49.8% |

| ASMPT (SEHK:522) | HK$58.15 | HK$115.96 | 49.9% |

| Zhejiang Leapmotor Technology (SEHK:9863) | HK$41.75 | HK$82.70 | 49.5% |

| Doosan Fuel Cell (KOSE:A336260) | ₩15970.00 | ₩31552.20 | 49.4% |

Let's dive into some prime choices out of the screener.

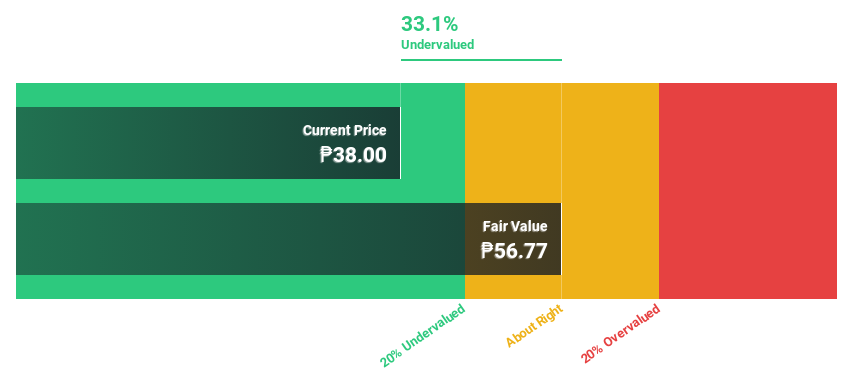

DigiPlus Interactive (PSE:PLUS)

Overview: DigiPlus Interactive Corp. operates general amusement, recreation enterprises, hotels, and gaming facilities in the Philippines through its subsidiaries, with a market capitalization of ₱163.30 billion.

Operations: The company's revenue segments include the Casino Group at ₱501.05 million, the Retail Group at ₱61.84 billion, the Property Group at ₱82.19 million, and the Network and License Group at ₱402.91 million.

Estimated Discount To Fair Value: 35.2%

DigiPlus Interactive is trading at ₱37.05, significantly below its estimated fair value of ₱57.9, suggesting undervaluation based on cash flows. Despite revenue growth forecasts of 15.3% annually, which is slower than some benchmarks but faster than the Philippine market average, earnings are expected to grow at 19.7% per year—outpacing the market's 10.5%. Recent strategic expansions into Singapore aim to bolster international growth and leverage global connectivity for long-term success.

- Our comprehensive growth report raises the possibility that DigiPlus Interactive is poised for substantial financial growth.

- Take a closer look at DigiPlus Interactive's balance sheet health here in our report.

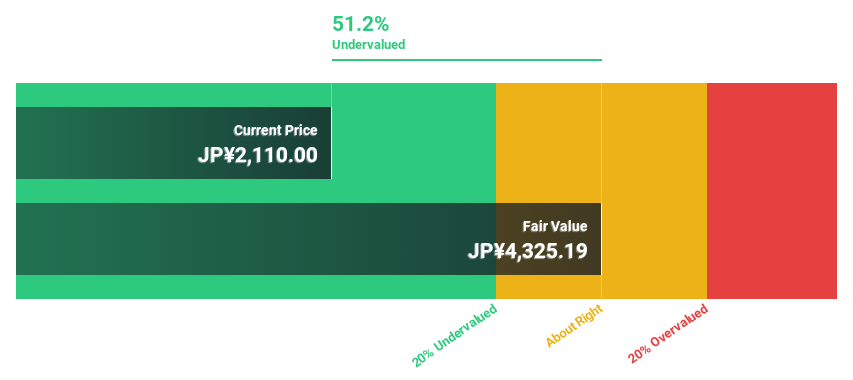

Trial Holdings (TSE:141A)

Overview: Trial Holdings Inc. operates in the retail, logistics, financial and payment services, and retail tech sectors with a market cap of ¥244.25 billion.

Operations: The company's revenue primarily comes from its Distribution and Retail segment, which generated ¥754.69 billion, while the Retail AI segment contributed ¥4.51 billion.

Estimated Discount To Fair Value: 47.5%

Trial Holdings is trading at ¥2208, considerably below its fair value estimate of ¥4203.24, highlighting potential undervaluation based on cash flows. Despite a highly volatile share price recently, earnings are forecast to grow significantly at 21.4% per year, outpacing the JP market's 8%. Recent sales figures show robust growth with all store sales increasing over 111% year-over-year. The board is considering acquiring Seiyu Co., Ltd., potentially enhancing future revenue streams.

- Our expertly prepared growth report on Trial Holdings implies its future financial outlook may be stronger than recent results.

- Click to explore a detailed breakdown of our findings in Trial Holdings' balance sheet health report.

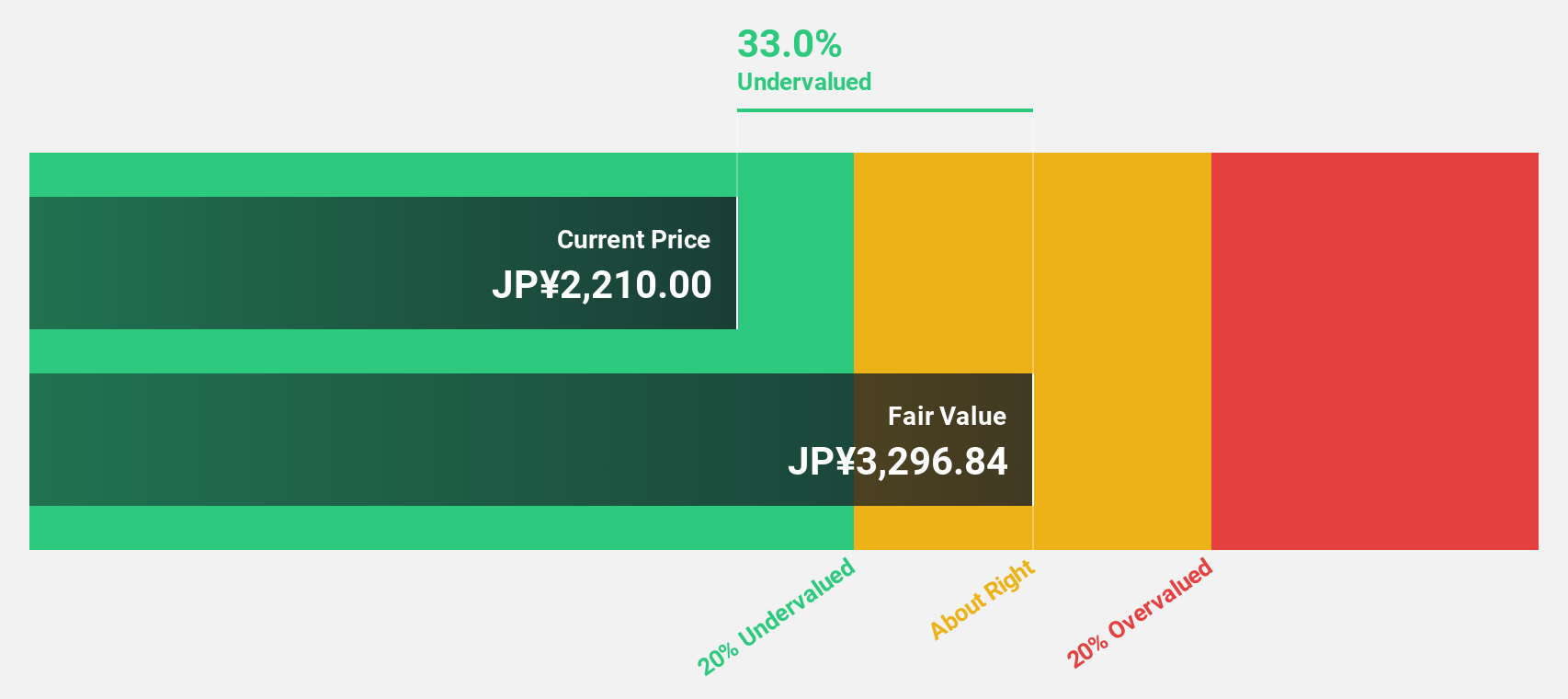

COVER (TSE:5253)

Overview: COVER Corporation operates in the virtual platform, VTuber production, and media mix sectors with a market cap of ¥175.50 billion.

Operations: The company generates revenue through its virtual platform, VTuber production, and media mix businesses.

Estimated Discount To Fair Value: 10.5%

COVER is trading at ¥2952, slightly below its estimated fair value of ¥3298.94, indicating potential undervaluation. The company's earnings are forecast to grow significantly at 24.7% annually, surpassing the JP market's 8%. Although revenue growth is expected to be moderate at 17.2% per year, it remains above the market average of 4.2%. Despite recent share price volatility, COVER's robust earnings outlook positions it well for future growth based on cash flows.

- The growth report we've compiled suggests that COVER's future prospects could be on the up.

- Get an in-depth perspective on COVER's balance sheet by reading our health report here.

Key Takeaways

- Take a closer look at our Undervalued Global Stocks Based On Cash Flows list of 507 companies by clicking here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Trial Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:141A

Trial Holdings

Operates in the retail, logistics, financial / payment services, and retail tech businesses.

Reasonable growth potential with adequate balance sheet.