Is It Too Late to Consider Ryanair After Its 48.7% One Year Surge?

Reviewed by Bailey Pemberton

- If you have been wondering whether Ryanair Holdings is still good value after its massive run up, you are not alone. That is exactly what we are going to unpack here.

- The stock has cooled slightly in the last week, down 2.9%, but it is still up 1.6% over 30 days, 44.3% year to date and a huge 48.7% over the last year, with a 124.5% gain over three years and 77.1% over five.

- Behind those moves, investors have been reacting to Ryanair's expanding route network and ongoing capacity shifts across European carriers, which are reshaping competitive dynamics and pricing power. Regulatory developments around sustainability, airport fees and slot allocation have also been in focus, as they could influence Ryanair's cost base and long term growth runway.

- Despite all that excitement, Ryanair currently scores just 1/6 on our valuation checks. Next we will break down what different valuation methods are really saying about the stock and, toward the end of the article, look at an even better way to think about its true value.

Ryanair Holdings scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

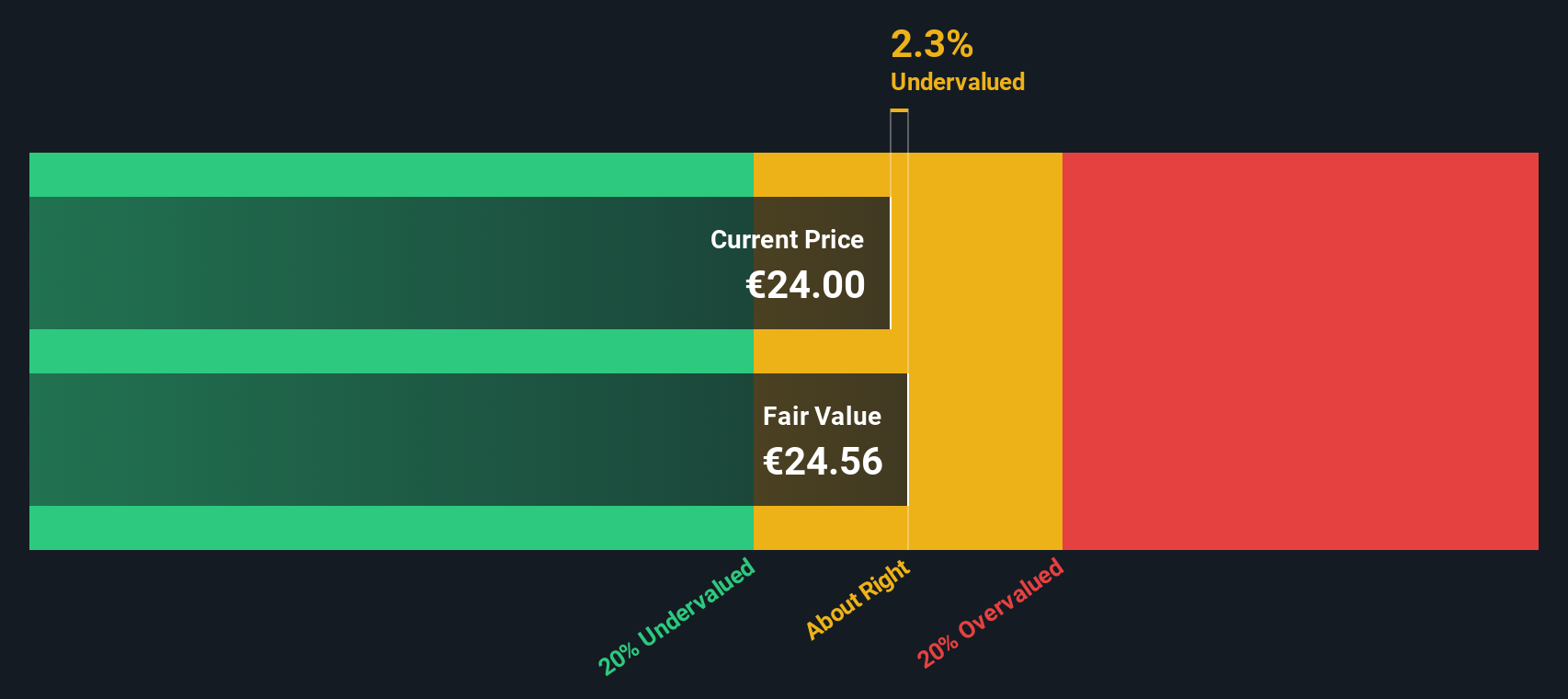

Approach 1: Ryanair Holdings Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, estimates what a business is worth by projecting the cash it can generate in the future and then discounting those cash flows back to today in € terms.

For Ryanair Holdings, the model starts from last twelve month free cash flow of about €1.8 billion and uses analyst forecasts for the next few years, then extrapolates further out. Under this 2 Stage Free Cash Flow to Equity approach, free cash flow is projected to rise to roughly €1.8 billion again by 2030, with a path that includes periods of higher and lower growth as capacity, pricing and costs evolve.

Pulling all those projected cash flows back to today gives an estimated intrinsic value of about €25.88 per share. That is roughly 7.1% above the current market price, implying the stock is trading slightly above what this cash flow based model suggests it is worth.

Result: ABOUT RIGHT

Ryanair Holdings is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

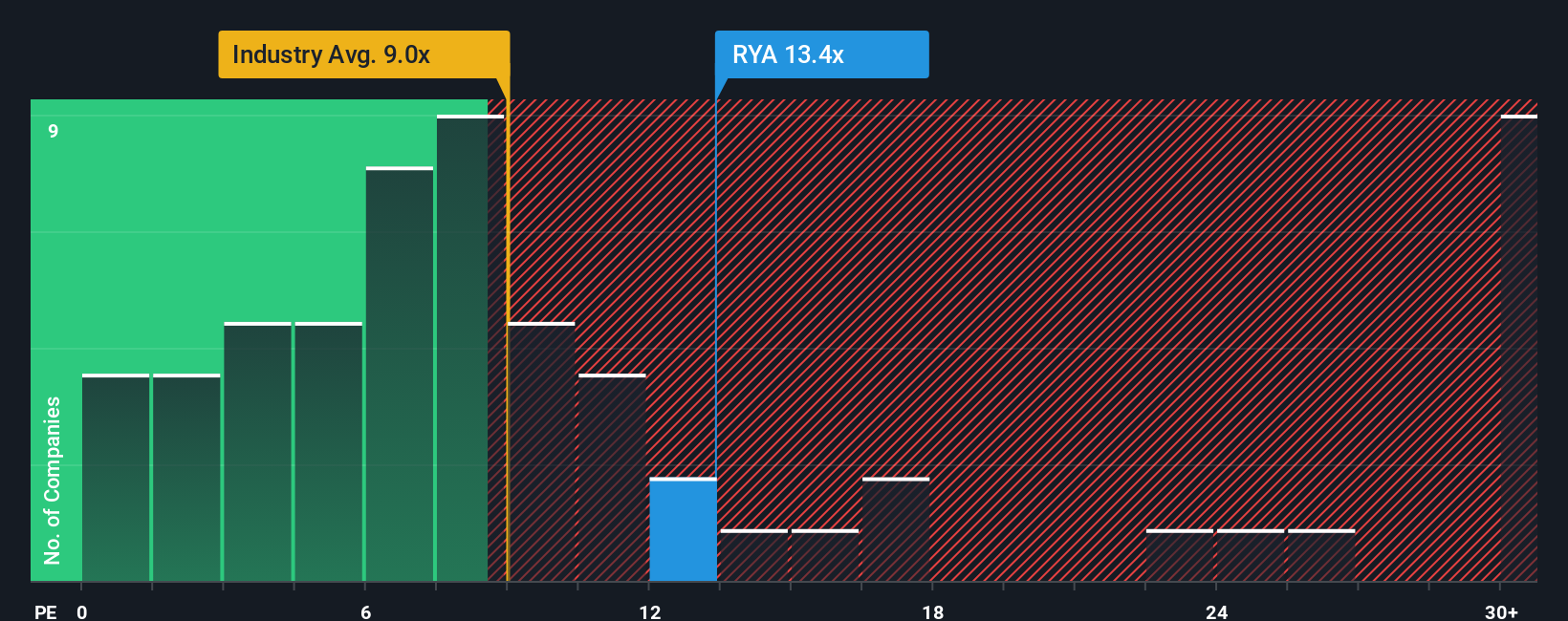

Approach 2: Ryanair Holdings Price vs Earnings

For profitable companies like Ryanair, the price to earnings, or PE, ratio is a useful way to gauge value because it links what investors pay today to the profits the business is already generating. In general, faster growth and lower perceived risk justify a higher PE, while slower growth or higher risk should come with a lower, more cautious multiple.

Ryanair currently trades on about 12.4x earnings, which is above the broader Airlines industry average of roughly 9.0x but below the peer group average of around 17.1x. At first glance, that suggests investors are willing to pay a premium to the typical airline, but not as much as for some better rated peers.

Simply Wall St also uses a Fair Ratio framework, which estimates what PE multiple would be reasonable for Ryanair given its earnings growth outlook, profitability, size, industry and specific risks. This tailored yardstick is more insightful than a simple comparison with peers or the industry, because it adjusts for the fact that not all airlines have the same growth runway, balance sheet strength or risk profile. On this basis, Ryanair’s current 12.4x PE sits meaningfully below where its Fair Ratio would be, pointing to a discount rather than excessive optimism.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1443 companies where insiders are betting big on explosive growth.

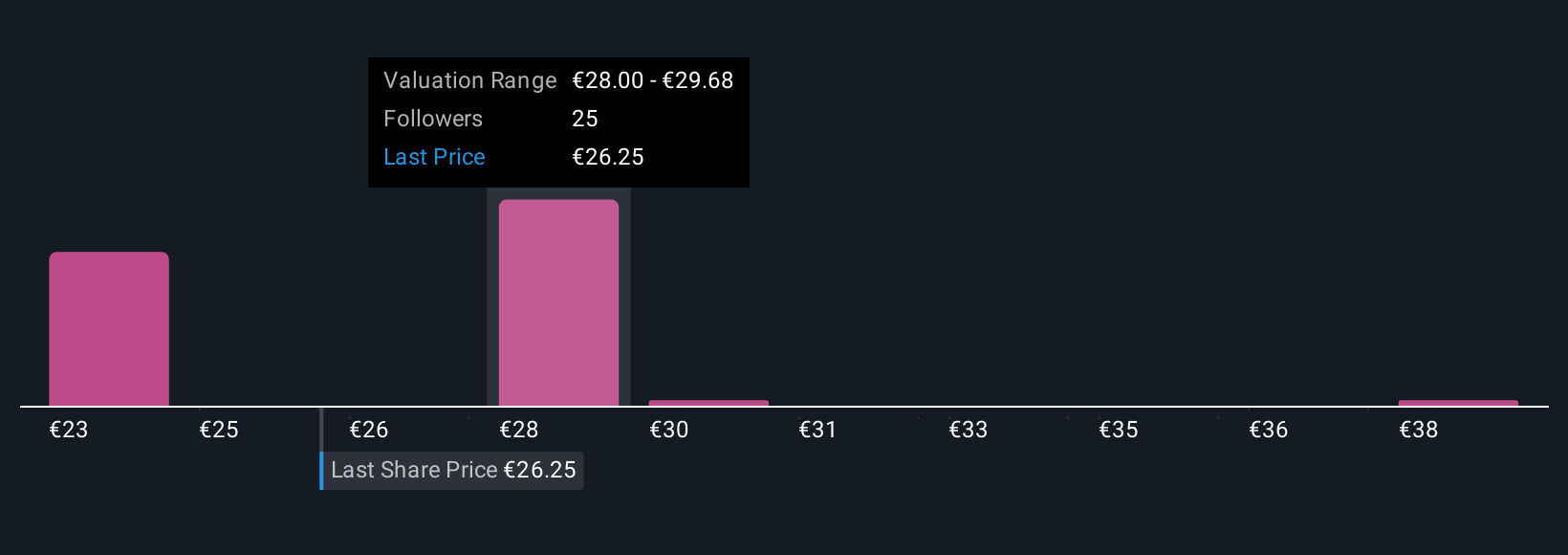

Upgrade Your Decision Making: Choose your Ryanair Holdings Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to connect your view of a company with the numbers behind it.

A Narrative is your story about a business, captured through your assumptions for fair value, future revenue growth, earnings and profit margins, so you are not just staring at ratios but explaining why they make sense.

On Simply Wall St, Narratives live in the Community page, where millions of investors use them to link a company’s story to a financial forecast and then to an estimated fair value that can be compared directly with today’s share price to help inform a decision on whether to buy, hold or sell.

Because Narratives update dynamically when fresh news, earnings or guidance arrives, they stay relevant. You can see, for example, one Ryanair Narrative that assumes robust post pandemic travel demand and higher pricing power leading to a much higher fair value, while another bakes in rising fuel costs and tougher regulation to arrive at a far lower estimate.

Do you think there's more to the story for Ryanair Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ISE:RYA

Ryanair Holdings

Provides scheduled-passenger airline services in Ireland, Italy, Spain, the United Kingdom, and internationally.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)