- India

- /

- Auto Components

- /

- NSEI:ASKAUTOLTD

ASK Automotive Limited (NSE:ASKAUTOLTD) Just Reported And Analysts Have Been Lifting Their Price Targets

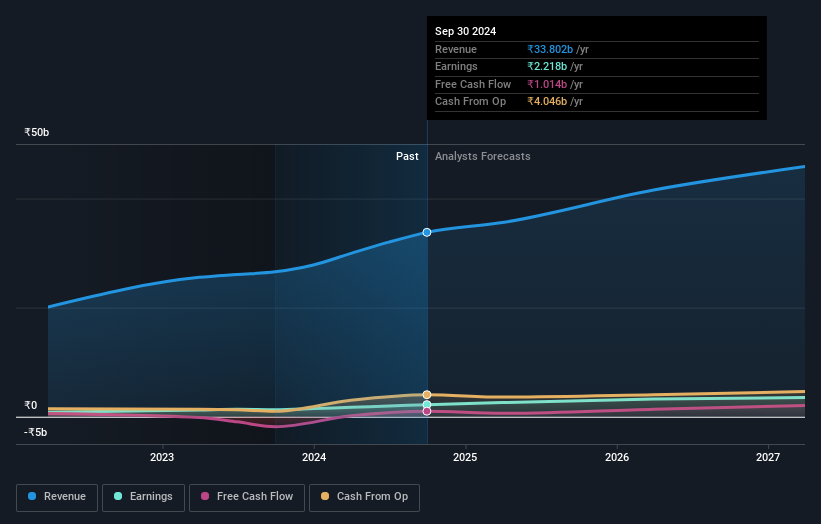

It's been a good week for ASK Automotive Limited (NSE:ASKAUTOLTD) shareholders, because the company has just released its latest second-quarter results, and the shares gained 8.7% to ₹442. Results overall were respectable, with statutory earnings of ₹8.81 per share roughly in line with what the analysts had forecast. Revenues of ₹9.7b came in 3.7% ahead of analyst predictions. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

Check out our latest analysis for ASK Automotive

Taking into account the latest results, the most recent consensus for ASK Automotive from three analysts is for revenues of ₹35.6b in 2025. If met, it would imply a modest 5.3% increase on its revenue over the past 12 months. Per-share earnings are expected to step up 17% to ₹13.20. Yet prior to the latest earnings, the analysts had been anticipated revenues of ₹35.2b and earnings per share (EPS) of ₹12.00 in 2025. The analysts seems to have become more bullish on the business, judging by their new earnings per share estimates.

The analysts have been lifting their price targets on the back of the earnings upgrade, with the consensus price target rising 20% to ₹473. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. There are some variant perceptions on ASK Automotive, with the most bullish analyst valuing it at ₹475 and the most bearish at ₹470 per share. This is a very narrow spread of estimates, implying either that ASK Automotive is an easy company to value, or - more likely - the analysts are relying heavily on some key assumptions.

Of course, another way to look at these forecasts is to place them into context against the industry itself. We would highlight that ASK Automotive's revenue growth is expected to slow, with the forecast 11% annualised growth rate until the end of 2025 being well below the historical 27% growth over the last year. Juxtapose this against the other companies in the industry with analyst coverage, which are forecast to grow their revenues (in aggregate) 10% annually. Factoring in the forecast slowdown in growth, it looks like ASK Automotive is forecast to grow at about the same rate as the wider industry.

The Bottom Line

The most important thing here is that the analysts upgraded their earnings per share estimates, suggesting that there has been a clear increase in optimism towards ASK Automotive following these results. They also reconfirmed their revenue estimates, with the company predicted to grow at about the same rate as the wider industry. There was also a nice increase in the price target, with the analysts clearly feeling that the intrinsic value of the business is improving.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. We have estimates - from multiple ASK Automotive analysts - going out to 2027, and you can see them free on our platform here.

Even so, be aware that ASK Automotive is showing 1 warning sign in our investment analysis , you should know about...

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:ASKAUTOLTD

ASK Automotive

Manufactures and sells auto components for the automobile industry in India.

Reasonable growth potential with proven track record.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Unicycive Therapeutics (Nasdaq: UNCY) – Preparing for a Second Shot at Bringing a New Kidney Treatment to Market (TEST)

Rocket Lab USA Will Ignite a 30% Revenue Growth Journey

Dollar general to grow

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026