- India

- /

- Personal Products

- /

- NSEI:COLPAL

Colgate-Palmolive (India)'s (NSE:COLPAL) Solid Profits Have Weak Fundamentals

Despite announcing strong earnings, Colgate-Palmolive (India) Limited's (NSE:COLPAL) stock was sluggish. We think that the market might be paying attention to some underlying factors that they find to be concerning.

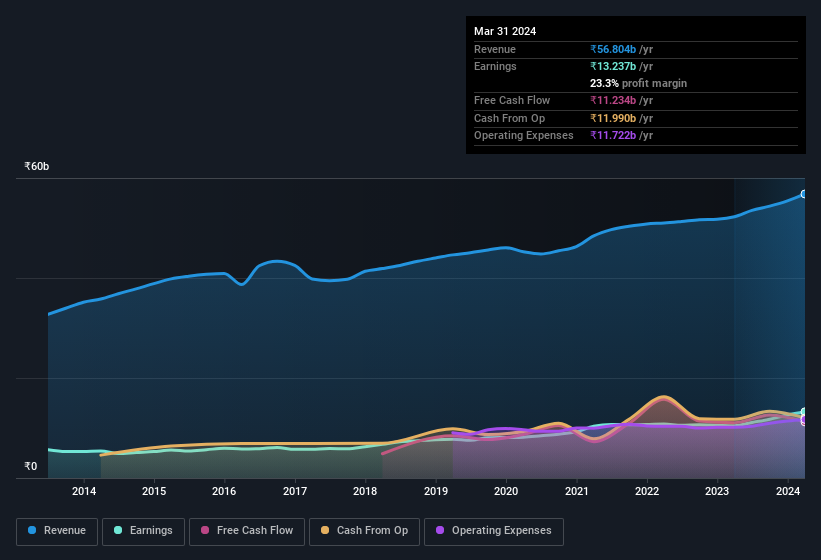

See our latest analysis for Colgate-Palmolive (India)

A Closer Look At Colgate-Palmolive (India)'s Earnings

Many investors haven't heard of the accrual ratio from cashflow, but it is actually a useful measure of how well a company's profit is backed up by free cash flow (FCF) during a given period. To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. This ratio tells us how much of a company's profit is not backed by free cashflow.

As a result, a negative accrual ratio is a positive for the company, and a positive accrual ratio is a negative. That is not intended to imply we should worry about a positive accrual ratio, but it's worth noting where the accrual ratio is rather high. That's because some academic studies have suggested that high accruals ratios tend to lead to lower profit or less profit growth.

For the year to March 2024, Colgate-Palmolive (India) had an accrual ratio of 0.28. Unfortunately, that means its free cash flow was a lot less than its statutory profit, which makes us doubt the utility of profit as a guide. Indeed, in the last twelve months it reported free cash flow of ₹11b, which is significantly less than its profit of ₹13.2b. Notably Colgate-Palmolive (India)'s free cash flow was stable over the last year. The good news for shareholders is that Colgate-Palmolive (India)'s accrual ratio was much better last year, so this year's poor reading might simply be a case of a short term mismatch between profit and FCF. As a result, some shareholders may be looking for stronger cash conversion in the current year.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

Our Take On Colgate-Palmolive (India)'s Profit Performance

Colgate-Palmolive (India)'s accrual ratio for the last twelve months signifies cash conversion is less than ideal, which is a negative when it comes to our view of its earnings. Therefore, it seems possible to us that Colgate-Palmolive (India)'s true underlying earnings power is actually less than its statutory profit. But at least holders can take some solace from the 28% per annum growth in EPS for the last three. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. Keep in mind, when it comes to analysing a stock it's worth noting the risks involved. For example - Colgate-Palmolive (India) has 2 warning signs we think you should be aware of.

This note has only looked at a single factor that sheds light on the nature of Colgate-Palmolive (India)'s profit. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

If you're looking to trade Colgate-Palmolive (India), open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:COLPAL

Colgate-Palmolive (India)

Manufactures and trades in personal and oral care products in India.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Community Narratives