- India

- /

- Diversified Financial

- /

- NSEI:CANFINHOME

Can Fin Homes Limited (NSE:CANFINHOME) Shares Fly 27% But Investors Aren't Buying For Growth

Can Fin Homes Limited (NSE:CANFINHOME) shareholders have had their patience rewarded with a 27% share price jump in the last month. Looking further back, the 18% rise over the last twelve months isn't too bad notwithstanding the strength over the last 30 days.

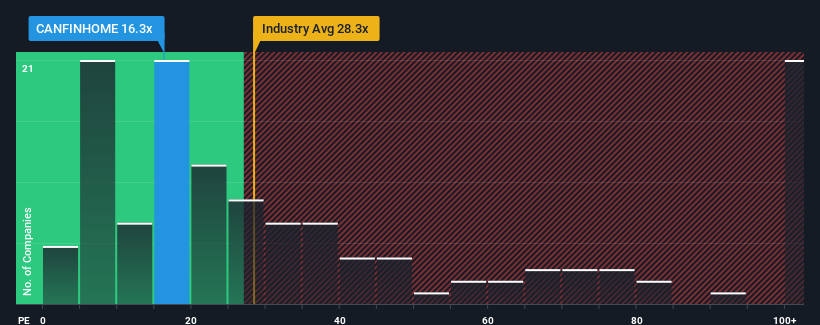

Although its price has surged higher, Can Fin Homes' price-to-earnings (or "P/E") ratio of 16.3x might still make it look like a strong buy right now compared to the market in India, where around half of the companies have P/E ratios above 33x and even P/E's above 64x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/E.

There hasn't been much to differentiate Can Fin Homes' and the market's earnings growth lately. One possibility is that the P/E is low because investors think this modest earnings performance may begin to slide. If you like the company, you'd be hoping this isn't the case so that you could pick up some stock while it's out of favour.

See our latest analysis for Can Fin Homes

Does Growth Match The Low P/E?

There's an inherent assumption that a company should far underperform the market for P/E ratios like Can Fin Homes' to be considered reasonable.

If we review the last year of earnings growth, the company posted a terrific increase of 21%. Pleasingly, EPS has also lifted 65% in aggregate from three years ago, thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing earnings over that time.

Shifting to the future, estimates from the analysts covering the company suggest earnings should grow by 16% per year over the next three years. That's shaping up to be materially lower than the 22% per annum growth forecast for the broader market.

With this information, we can see why Can Fin Homes is trading at a P/E lower than the market. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Key Takeaway

Even after such a strong price move, Can Fin Homes' P/E still trails the rest of the market significantly. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Can Fin Homes maintains its low P/E on the weakness of its forecast growth being lower than the wider market, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with Can Fin Homes (at least 1 which makes us a bit uncomfortable), and understanding these should be part of your investment process.

If you're unsure about the strength of Can Fin Homes' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:CANFINHOME

Can Fin Homes

Provides housing finance services primarily to individuals, builders, corporates, and others in India.

6 star dividend payer and fair value.

Similar Companies

Market Insights

Community Narratives