Advertisement

- Poland

- /

- Metals and Mining

- /

- WSE:COG

3 Stocks That May Be Priced Below Their Worth In February 2025

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate geopolitical tensions and consumer spending concerns, major indices have experienced notable fluctuations, with recent declines highlighting investor apprehension. Amid this uncertainty, identifying stocks that may be undervalued can present opportunities for investors seeking to capitalize on potential market inefficiencies.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Argan (NYSE:AGX) | US$133.63 | US$264.41 | 49.5% |

| Hibino (TSE:2469) | ¥2795.00 | ¥5545.38 | 49.6% |

| Celestica (TSX:CLS) | CA$169.73 | CA$335.20 | 49.4% |

| 3onedata (SHSE:688618) | CN¥24.76 | CN¥49.00 | 49.5% |

| Neosem (KOSDAQ:A253590) | ₩12020.00 | ₩23933.78 | 49.8% |

| Shanghai Haohai Biological Technology (SEHK:6826) | HK$26.70 | HK$52.81 | 49.4% |

| Sobha (NSEI:SOBHA) | ₹1191.35 | ₹2382.65 | 50% |

| Laboratorio Reig Jofre (BME:RJF) | €2.69 | €5.32 | 49.4% |

| Integral Diagnostics (ASX:IDX) | A$2.89 | A$5.77 | 49.9% |

| Superloop (ASX:SLC) | A$2.19 | A$4.35 | 49.6% |

Here we highlight a subset of our preferred stocks from the screener.

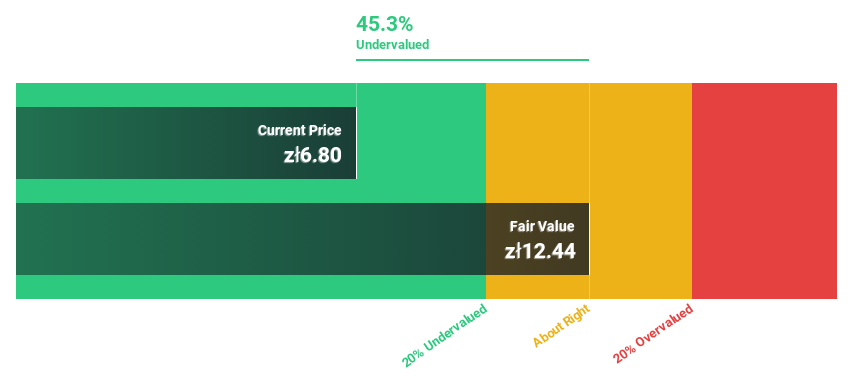

Bang & Olufsen (CPSE:BO)

Overview: Bang & Olufsen A/S is a company that designs, develops, markets, manufactures, and sells audio and video products across Europe, the Middle East, Africa, the Americas, and the Asia Pacific with a market cap of DKK2.12 billion.

Operations: The company's revenue segments are distributed across APAC with DKK690 million, EMEA with DKK1.21 billion, Americas with DKK302 million, and Brand Partnering and Other Activities contributing DKK312 million.

Estimated Discount To Fair Value: 45.3%

Bang & Olufsen is trading at DKK 14.54, significantly below its estimated fair value of DKK 26.6, suggesting it may be undervalued based on cash flows. Despite recent financial challenges, including a net loss of DKK 30 million for the past six months and shareholder dilution from a follow-on equity offering, the company is expected to achieve profitability within three years with revenue growth outpacing the Danish market at 9.8% annually.

- In light of our recent growth report, it seems possible that Bang & Olufsen's financial performance will exceed current levels.

- Get an in-depth perspective on Bang & Olufsen's balance sheet by reading our health report here.

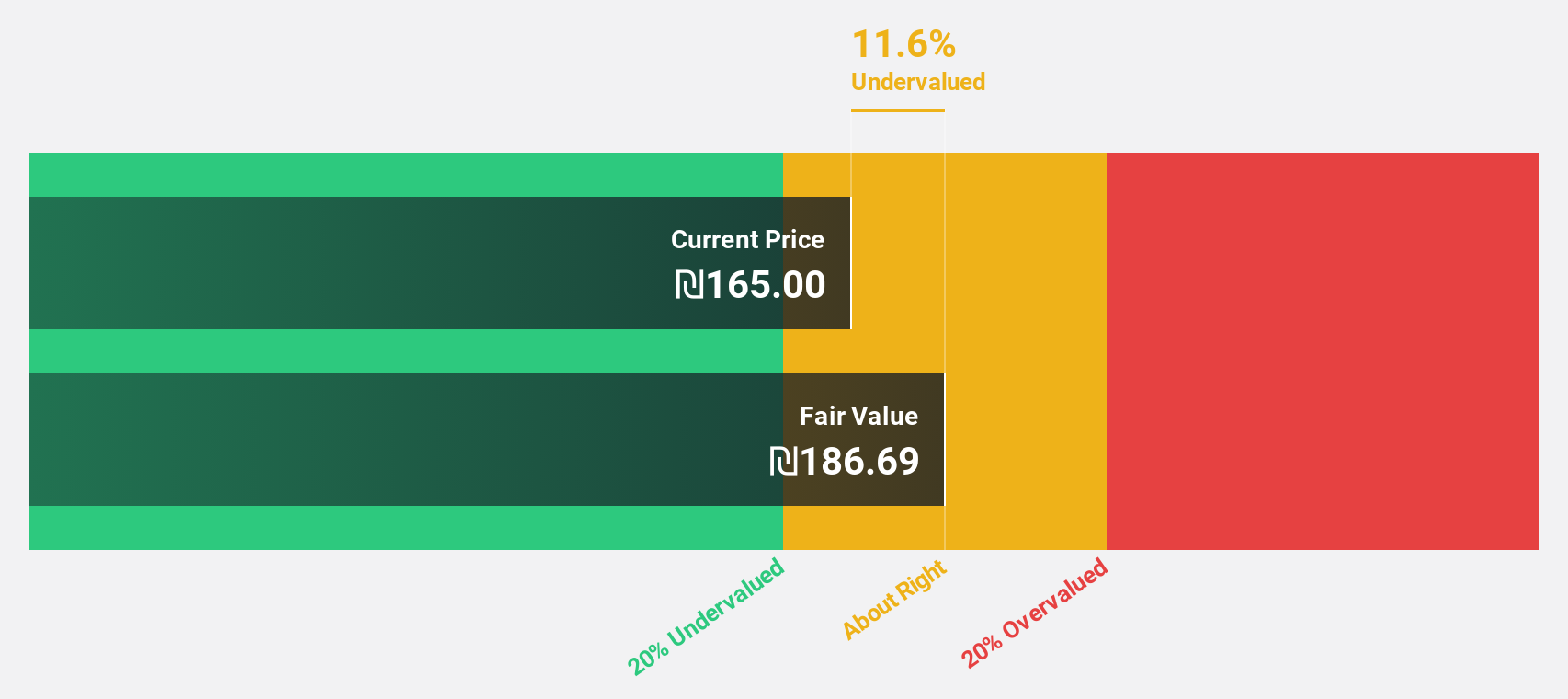

Nayax (TASE:NYAX)

Overview: Nayax Ltd. is a fintech company that provides system and payment platforms for retailers across the United States, Europe, the United Kingdom, Australia, Israel, and other regions worldwide with a market cap of ₪5.13 billion.

Operations: The company generates revenue primarily from its Internet Software and Services segment, totaling $291.65 million.

Estimated Discount To Fair Value: 12.7%

Nayax, trading at ₪141.6, is slightly undervalued compared to its fair value estimate of ₪162.13. The company anticipates robust revenue growth of 22.4% annually, surpassing the IL market average and projecting profitability within three years. Recent strategic moves include a partnership with SECO for IoT payment solutions and expanding retail offerings in Europe, enhancing its competitive position despite low forecasted return on equity of 12.4%.

- Our expertly prepared growth report on Nayax implies its future financial outlook may be stronger than recent results.

- Click here to discover the nuances of Nayax with our detailed financial health report.

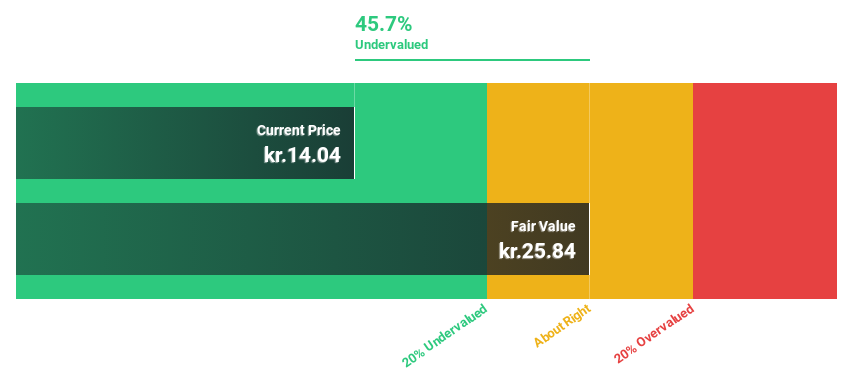

Cognor Holding (WSE:COG)

Overview: Cognor Holding S.A. is involved in the production and distribution of steel products across Poland, Czechia, Germany, and internationally, with a market capitalization of PLN1.20 billion.

Operations: Cognor Holding S.A. generates revenue from several segments, including Hsj (PLN1.07 billion), Jap (PLN122.18 million), Oms (PLN117.12 million), Ferrostal (PLN881.94 million), and Zlomrex Metal (PLN599.89 million).

Estimated Discount To Fair Value: 40.3%

Cognor Holding, priced at PLN6.99, is significantly undervalued compared to its fair value of PLN11.72, trading 40.3% below this estimate. Although revenue growth is projected at 14% annually—outpacing the Polish market's 4.9%—profitability is expected within three years with earnings forecasted to grow substantially by 70.06% per year. However, the company's return on equity remains low at a forecasted 1.4%, presenting a potential risk factor despite strong cash flow valuation metrics.

- The analysis detailed in our Cognor Holding growth report hints at robust future financial performance.

- Dive into the specifics of Cognor Holding here with our thorough financial health report.

Summing It All Up

- Gain an insight into the universe of 909 Undervalued Stocks Based On Cash Flows by clicking here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About WSE:COG

Cognor Holding

Engages in the production and distribution of steel products in Poland, Czechia, Germany, and internationally.

Mediocre balance sheet very low.

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|30.8% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|42.2% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$174.00|38.3% undervalued

AG

Community Contributor