With EPS Growth And More, United Polyfab Gujarat (NSE:UNITEDPOLY) Makes An Interesting Case

The excitement of investing in a company that can reverse its fortunes is a big draw for some speculators, so even companies that have no revenue, no profit, and a record of falling short, can manage to find investors. Sometimes these stories can cloud the minds of investors, leading them to invest with their emotions rather than on the merit of good company fundamentals. Loss-making companies are always racing against time to reach financial sustainability, so investors in these companies may be taking on more risk than they should.

In contrast to all that, many investors prefer to focus on companies like United Polyfab Gujarat (NSE:UNITEDPOLY), which has not only revenues, but also profits. While profit isn't the sole metric that should be considered when investing, it's worth recognising businesses that can consistently produce it.

Our analysis indicates that UNITEDPOLY is potentially undervalued!

United Polyfab Gujarat's Improving Profits

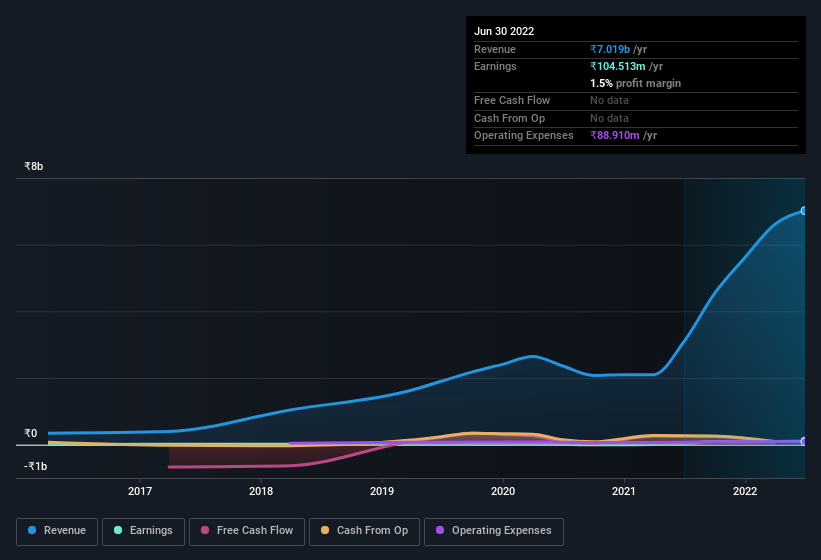

In business, profits are a key measure of success; and share prices tend to reflect earnings per share (EPS) performance. So for many budding investors, improving EPS is considered a good sign. Commendations have to be given in seeing that United Polyfab Gujarat grew its EPS from ₹1.56 to ₹4.99, in one short year. Even though that growth rate may not be repeated, that looks like a breakout improvement. But the key is discerning whether something profound has changed, or if this is a just a one-off boost.

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. While we note United Polyfab Gujarat achieved similar EBIT margins to last year, revenue grew by a solid 127% to ₹7.0b. That's progress.

In the chart below, you can see how the company has grown earnings and revenue, over time. To see the actual numbers, click on the chart.

Since United Polyfab Gujarat is no giant, with a market capitalisation of ₹1.0b, you should definitely check its cash and debt before getting too excited about its prospects.

Are United Polyfab Gujarat Insiders Aligned With All Shareholders?

Investors are always searching for a vote of confidence in the companies they hold and insider buying is one of the key indicators for optimism on the market. That's because insider buying often indicates that those closest to the company have confidence that the share price will perform well. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

Insider selling of United Polyfab Gujarat shares was insignificant compared to the one buyer, over the last twelve months. To be exact, Chairman of the Board & MD Gagan Nirmal Mittal put their money where their mouth is, paying ₹50m at an average of price of ₹47.81 per share That can definitely be seen as a sign of conviction.

On top of the insider buying, we can also see that United Polyfab Gujarat insiders own a large chunk of the company. Owning 43% of the company, insiders have plenty riding on the performance of the the share price. Shareholders and speculators should be reassured by this kind of alignment, as it suggests the business will be run for the benefit of shareholders. Valued at only ₹1.0b United Polyfab Gujarat is really small for a listed company. That means insiders only have ₹446m worth of shares, despite the large proportional holding. This isn't an overly large holding but it should still keep the insiders motivated to deliver the best outcomes for shareholders.

While insiders are apparently happy to hold and accumulate shares, that is just part of the big picture. That's because on our analysis the CEO, Gagan Nirmal Mittal, is paid less than the median for similar sized companies. The median total compensation for CEOs of companies similar in size to United Polyfab Gujarat, with market caps under ₹16b is around ₹3.6m.

United Polyfab Gujarat's CEO only received compensation totalling ₹1.4m in the year to March 2022. You could consider this pay as somewhat symbolic, which suggests the CEO does not need a lot of compensation to stay motivated. CEO compensation is hardly the most important aspect of a company to consider, but when it's reasonable, that gives a little more confidence that leadership are looking out for shareholder interests. Generally, arguments can be made that reasonable pay levels attest to good decision-making.

Is United Polyfab Gujarat Worth Keeping An Eye On?

United Polyfab Gujarat's earnings have taken off in quite an impressive fashion. The cherry on top is that insiders own a bunch of shares, and one has been buying more. These factors seem to indicate the company's potential and that it has reached an inflection point. We'd suggest United Polyfab Gujarat belongs near the top of your watchlist. We don't want to rain on the parade too much, but we did also find 2 warning signs for United Polyfab Gujarat (1 is potentially serious!) that you need to be mindful of.

The good news is that United Polyfab Gujarat is not the only growth stock with insider buying. Here's a list of them... with insider buying in the last three months!

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

If you're looking to trade United Polyfab Gujarat, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:UNITEDPOLY

Solid track record with adequate balance sheet.

Similar Companies

Market Insights

Community Narratives