- Italy

- /

- Oil and Gas

- /

- BIT:ENI

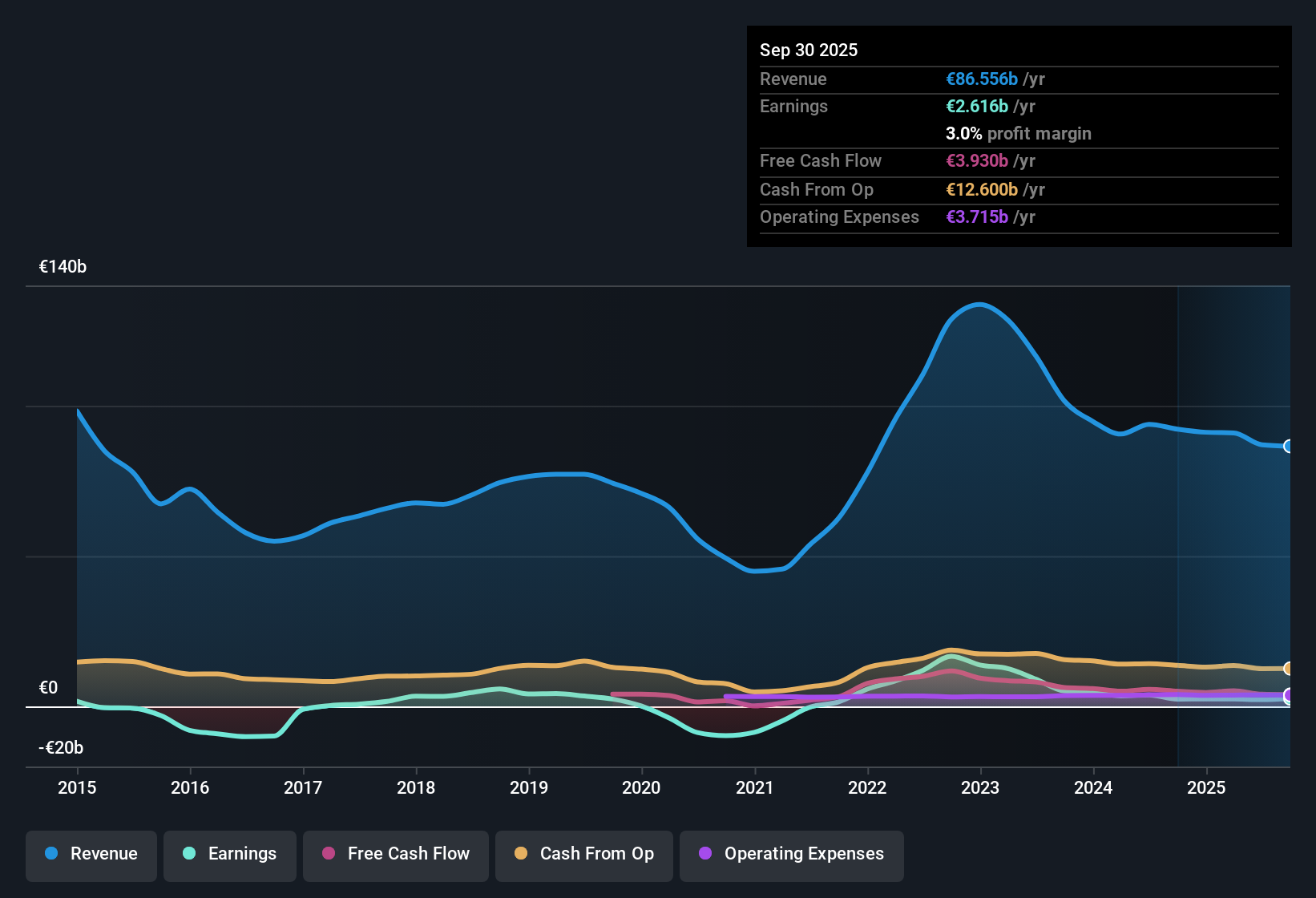

Eni (BIT:ENI) Net Profit Margin Drops to 2.6%, Challenging Bullish Margin Recovery Narratives

Reviewed by Simply Wall St

Eni (BIT:ENI) has grown profitability by 22.2% per year over the past five years, though recent results show a net profit margin of 2.6%, down from last year’s 4.1%. Looking ahead, earnings are forecast to grow at 4% annually and revenues at 3.8% per year, both trailing Italian market averages. With shares trading at €15.84, below a DCF fair value of €19.76 but above industry Price-to-Earnings multiples, investors face a mix of valuation appeal along with concerns about compressed margins and slowing growth.

See our full analysis for Eni.With the headline numbers in hand, the next step is to see how these results compare to the widely debated community narratives and market expectations.

See what the community is saying about Eni

Analyst Margin Forecast Rises to 5.8%

- Analysts expect Eni's profit margins to climb from today's 2.6% to 5.8% in three years, signaling a potential turnaround from recent compression.

- According to the analysts' consensus view, margin gains are tied to diversification into LNG and sustainable mobility, with some important caveats:

- Strategic LNG expansion in Africa, Argentina, and Southeast Asia aims to stabilize earnings as the energy transition unfolds, supporting the case for improved margins.

- Biorefining and growth in sustainable mobility are seen as higher-margin drivers. However, continued legacy business losses and delayed renewable cash flow neutrality could threaten overall margin strength.

Consensus narrative notes Eni’s margin recovery depends on execution in LNG and lower-carbon ventures, while legacy business losses and delayed renewable profits highlight the challenge. See how this debate plays out in the analyst community. 📊 Read the full Eni Consensus Narrative.

Legacy Businesses Continue to Drag Earnings

- Versalis, Eni's chemicals and downstream division, posted ongoing losses last year. Management cited a "lack of meaningful economic recovery" in the European chemical sector and minimal improvement in margin outlook.

- Bears argue the persistent negative free cash flow from legacy businesses poses an ongoing drag on group results:

- The inability to quickly restructure loss-making divisions like Versalis, despite closing high-cost operations, could stall efforts to reduce leverage and limit Eni's ability to boost shareholder returns.

- These challenges threaten to offset gains from faster-growing business areas and increase the risk that Eni will underperform relative to peers during the next industry downturn.

Valuation Signal: Premium Multiple vs Peers

- Eni trades at a Price-to-Earnings ratio of 21.1x, noticeably above its peer group average of 14.7x and the wider European Oil and Gas industry at 14.5x, despite being under its DCF fair value of €19.76.

- Analysts' consensus view states the relatively high PE multiple reflects confidence in margin recovery and growth from new business lines:

- However, the current share price of €15.84 is just 0.5% above the €15.75 analyst price target, suggesting that upside may already be largely reflected unless Eni can exceed margin and earnings expectations decisively.

- The valuation tension highlights how the market is balancing DCF undervaluation against premium multiples, with little margin for error if margin forecasts do not materialize.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Eni on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Spot something in the data that stands out? It takes just a few minutes to craft your perspective and add your voice to the story. Do it your way

A great starting point for your Eni research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

See What Else Is Out There

Eni’s reliance on volatile legacy businesses and recent margin compression highlight ongoing risks to sustained profitability and stable earnings growth.

If choppy results concern you, check out stable growth stocks screener (2099 results) to target companies delivering smoother revenue and profit expansion, regardless of the cycle.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Eni might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About BIT:ENI

Eni

Operates as an integrated energy company in Italy, Other European Union, Rest of Europe, the United States, Asia, Africa, and internationally.

Excellent balance sheet with proven track record and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Cheap if able to sustain revenue, and a potential bargain if able to turn store openings into revenue growth

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)