Regular readers will know that we love our dividends at Simply Wall St, which is why it's exciting to see ITC Limited (NSE:ITC) is about to trade ex-dividend in the next 4 days. The ex-dividend date is one business day before the record date, which is the cut-off date for shareholders to be present on the company's books to be eligible for a dividend payment. The ex-dividend date is important because any transaction on a stock needs to have been settled before the record date in order to be eligible for a dividend. This means that investors who purchase ITC's shares on or after the 4th of June will not receive the dividend, which will be paid on the 25th of August.

The company's next dividend payment will be ₹7.50 per share. Last year, in total, the company distributed ₹13.00 to shareholders. Based on the last year's worth of payments, ITC stock has a trailing yield of around 3.2% on the current share price of ₹430.95. If you buy this business for its dividend, you should have an idea of whether ITC's dividend is reliable and sustainable. So we need to check whether the dividend payments are covered, and if earnings are growing.

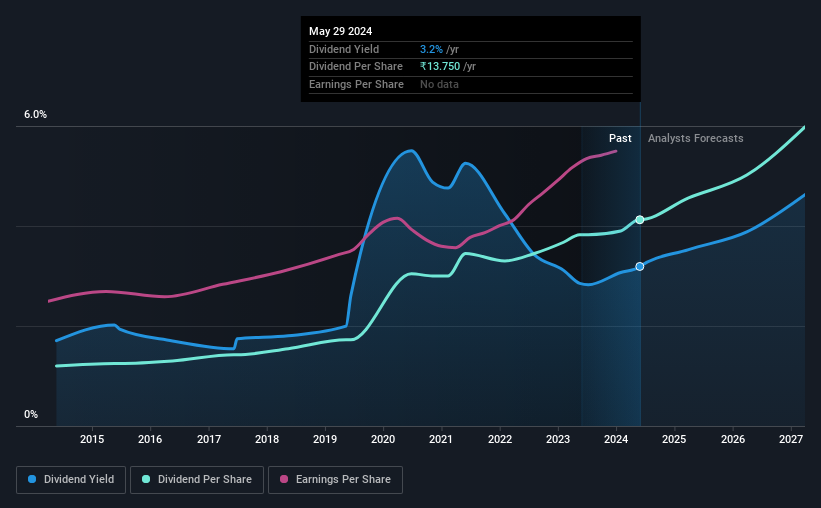

See our latest analysis for ITC

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Its dividend payout ratio is 79% of profit, which means the company is paying out a majority of its earnings. The relatively limited profit reinvestment could slow the rate of future earnings growth. It could become a concern if earnings started to decline. Yet cash flows are even more important than profits for assessing a dividend, so we need to see if the company generated enough cash to pay its distribution. It paid out 97% of its free cash flow in the form of dividends last year, which is outside the comfort zone for most businesses. Cash flows are usually much more volatile than earnings, so this could be a temporary effect - but we'd generally want to look more closely here.

ITC paid out less in dividends than it reported in profits, but unfortunately it didn't generate enough cash to cover the dividend. Cash is king, as they say, and were ITC to repeatedly pay dividends that aren't well covered by cashflow, we would consider this a warning sign.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Stocks in companies that generate sustainable earnings growth often make the best dividend prospects, as it is easier to lift the dividend when earnings are rising. Investors love dividends, so if earnings fall and the dividend is reduced, expect a stock to be sold off heavily at the same time. For this reason, we're glad to see ITC's earnings per share have risen 12% per annum over the last five years. Earnings have been growing at a decent rate, but we're concerned dividend payments consumed most of the company's cash flow over the past year.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. ITC has delivered an average of 13% per year annual increase in its dividend, based on the past 10 years of dividend payments. It's great to see earnings per share growing rapidly over several years, and dividends per share growing right along with it.

The Bottom Line

Is ITC worth buying for its dividend? Earnings per share growth is a positive, and the company's payout ratio looks normal. However, we note ITC paid out a much higher percentage of its free cash flow, which makes us uncomfortable. Overall, it's not a bad combination, but we feel that there are likely more attractive dividend prospects out there.

However if you're still interested in ITC as a potential investment, you should definitely consider some of the risks involved with ITC. Our analysis shows 1 warning sign for ITC and you should be aware of it before buying any shares.

If you're in the market for strong dividend payers, we recommend checking our selection of top dividend stocks.

If you're looking to trade ITC, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:ITC

ITC

Engages in the fast-moving consumer goods, hotels, paperboards and paper and packaging, agri, and information technology businesses in India and internationally.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Community Narratives