3 Stocks That May Be Trading Below Estimated Value In December 2024

Reviewed by Simply Wall St

As global markets continue to reach record highs, with indices such as the Dow Jones Industrial Average and S&P 500 Index soaring, investor sentiment remains buoyed by domestic policy developments and geopolitical events. Amidst this robust market environment, identifying stocks that may be trading below their estimated value can offer potential opportunities for investors seeking to capitalize on undervaluation in a landscape driven by economic stability and inflation control efforts.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Türkiye Sise Ve Cam Fabrikalari (IBSE:SISE) | TRY41.22 | TRY82.15 | 49.8% |

| PharmaResearch (KOSDAQ:A214450) | ₩213500.00 | ₩426006.27 | 49.9% |

| Giant Biogene Holding (SEHK:2367) | HK$48.30 | HK$96.27 | 49.8% |

| DAEDUCK ELECTRONICS (KOSE:A353200) | ₩14050.00 | ₩28039.12 | 49.9% |

| Power Root Berhad (KLSE:PWROOT) | MYR1.46 | MYR2.92 | 50% |

| Enento Group Oyj (HLSE:ENENTO) | €18.02 | €35.91 | 49.8% |

| EuroGroup Laminations (BIT:EGLA) | €2.726 | €5.42 | 49.7% |

| Fine Foods & Pharmaceuticals N.T.M (BIT:FF) | €7.84 | €15.60 | 49.7% |

| First Advantage (NasdaqGS:FA) | US$19.37 | US$38.63 | 49.9% |

| AeroVironment (NasdaqGS:AVAV) | US$203.19 | US$404.34 | 49.7% |

Underneath we present a selection of stocks filtered out by our screen.

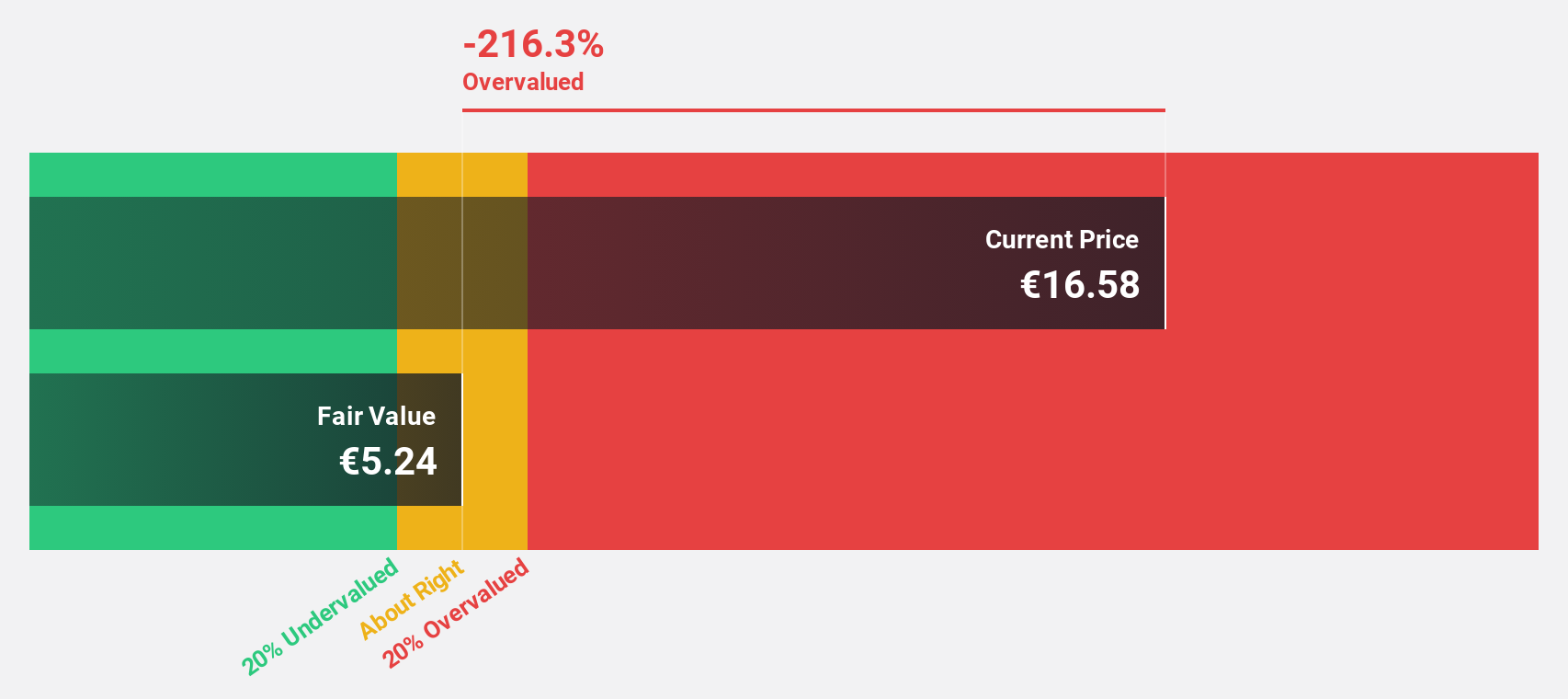

Fincantieri (BIT:FCT)

Overview: Fincantieri S.p.A. is a global player in the shipbuilding industry with a market capitalization of approximately €19 billion.

Operations: The company's revenue segments include Shipbuilding (€5.92 billion), Offshore and Specialized Vessels (€1.17 billion), and Equipment, Systems and Infrastructure (€1.21 billion).

Estimated Discount To Fair Value: 15.1%

Fincantieri S.p.A. is trading at €5.9, below its estimated fair value of €6.95, indicating it may be undervalued based on discounted cash flow analysis. Despite past shareholder dilution and modest historical earnings growth of 0.5% annually over five years, the company shows potential with forecasted annual profit growth above the market average and anticipated profitability within three years. Recent strategic alliances bolster its position in defense manufacturing, potentially enhancing future cash flows.

- Our growth report here indicates Fincantieri may be poised for an improving outlook.

- Navigate through the intricacies of Fincantieri with our comprehensive financial health report here.

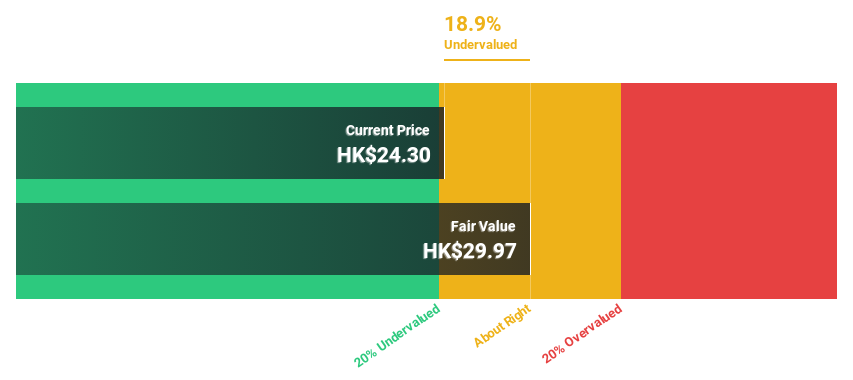

China Tobacco International (HK) (SEHK:6055)

Overview: China Tobacco International (HK) Company Limited operates in the tobacco industry, with a market capitalization of approximately HK$17.19 billion.

Operations: The company's revenue is derived from several segments, including the Tobacco Leaf Products Import Business at HK$8.43 billion, Tobacco Leaf Products Export Business at HK$1.82 billion, Cigarettes Export Business at HK$1.52 billion, Brazil Operation Business at HK$884.06 million, and New Tobacco Products Export Business at HK$139.60 million.

Estimated Discount To Fair Value: 17.3%

China Tobacco International (HK) is trading at HK$24.85, below its estimated fair value of HK$30.06, suggesting it could be undervalued based on cash flow analysis. Despite revenue growth projections of 11.1% annually being slower than desired, earnings are expected to grow faster than the Hong Kong market at 12.3% per year. However, debt coverage by operating cash flow remains a concern and may impact financial stability moving forward.

- Our earnings growth report unveils the potential for significant increases in China Tobacco International (HK)'s future results.

- Dive into the specifics of China Tobacco International (HK) here with our thorough financial health report.

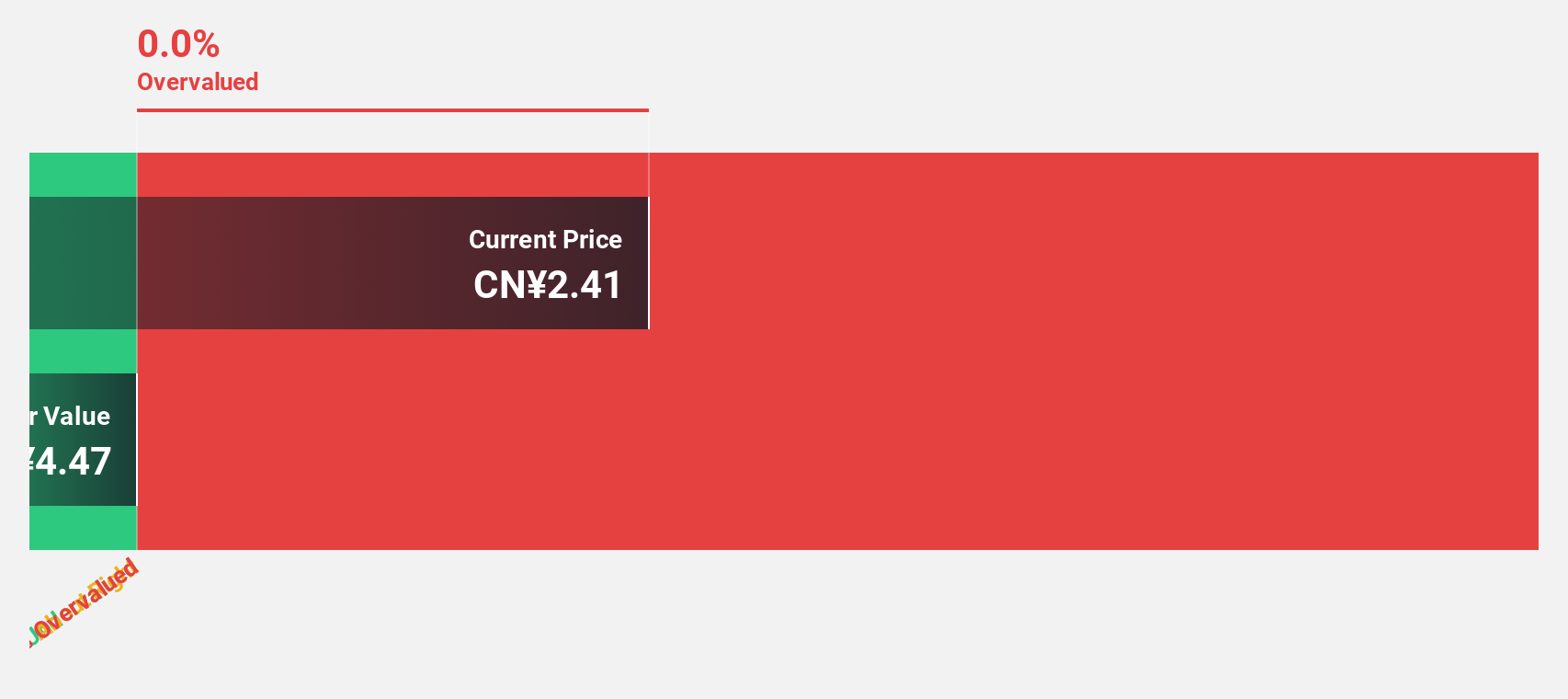

Yangmei ChemicalLtd (SHSE:600691)

Overview: Yangmei Chemical Co., Ltd. is involved in the research, development, production, and sale of chemical products in China with a market capitalization of CN¥5.96 billion.

Operations: Yangmei Chemical Co., Ltd. generates revenue through its activities in the research, development, production, and sale of chemical products within China.

Estimated Discount To Fair Value: 25.3%

Yangmei Chemical Ltd. is trading at CN¥2.51, significantly below its estimated fair value of CN¥3.36, indicating potential undervaluation based on cash flow analysis. Despite a challenging year with revenue dropping to CN¥7.92 billion and a net loss of CN¥387.08 million for the first nine months of 2024, the company is expected to achieve profitability within three years with earnings growing over 100% annually and revenues increasing faster than the Chinese market average.

- Our comprehensive growth report raises the possibility that Yangmei ChemicalLtd is poised for substantial financial growth.

- Take a closer look at Yangmei ChemicalLtd's balance sheet health here in our report.

Make It Happen

- Reveal the 900 hidden gems among our Undervalued Stocks Based On Cash Flows screener with a single click here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About BIT:FCT

Reasonable growth potential and fair value.