- Japan

- /

- Trade Distributors

- /

- TSE:8093

3 Dividend Stocks To Consider With Up To 4.2% Yield

Reviewed by Simply Wall St

In recent weeks, global markets have experienced volatility due to tariff uncertainties and mixed economic data, with U.S. stocks ending lower despite some positive earnings reports. As investors navigate these complex conditions, dividend stocks can offer a measure of stability and income potential, making them an attractive option for those looking to balance risk in their portfolios amidst ongoing market fluctuations.

Top 10 Dividend Stocks

| Name | Dividend Yield | Dividend Rating |

| Wuliangye YibinLtd (SZSE:000858) | 3.93% | ★★★★★★ |

| Padma Oil (DSE:PADMAOIL) | 7.54% | ★★★★★★ |

| Tsubakimoto Chain (TSE:6371) | 4.33% | ★★★★★★ |

| Nihon Parkerizing (TSE:4095) | 3.85% | ★★★★★★ |

| GakkyushaLtd (TSE:9769) | 4.45% | ★★★★★★ |

| CAC Holdings (TSE:4725) | 4.11% | ★★★★★★ |

| China South Publishing & Media Group (SHSE:601098) | 3.90% | ★★★★★★ |

| HUAYU Automotive Systems (SHSE:600741) | 4.28% | ★★★★★★ |

| DoshishaLtd (TSE:7483) | 3.85% | ★★★★★★ |

| FALCO HOLDINGS (TSE:4671) | 6.54% | ★★★★★★ |

Click here to see the full list of 1972 stocks from our Top Dividend Stocks screener.

Let's explore several standout options from the results in the screener.

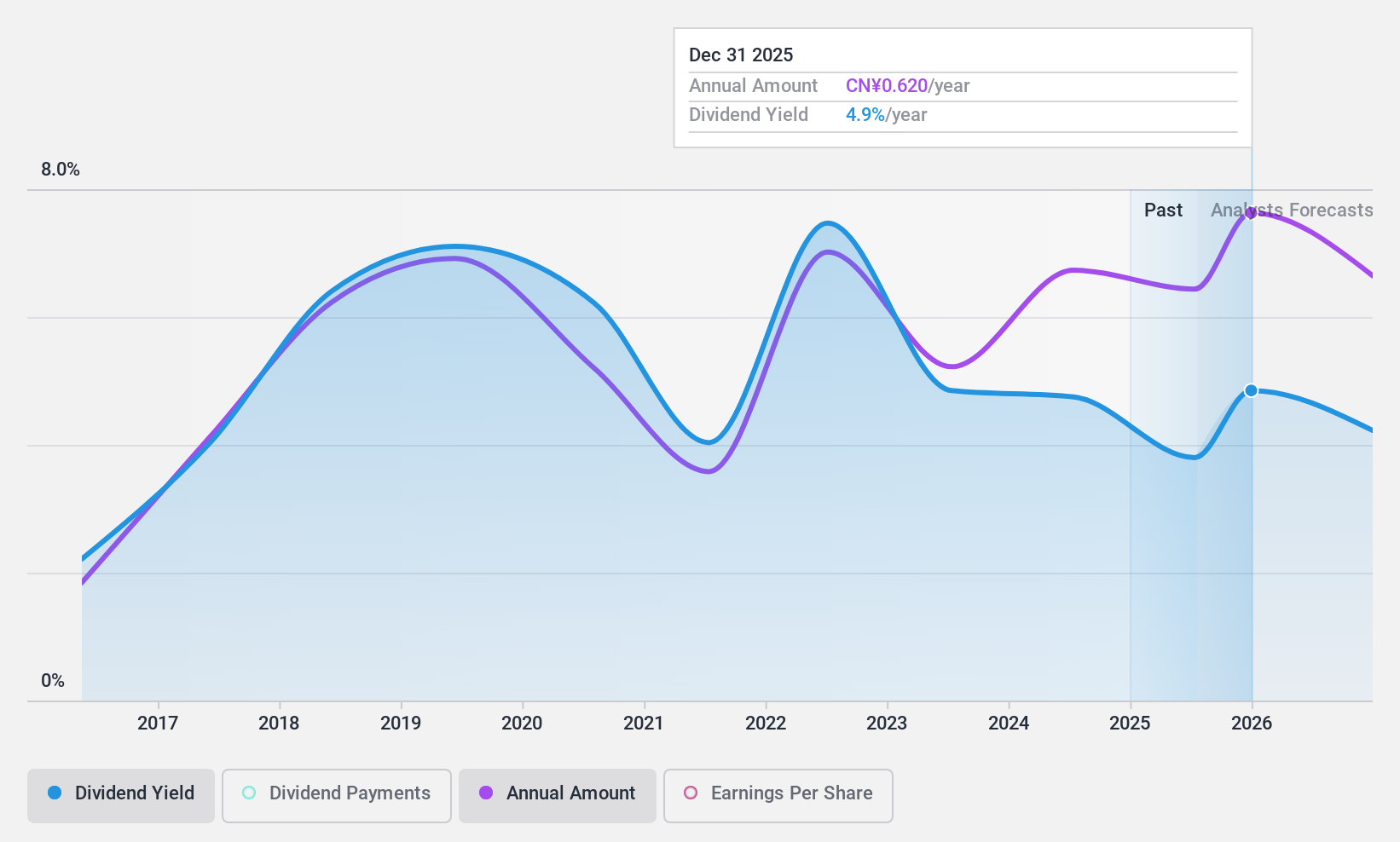

Guangdong Provincial Expressway Development (SZSE:000429)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Guangdong Provincial Expressway Development Co., Ltd. operates expressways and bridges in China and has a market cap of CN¥24.74 billion.

Operations: The company's revenue segments include income from expressway tolls amounting to CN¥5.32 billion and bridge tolls totaling CN¥1.89 billion.

Dividend Yield: 4.2%

Guangdong Provincial Expressway Development offers a dividend yield of 4.21%, placing it in the top 25% of CN market payers. However, its dividends are not well covered by free cash flows, with a high cash payout ratio of 99.3%. Despite earnings growth and a reasonable payout ratio of 70.1%, the dividends have been volatile and unreliable over the past decade, raising concerns about sustainability for dividend investors.

- Get an in-depth perspective on Guangdong Provincial Expressway Development's performance by reading our dividend report here.

- Our valuation report here indicates Guangdong Provincial Expressway Development may be overvalued.

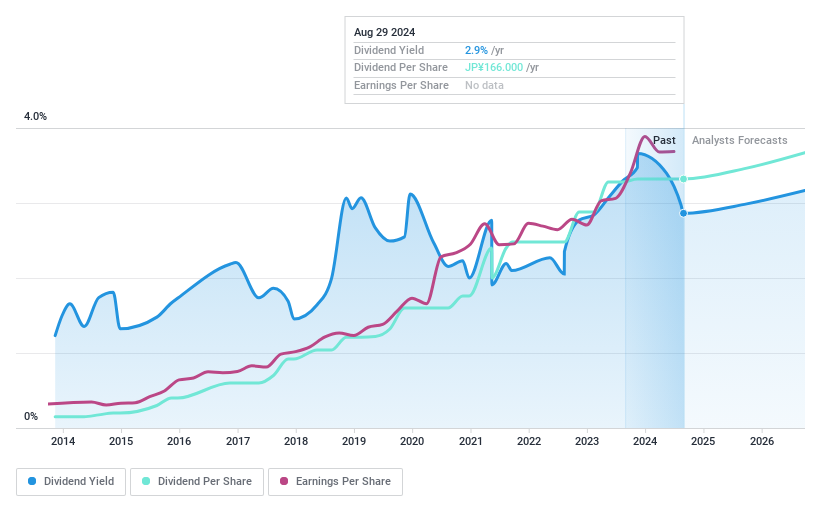

Open House Group (TSE:3288)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Open House Group Co., Ltd. operates in the real estate and other businesses with a market cap of ¥592.38 billion.

Operations: Open House Group Co., Ltd. generates revenue from several segments, including Single-Family Homes at ¥590.17 billion, Profitable Real Estate Business at ¥196.56 billion, Pressance Corporation at ¥180.85 billion, Meldia at ¥140.52 billion, and the Condominium Business at ¥89.29 billion.

Dividend Yield: 3.1%

Open House Group's dividends have been stable and reliable over the past decade, with a payout ratio of 21.2% covered by earnings and a cash payout ratio of 19.7%. Despite a lower dividend yield of 3.1% compared to top-tier JP market payers, its low Price-To-Earnings ratio (6.8x) suggests good value relative to the market average. Recent strategic moves include acquiring Pressance Corporation and securing JPY 10 billion in debt financing for business expansion, potentially impacting future dividend policies.

- Delve into the full analysis dividend report here for a deeper understanding of Open House Group.

- Upon reviewing our latest valuation report, Open House Group's share price might be too pessimistic.

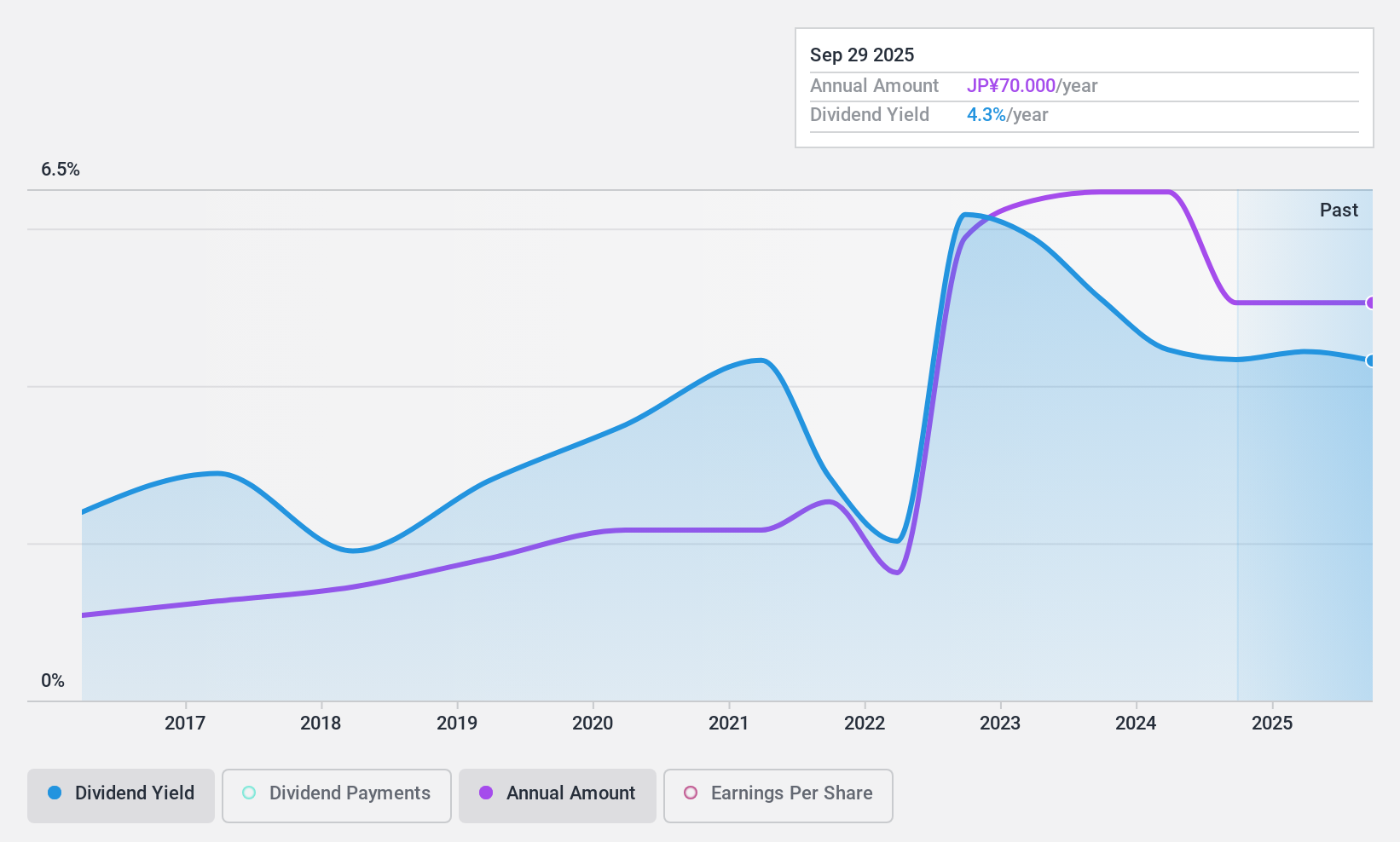

Kyokuto Boeki Kaisha (TSE:8093)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Kyokuto Boeki Kaisha, Ltd. is an engineering trading company operating both in Japan and internationally with a market cap of ¥19.35 billion.

Operations: Kyokuto Boeki Kaisha, Ltd. generates revenue from its Industrial Material Departments (¥13.99 billion), Machine Part Related Department (¥18.69 billion), and Industrial Equipment Related Departments (¥13.14 billion).

Dividend Yield: 4.2%

Kyokuto Boeki Kaisha's dividend yield of 4.22% ranks it among the top 25% of dividend payers in Japan, but its dividends have been volatile and unreliable over the past decade. The company's payout ratio is 76.9%, indicating coverage by earnings, though not by free cash flow, raising sustainability concerns. A recent share repurchase program worth ¥500 million aims to enhance shareholder returns and capital efficiency, potentially impacting future dividend stability positively.

- Click here and access our complete dividend analysis report to understand the dynamics of Kyokuto Boeki Kaisha.

- Our comprehensive valuation report raises the possibility that Kyokuto Boeki Kaisha is priced higher than what may be justified by its financials.

Seize The Opportunity

- Explore the 1972 names from our Top Dividend Stocks screener here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Kyokuto Boeki Kaisha might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:8093

Kyokuto Boeki Kaisha

Primarily operates as an engineering trading company in Japan and internationally.

Flawless balance sheet established dividend payer.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Salesforce Stock: AI-Fueled Growth Is Real — But Can Margins Stay This Strong?

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)