- India

- /

- Paper and Forestry Products

- /

- NSEI:WSTCSTPAPR

With EPS Growth And More, West Coast Paper Mills (NSE:WSTCSTPAPR) Makes An Interesting Case

The excitement of investing in a company that can reverse its fortunes is a big draw for some speculators, so even companies that have no revenue, no profit, and a record of falling short, can manage to find investors. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses. Loss-making companies are always racing against time to reach financial sustainability, so investors in these companies may be taking on more risk than they should.

So if this idea of high risk and high reward doesn't suit, you might be more interested in profitable, growing companies, like West Coast Paper Mills (NSE:WSTCSTPAPR). While this doesn't necessarily speak to whether it's undervalued, the profitability of the business is enough to warrant some appreciation - especially if its growing.

Check out our latest analysis for West Coast Paper Mills

West Coast Paper Mills' Improving Profits

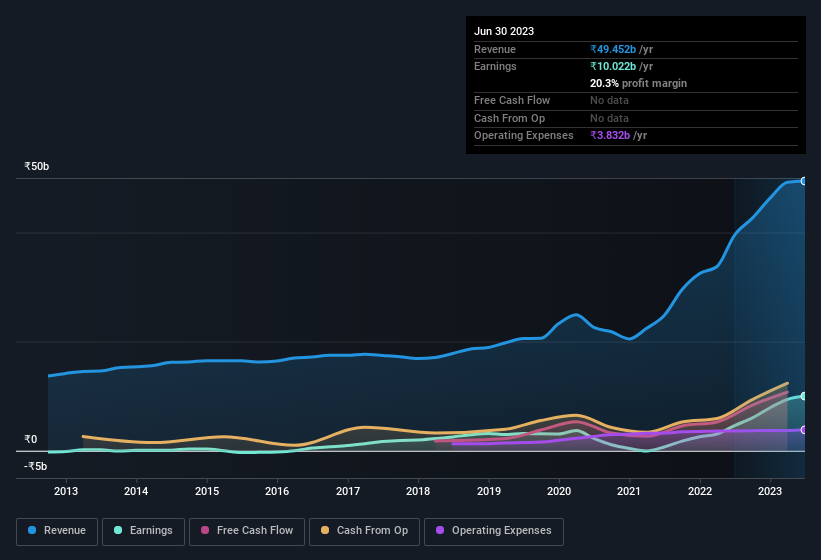

Over the last three years, West Coast Paper Mills has grown earnings per share (EPS) at as impressive rate from a relatively low point, resulting in a three year percentage growth rate that isn't particularly indicative of expected future performance. So it would be better to isolate the growth rate over the last year for our analysis. Outstandingly, West Coast Paper Mills' EPS shot from ₹69.70 to ₹152, over the last year. It's not often a company can achieve year-on-year growth of 118%. That could be a sign that the business has reached a true inflection point.

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. West Coast Paper Mills shareholders can take confidence from the fact that EBIT margins are up from 16% to 31%, and revenue is growing. That's great to see, on both counts.

The chart below shows how the company's bottom and top lines have progressed over time. To see the actual numbers, click on the chart.

While it's always good to see growing profits, you should always remember that a weak balance sheet could come back to bite. So check West Coast Paper Mills' balance sheet strength, before getting too excited.

Are West Coast Paper Mills Insiders Aligned With All Shareholders?

Investors are always searching for a vote of confidence in the companies they hold and insider buying is one of the key indicators for optimism on the market. That's because insider buying often indicates that those closest to the company have confidence that the share price will perform well. Of course, we can never be sure what insiders are thinking, we can only judge their actions.

West Coast Paper Mills top brass are certainly in sync, not having sold any shares, over the last year. But the real excitement comes from the ₹9.6m that Non-Executive Director Shashi Bangur spent buying shares (at an average price of about ₹479). Purchases like this clue us in to the to the faith management has in the business' future.

The good news, alongside the insider buying, for West Coast Paper Mills bulls is that insiders (collectively) have a meaningful investment in the stock. Given insiders own a significant chunk of shares, currently valued at ₹6.1b, they have plenty of motivation to push the business to succeed. Amounting to 15% of the outstanding shares, indicating that insiders are also significantly impacted by the decisions they make on the behalf of the business.

Should You Add West Coast Paper Mills To Your Watchlist?

West Coast Paper Mills' earnings per share growth have been climbing higher at an appreciable rate. The cherry on top is that insiders own a bunch of shares, and one has been buying more. These factors seem to indicate the company's potential and that it has reached an inflection point. We'd suggest West Coast Paper Mills belongs near the top of your watchlist. However, before you get too excited we've discovered 1 warning sign for West Coast Paper Mills that you should be aware of.

The good news is that West Coast Paper Mills is not the only growth stock with insider buying. Here's a list of them... with insider buying in the last three months!

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Valuation is complex, but we're here to simplify it.

Discover if West Coast Paper Mills might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:WSTCSTPAPR

West Coast Paper Mills

Manufactures, produces and sells pulp, paper, and paper boards in India.

Flawless balance sheet average dividend payer.

Market Insights

Community Narratives