This Broker Just Slashed Their GMM Pfaudler Limited (NSE:GMMPFAUDLR) Earnings Forecasts

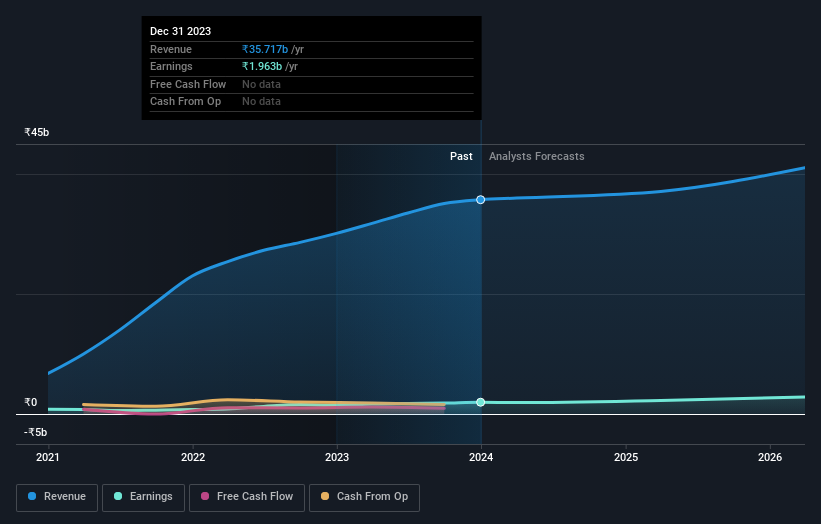

One thing we could say about the covering analyst on GMM Pfaudler Limited (NSE:GMMPFAUDLR) - they aren't optimistic, having just made a major negative revision to their near-term (statutory) forecasts for the organization. Revenue and earnings per share (EPS) forecasts were both revised downwards, with the analyst seeing grey clouds on the horizon.

Following the downgrade, the most recent consensus for GMM Pfaudler from its solo analyst is for revenues of ₹37b in 2025 which, if met, would be a credible 3.8% increase on its sales over the past 12 months. Statutory earnings per share are presumed to ascend 15% to ₹50.30. Previously, the analyst had been modelling revenues of ₹41b and earnings per share (EPS) of ₹64.10 in 2025. It looks like analyst sentiment has declined substantially, with a measurable cut to revenue estimates and a pretty serious decline to earnings per share numbers as well.

See our latest analysis for GMM Pfaudler

The consensus price target fell 13% to ₹1,803, with the weaker earnings outlook clearly leading analyst valuation estimates.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the GMM Pfaudler's past performance and to peers in the same industry. We would highlight that GMM Pfaudler's revenue growth is expected to slow, with the forecast 3.1% annualised growth rate until the end of 2025 being well below the historical 43% p.a. growth over the last five years. Compare this against other companies (with analyst forecasts) in the industry, which are in aggregate expected to see revenue growth of 12% annually. Factoring in the forecast slowdown in growth, it seems obvious that GMM Pfaudler is also expected to grow slower than other industry participants.

The Bottom Line

The most important thing to take away is that the analyst cut their earnings per share estimates, expecting a clear decline in business conditions. Unfortunately the analyst also downgraded their revenue estimates, and industry data suggests that GMM Pfaudler's revenues are expected to grow slower than the wider market. With a serious cut to next year's expectations and a falling price target, we wouldn't be surprised if investors were becoming wary of GMM Pfaudler.

Even so, the longer term trajectory of the business is much more important for the value creation of shareholders. We have analyst estimates for GMM Pfaudler going out as far as 2026, and you can see them free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:GMMPFAUDLR

GMM Pfaudler

Designs, manufactures, installs, and services corrosion-resistant equipment and complete chemical process systems used in the chemical, pharmaceutical, and other industries in India and internationally.

Adequate balance sheet average dividend payer.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)