Advertisement

Undiscovered Gems With Strong Fundamentals For December 2024

Simply Wall St

Reviewed by Simply Wall St

As global markets continue to rally, with U.S. small-cap indices like the Russell 2000 reaching new highs, investors are closely monitoring economic indicators that suggest robust consumer spending despite a manufacturing slump. In this dynamic environment, identifying stocks with strong fundamentals becomes crucial as they can offer resilience and potential growth amid geopolitical uncertainties and shifting domestic policies.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Bahrain National Holding Company B.S.C | NA | 20.11% | 5.44% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Standard Bank | 0.13% | 27.78% | 30.36% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| HOMAG Group | NA | -31.14% | 23.43% | ★★★★★☆ |

| Pure Cycle | 5.31% | -4.44% | -5.74% | ★★★★★☆ |

| Arab Banking Corporation (B.S.C.) | 213.15% | 18.58% | 29.63% | ★★★★☆☆ |

| Wilson | 64.79% | 30.09% | 68.29% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Invest Bank | 135.69% | 11.07% | 18.67% | ★★★★☆☆ |

We'll examine a selection from our screener results.

Fujian Start GroupLtd (SHSE:600734)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Fujian Start Group Co. Ltd specializes in providing anti-intrusion detection systems in China, with a market cap of CN¥8.99 billion.

Operations: The company generates revenue primarily through its anti-intrusion detection systems in China. It has a market cap of CN¥8.99 billion, reflecting its position in the industry.

Fujian Start Group, a smaller player in the tech industry, has shown impressive earnings growth of 533% over the past year, outpacing the industry's 7%. Despite sales dropping to CNY 63.49 million from CNY 207.82 million last year, net income rose to CNY 36.55 million from CNY 18.43 million, indicating improved profitability with basic earnings per share doubling to CNY 0.0168. The company's debt-to-equity ratio has significantly decreased from 74% to about 36% over five years, suggesting better financial health and more cash than total debt positions it well for future endeavors despite challenges in revenue generation.

- Dive into the specifics of Fujian Start GroupLtd here with our thorough health report.

Gain insights into Fujian Start GroupLtd's past trends and performance with our Past report.

MODEC (TSE:6269)

Simply Wall St Value Rating: ★★★★☆☆

Overview: MODEC, Inc. is a general contractor specializing in the engineering, procurement, construction, and installation of floating production systems globally with a market capitalization of ¥224.39 billion.

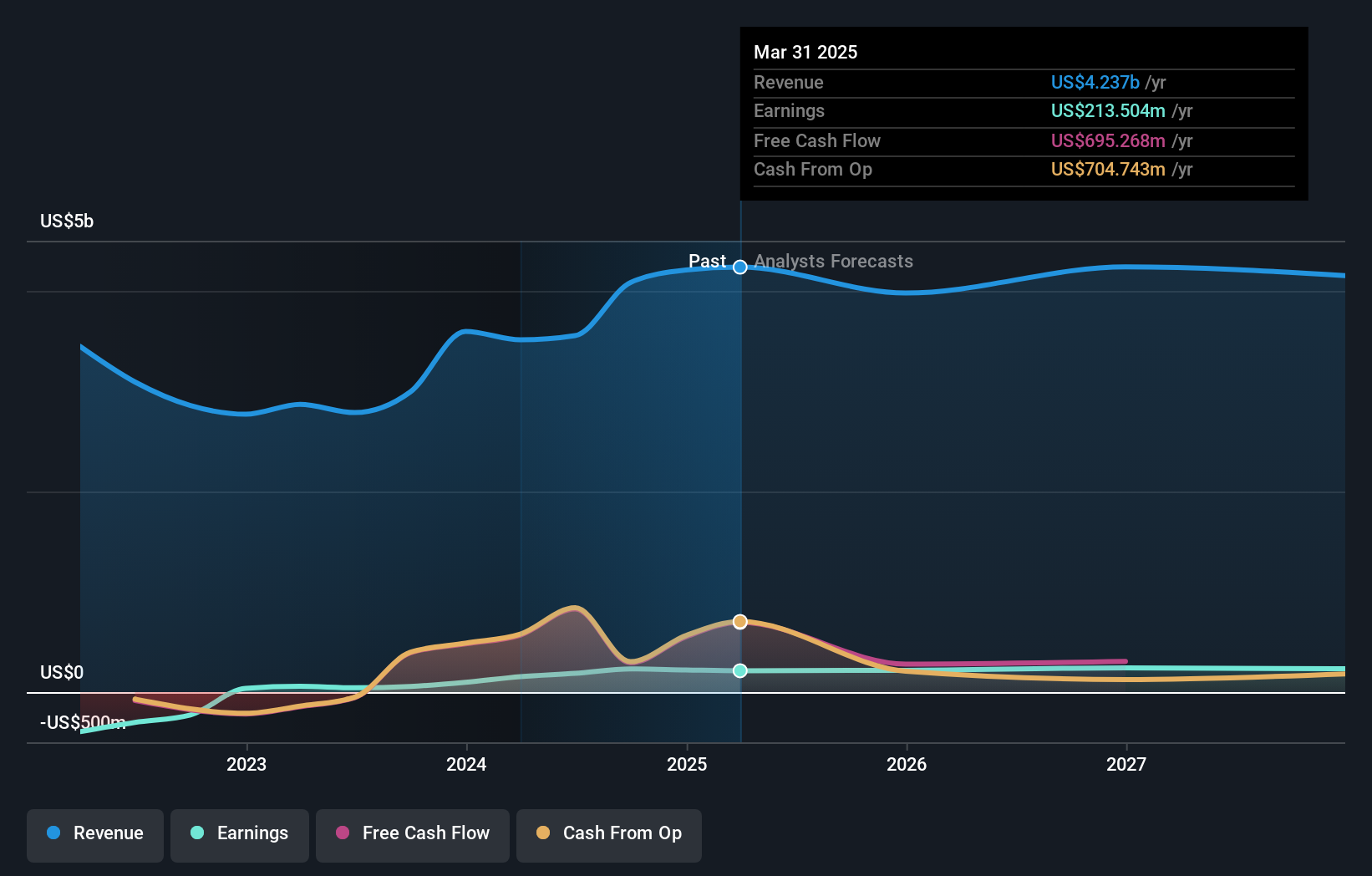

Operations: MODEC generates revenue primarily from the construction of floating oil production facilities and related services, amounting to $4.08 billion.

MODEC is carving its niche in the energy services sector with impressive recent performance. The company's earnings surged by 310% over the past year, outpacing the industry average of 22.5%. Trading at a significant discount, it sits 41.7% below its estimated fair value, suggesting potential undervaluation in the market. Despite an increase in its debt to equity ratio from 18.8% to 46.8% over five years, MODEC remains profitable and covers interest payments comfortably with earnings surpassing interest expenses. This financial stability positions MODEC as a compelling prospect amidst industry volatility and growth challenges ahead.

- Click here and access our complete health analysis report to understand the dynamics of MODEC.

Review our historical performance report to gain insights into MODEC's's past performance.

San-in Godo BankLtd (TSE:8381)

Simply Wall St Value Rating: ★★★★☆☆

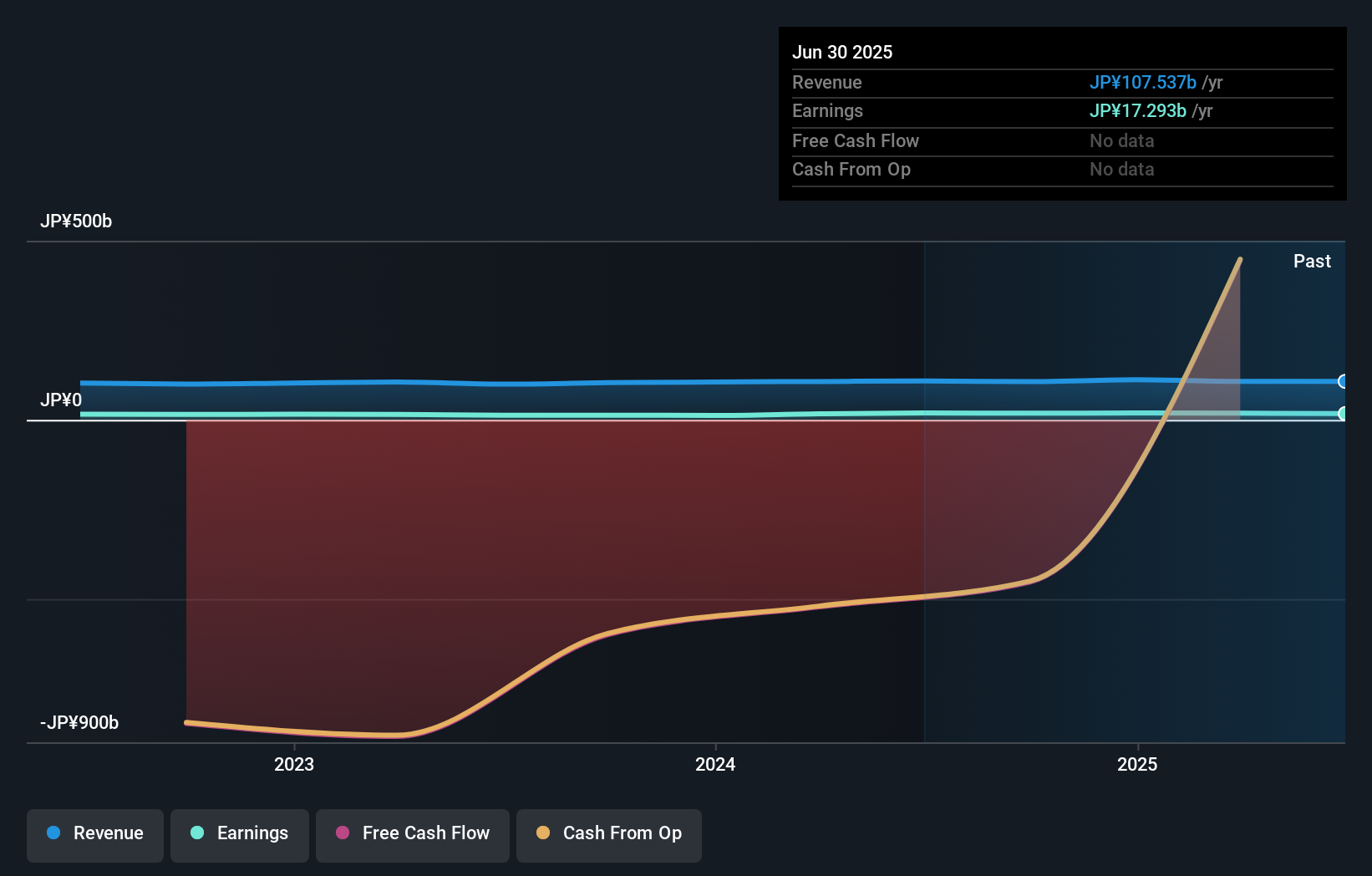

Overview: The San-in Godo Bank, Ltd., along with its subsidiaries, offers a range of banking products and services to individual and corporate clients in Japan, with a market capitalization of ¥187.89 billion.

Operations: San-in Godo Bank generates revenue primarily through interest income from loans and fees from banking services. The bank's cost structure includes interest expenses on deposits and operational costs related to service provision. Notably, the net profit margin is 15.67%, indicating the efficiency of its operations in converting revenue into actual profit.

San-in Godo Bank, with total assets of ¥7.55 trillion and equity of ¥323.5 billion, stands out for its robust earnings growth of 40.4% over the past year, surpassing the industry average of 22.6%. Despite having an appropriate level of bad loans at 1.4%, it faces challenges with a low allowance for these loans at 73%. The bank's valuation appears attractive, trading at nearly 26% below its estimated fair value while relying on primarily low-risk funding sources accounting for 89% of liabilities. Recent guidance suggests ordinary income expectations around ¥131.9 billion consolidated and a dividend increase to ¥24 per share signals confidence in future prospects.

- Take a closer look at San-in Godo BankLtd's potential here in our health report.

Understand San-in Godo BankLtd's track record by examining our Past report.

Turning Ideas Into Actions

- Delve into our full catalog of 4641 Undiscovered Gems With Strong Fundamentals here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:8381

San-in Godo BankLtd

Engages in the provision of various banking products and services for individuals and corporate customers in Japan.

Adequate balance sheet average dividend payer.

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|27.4% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|25.8% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.7% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.0% undervalued

RO

Community Contributor