- Israel

- /

- Wireless Telecom

- /

- TASE:CEL

Cellcom Israel (TASE:CEL) Reports 16% Net Income Increase in Q2 2025

Reviewed by Simply Wall St

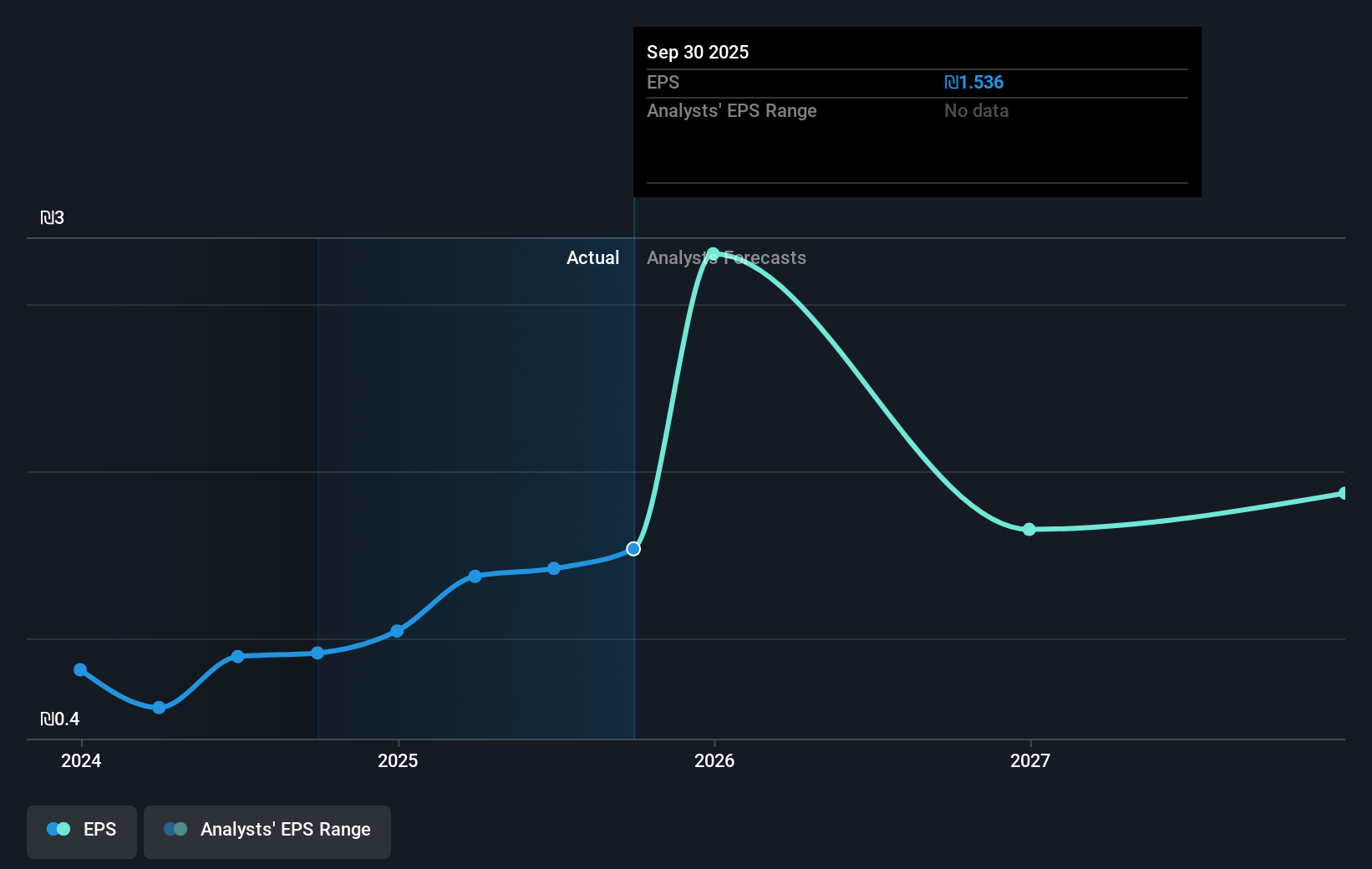

Cellcom Israel (TASE:CEL) recently reported its Q2 2025 earnings, revealing a 16% increase in net income compared to last year, while sales saw a slight decline. This upward trend in profitability may have supported the company’s stock price movement of 38% over the last quarter, though the broader market trends remain largely positive. With the S&P 500 and Nasdaq hitting all-time highs in the same period, the market environment itself has been conducive to rising valuations. The growth in earnings per share further added momentum to Cellcom Israel's share price amidst a favorable market landscape.

We've identified 1 warning sign for Cellcom Israel that you should be aware of.

Over the past five years, Cellcom Israel's total shareholder return, which includes both share price appreciation and dividends, reached 169.86%. This impressive growth reflects strong company performance relative to the industry. Notably, in the most recent year, Cellcom's performance outpaced both the Israeli market and the Wireless Telecom industry, with a significantly higher return over the 12-month period compared to the general market return of 62.9% and industry return of 23.1%.

The recent earnings announcement highlighted a positive trend in net income growth, with both quarterly and half-yearly positive results. This trend, along with a notably higher earnings per share, indicates a robust upward trajectory that may influence future revenue and earnings forecasts positively. However, despite this strong performance, Cellcom's current share price of ₪33.84 remains slightly above the consensus analyst price target of ₪33.00. Consequently, while the stock has experienced significant appreciation, potential investors might view it as being slightly overvalued based on current analyst expectations. The existing price premium above the estimated value could prompt closer scrutiny regarding anticipated future growth prospects.

Our expertly prepared valuation report Cellcom Israel implies its share price may be too high.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TASE:CEL

Solid track record with mediocre balance sheet.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)