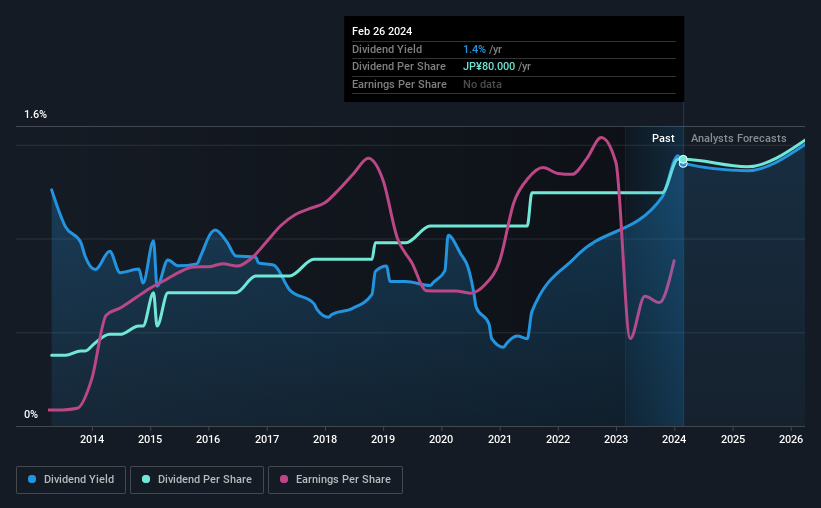

Nidec Corporation (TSE:6594) will increase its dividend from last year's comparable payment on the 3rd of June to ¥40.00. This takes the annual payment to 1.4% of the current stock price, which unfortunately is below what the industry is paying.

Check out our latest analysis for Nidec

Nidec's Earnings Easily Cover The Distributions

If it is predictable over a long period, even low dividend yields can be attractive. The last dividend was quite easily covered by Nidec's earnings. This means that a large portion of its earnings are being retained to grow the business.

Over the next year, EPS is forecast to expand by 158.9%. If the dividend continues on this path, the payout ratio could be 21% by next year, which we think can be pretty sustainable going forward.

Nidec Has A Solid Track Record

The company has a sustained record of paying dividends with very little fluctuation. Since 2014, the annual payment back then was ¥21.25, compared to the most recent full-year payment of ¥80.00. This implies that the company grew its distributions at a yearly rate of about 14% over that duration. We can see that payments have shown some very nice upward momentum without faltering, which provides some reassurance that future payments will also be reliable.

Dividend Growth Is Doubtful

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. Let's not jump to conclusions as things might not be as good as they appear on the surface. Nidec has seen earnings per share falling at 7.6% per year over the last five years. A modest decline in earnings isn't great, and it makes it quite unlikely that the dividend will grow in the future unless that trend can be reversed. Earnings are forecast to grow over the next 12 months and if that happens we could still be a little bit cautious until it becomes a pattern.

Our Thoughts On Nidec's Dividend

In summary, it's great to see that the company can raise the dividend and keep it in a sustainable range. While the payments look sustainable for now, earnings have been shrinking so the dividend could come under pressure in the future. This looks like it could be a good dividend stock going forward, but we would note that the payout ratio has been at higher levels in the past so it could happen again.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. For instance, we've picked out 1 warning sign for Nidec that investors should take into consideration. Is Nidec not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Nidec might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6594

Nidec

Develops, manufactures, and sells motors, electronics and optical components, and other related products in Japan and internationally.

Flawless balance sheet with solid track record and pays a dividend.

Similar Companies

Market Insights

Community Narratives