Shareholders May Not Be So Generous With Hang Tai Yue Group Holdings Limited's (HKG:8081) CEO Compensation And Here's Why

Key Insights

- Hang Tai Yue Group Holdings to hold its Annual General Meeting on 27th of June

- CEO Ching Yee Lam's total compensation includes salary of HK$1.21m

- The overall pay is comparable to the industry average

- Over the past three years, Hang Tai Yue Group Holdings' EPS grew by 60% and over the past three years, the total loss to shareholders 40%

Shareholders of Hang Tai Yue Group Holdings Limited (HKG:8081) will have been dismayed by the negative share price return over the last three years. Despite positive EPS growth in the past few years, the share price hasn't tracked the fundamental performance of the company. Shareholders may want to question the board on the future direction of the company at the upcoming AGM on 27th of June. They could also influence management through voting on resolutions such as executive remuneration. We think shareholders might be reluctant to increase compensation for the CEO at the moment, according to our analysis below.

View our latest analysis for Hang Tai Yue Group Holdings

Comparing Hang Tai Yue Group Holdings Limited's CEO Compensation With The Industry

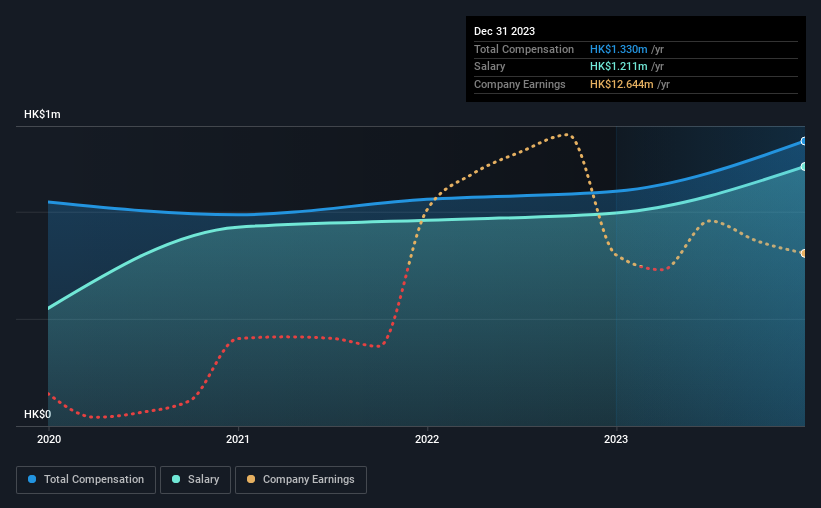

At the time of writing, our data shows that Hang Tai Yue Group Holdings Limited has a market capitalization of HK$242m, and reported total annual CEO compensation of HK$1.3m for the year to December 2023. That's a notable increase of 21% on last year. We note that the salary portion, which stands at HK$1.21m constitutes the majority of total compensation received by the CEO.

For comparison, other companies in the Hong Kong IT industry with market capitalizations below HK$1.6b, reported a median total CEO compensation of HK$1.2m. So it looks like Hang Tai Yue Group Holdings compensates Ching Yee Lam in line with the median for the industry.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | HK$1.2m | HK$994k | 91% |

| Other | HK$119k | HK$101k | 9% |

| Total Compensation | HK$1.3m | HK$1.1m | 100% |

On an industry level, roughly 85% of total compensation represents salary and 15% is other remuneration. There isn't a significant difference between Hang Tai Yue Group Holdings and the broader market, in terms of salary allocation in the overall compensation package. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

Hang Tai Yue Group Holdings Limited's Growth

Hang Tai Yue Group Holdings Limited's earnings per share (EPS) grew 60% per year over the last three years. In the last year, its revenue is down 52%.

Shareholders would be glad to know that the company has improved itself over the last few years. The lack of revenue growth isn't ideal, but it is the bottom line that counts most in business. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Hang Tai Yue Group Holdings Limited Been A Good Investment?

Few Hang Tai Yue Group Holdings Limited shareholders would feel satisfied with the return of -40% over three years. This suggests it would be unwise for the company to pay the CEO too generously.

In Summary...

Despite the growth in its earnings, the share price decline in the past three years is certainly concerning. The fact that the stock price hasn't grown along with earnings may indicate that other issues may be affecting that stock. Shareholders would probably be keen to find out what are the other factors could be weighing down the stock. The upcoming AGM will be a chance for shareholders to question the board on key matters, such as CEO remuneration or any other issues they might have and revisit their investment thesis with regards to the company.

CEO compensation can have a massive impact on performance, but it's just one element. We've identified 4 warning signs for Hang Tai Yue Group Holdings that investors should be aware of in a dynamic business environment.

Switching gears from Hang Tai Yue Group Holdings, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Hang Tai Yue Group Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:8081

Hang Tai Yue Group Holdings

An investment holding company, engages in the hospitality and related services, money lending, and assets investments businesses in Hong Kong and Australia.

Excellent balance sheet with low risk.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Hitit Bilgisayar Hizmetleri will achieve a 19.7% revenue boost in the next five years

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)