Advertisement

In a week marked by cautious Federal Reserve commentary and political uncertainty, global markets experienced broad-based declines, with U.S. stocks seeing significant losses before a Friday rally offered some recovery. Amid these turbulent times, investors are increasingly looking towards dividend stocks as they seek stability and income in their portfolios. A good dividend stock typically offers consistent payouts and has the potential to provide a buffer against market volatility, making it an attractive option in uncertain economic conditions.

Top 10 Dividend Stocks

| Name | Dividend Yield | Dividend Rating |

| Guaranty Trust Holding (NGSE:GTCO) | 6.30% | ★★★★★★ |

| Peoples Bancorp (NasdaqGS:PEBO) | 4.98% | ★★★★★★ |

| Southside Bancshares (NYSE:SBSI) | 4.56% | ★★★★★★ |

| Padma Oil (DSE:PADMAOIL) | 7.53% | ★★★★★★ |

| China South Publishing & Media Group (SHSE:601098) | 3.76% | ★★★★★★ |

| HUAYU Automotive Systems (SHSE:600741) | 4.26% | ★★★★★★ |

| E J Holdings (TSE:2153) | 3.84% | ★★★★★★ |

| Citizens & Northern (NasdaqCM:CZNC) | 6.05% | ★★★★★★ |

| Premier Financial (NasdaqGS:PFC) | 4.74% | ★★★★★★ |

| Banque Cantonale Vaudoise (SWX:BCVN) | 5.22% | ★★★★★★ |

Click here to see the full list of 1962 stocks from our Top Dividend Stocks screener.

Underneath we present a selection of stocks filtered out by our screen.

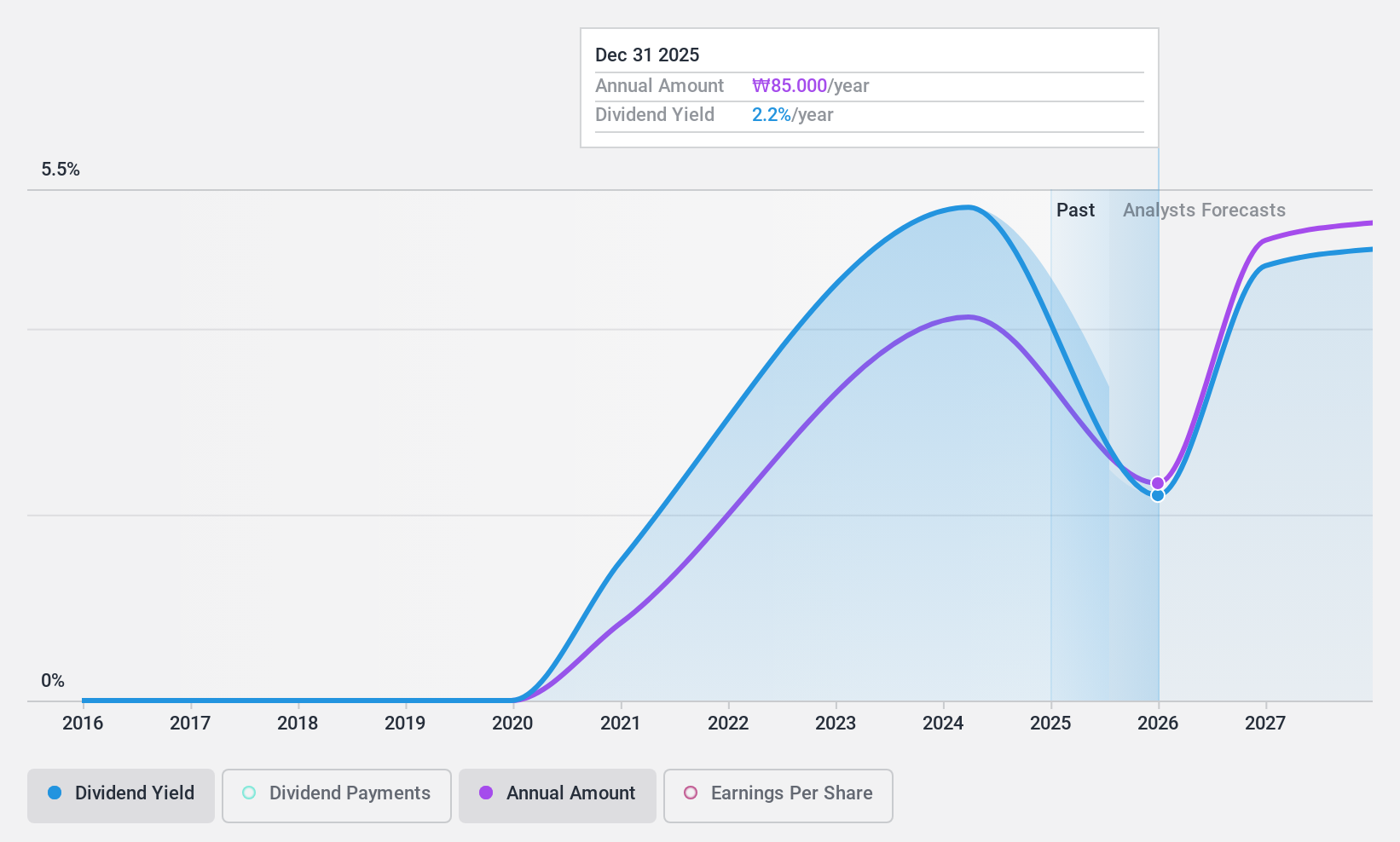

Hanwha Life Insurance (KOSE:A088350)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Hanwha Life Insurance Co., Ltd. offers a range of insurance products to individual and corporate clients across South Korea, Vietnam, China, Indonesia, and other international markets, with a market cap of ₩1.92 trillion.

Operations: Hanwha Life Insurance Co., Ltd.'s revenue is primarily derived from its Insurance segment, amounting to ₩20.36 billion, followed by Certificate at ₩2.03 billion, Non-financial at ₩2.69 billion, and Other Finance at ₩206.63 million.

Dividend Yield: 5.9%

Hanwha Life Insurance offers a compelling dividend profile with its dividends thoroughly covered by both earnings and cash flows, evidenced by a low payout ratio of 20.7% and a cash payout ratio of 2.2%. Despite only five years of dividend history, the payments have been stable and reliable. The company's dividend yield is in the top 25% in the Korean market, enhancing its attractiveness for income-focused investors while trading significantly below estimated fair value.

- Click here to discover the nuances of Hanwha Life Insurance with our detailed analytical dividend report.

- Upon reviewing our latest valuation report, Hanwha Life Insurance's share price might be too pessimistic.

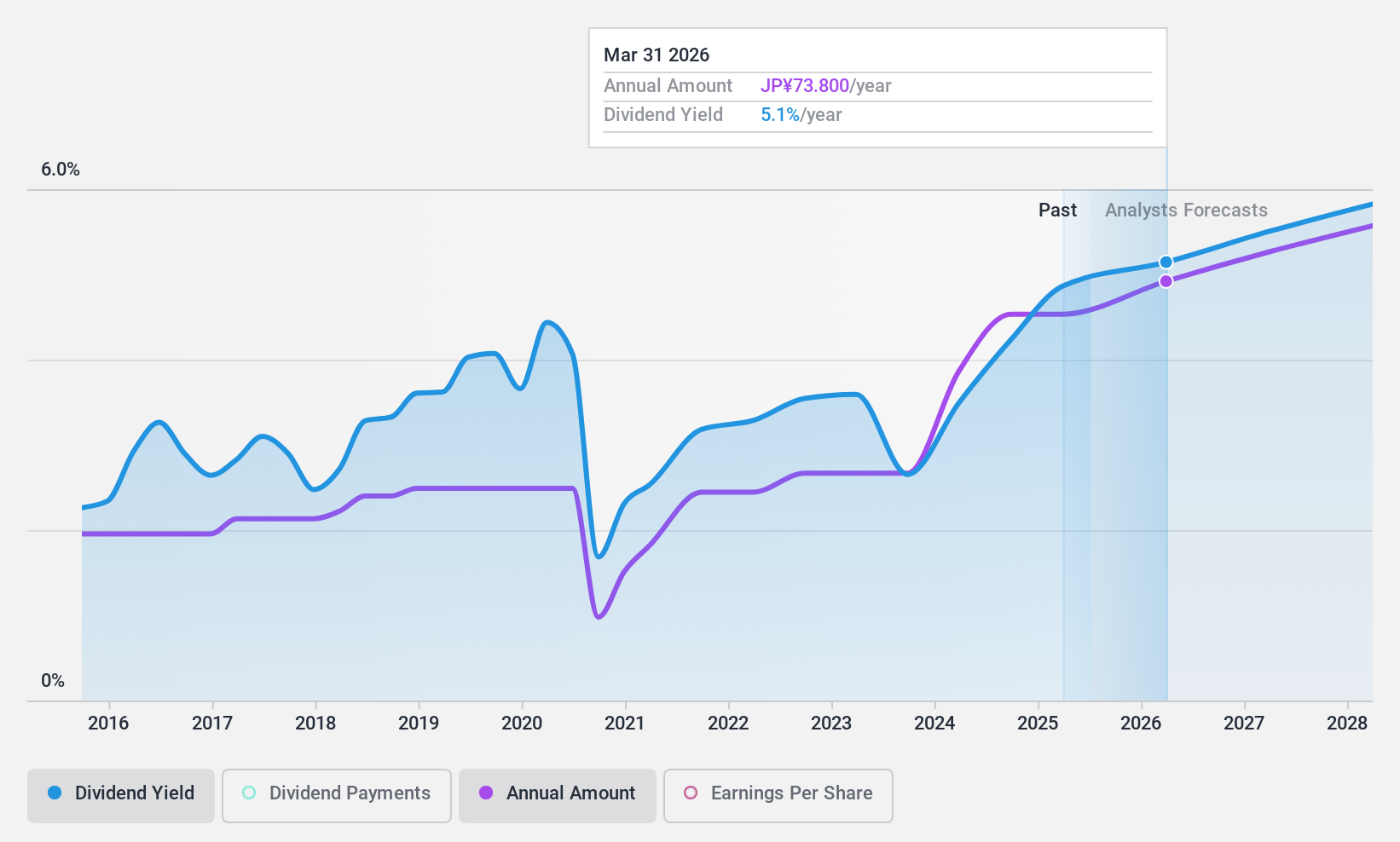

Honda Motor (TSE:7267)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Honda Motor Co., Ltd. is a global manufacturer and distributor of motorcycles, automobiles, power products, and other offerings with operations in Japan, North America, Europe, Asia, and beyond; it has a market cap of approximately ¥5.92 trillion.

Operations: Honda Motor Co., Ltd.'s revenue is primarily derived from its Automobile Business at ¥14.57 billion, followed by the Financial Services Business at ¥3.49 billion, the Motorcycle Business at ¥3.46 billion, and Power Products and Other Businesses contributing ¥411.25 million.

Dividend Yield: 4.7%

Honda Motor's dividend yield ranks in the top 25% of Japanese dividend payers, but it is not well covered by free cash flows. Despite a low payout ratio of 35.7%, indicating coverage by earnings, sustainability concerns arise due to insufficient cash flow support. The company’s dividends have been stable and growing over the past decade. Recent merger talks with Nissan could impact future financial strategies, potentially affecting dividend policies.

- Dive into the specifics of Honda Motor here with our thorough dividend report.

- The valuation report we've compiled suggests that Honda Motor's current price could be quite moderate.

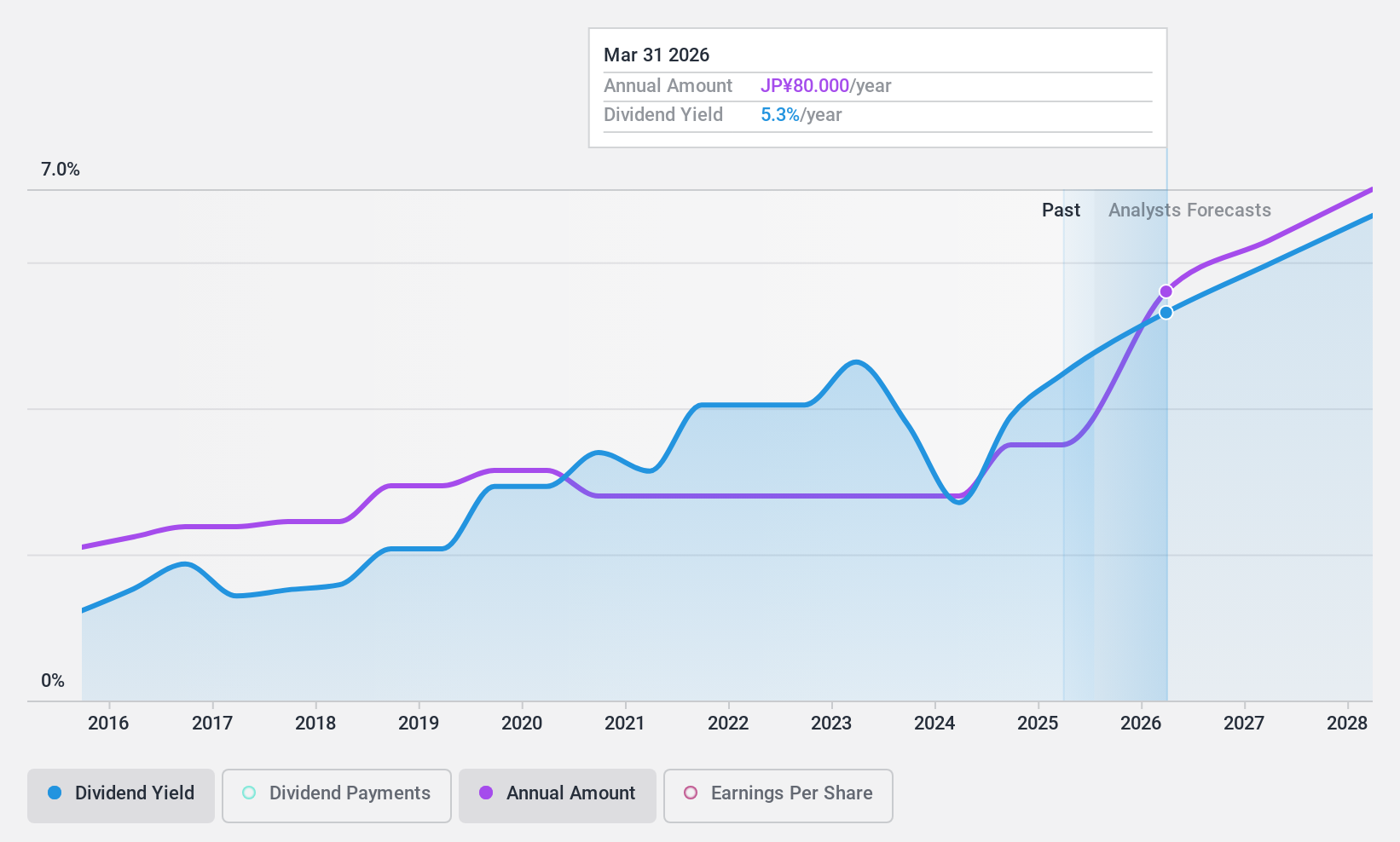

Nippon Seiki (TSE:7287)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Nippon Seiki Co., Ltd. manufactures and sells instruments for automobiles, motorcycles, agricultural and construction machines, and boats across Japan, the Americas, Europe, and Asia with a market cap of ¥64.02 billion.

Operations: Nippon Seiki Co., Ltd.'s revenue segments include Automotive Sales at ¥26.67 billion, the Resin Compound Business at ¥11.07 billion, and the Automotive Parts Business at ¥255.86 billion.

Dividend Yield: 4.5%

Nippon Seiki offers a dividend yield in the top 25% of the Japanese market, but its dividends are not supported by free cash flows despite being covered by earnings with a 68.1% payout ratio. The dividends have been stable and growing over the past decade. Recent share buybacks totaling ¥1,050 million for 1.7% of shares indicate efforts to enhance shareholder returns, though large one-off items affect financial results.

- Click here and access our complete dividend analysis report to understand the dynamics of Nippon Seiki.

- Our valuation report here indicates Nippon Seiki may be overvalued.

Next Steps

- Investigate our full lineup of 1962 Top Dividend Stocks right here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Honda Motor might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:7267

Honda Motor

Develops, manufactures, and distributes motorcycles, automobiles, power, and other products in Japan, North America, Europe, Asia, and internationally.

Undervalued established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|33.3% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|23.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|8.5% overvalued

DA

Community Contributor