Advertisement

Tasty Bite Eatables (NSE:TASTYBITE) shareholders notch a 4.6% CAGR over 5 years, yet earnings have been shrinking

Tasty Bite Eatables Limited (NSE:TASTYBITE) shareholders might be concerned after seeing the share price drop 13% in the last quarter. But at least the stock is up over the last five years. However we are not very impressed because the share price is only up 25%, less than the market return of 149%. While the long term returns are impressive, we do have some sympathy for those who bought more recently, given the 22% drop, in the last year.

The past week has proven to be lucrative for Tasty Bite Eatables investors, so let's see if fundamentals drove the company's five-year performance.

Check out our latest analysis for Tasty Bite Eatables

There is no denying that markets are sometimes efficient, but prices do not always reflect underlying business performance. One imperfect but simple way to consider how the market perception of a company has shifted is to compare the change in the earnings per share (EPS) with the share price movement.

During five years of share price growth, Tasty Bite Eatables actually saw its EPS drop 15% per year.

The strong decline in earnings per share suggests the market isn't using EPS to judge the company. The falling EPS doesn't correlate with the climbing share price, so it's worth taking a look at other metrics.

The modest 0.02% dividend yield is unlikely to be propping up the share price. On the other hand, Tasty Bite Eatables' revenue is growing nicely, at a compound rate of 6.2% over the last five years. It's quite possible that management are prioritizing revenue growth over EPS growth at the moment.

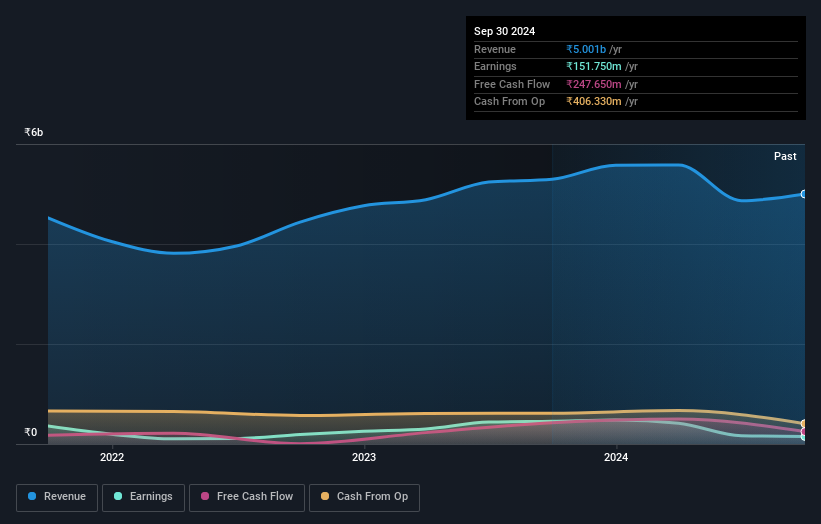

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

This free interactive report on Tasty Bite Eatables' balance sheet strength is a great place to start, if you want to investigate the stock further.

A Different Perspective

Investors in Tasty Bite Eatables had a tough year, with a total loss of 22% (including dividends), against a market gain of about 12%. Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. On the bright side, long term shareholders have made money, with a gain of 5% per year over half a decade. If the fundamental data continues to indicate long term sustainable growth, the current sell-off could be an opportunity worth considering. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. To that end, you should learn about the 2 warning signs we've spotted with Tasty Bite Eatables (including 1 which is a bit unpleasant) .

For those who like to find winning investments this free list of undervalued companies with recent insider purchasing, could be just the ticket.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Indian exchanges.

Valuation is complex, but we're here to simplify it.

Discover if Tasty Bite Eatables might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:TASTYBITE

Tasty Bite Eatables

Manufactures and sells prepared foods in India and internationally.

Excellent balance sheet very low.

Similar Companies

Market Insights

Advertisement

Community Narratives

RIO is poised to weather a depressed iron ore environment, but commodity diversification comes with lower margins

Fair Value AU$110.51|4.0% overvalued

DU

Community Contributor

The demand for personalized medicine will keep Thermo Fisher Scientific thriving

Fair Value US$540.27|20.1% undervalued

UN

Community Contributor

Silver Play by A Family with 10x Potential

Fair Value UK£24.00|88.5% undervalued

RO

Community Contributor