- Hong Kong

- /

- Specialty Stores

- /

- SEHK:1020

Cybernaut International Holdings Company Limited's (HKG:1020) Business Is Trailing The Industry But Its Shares Aren't

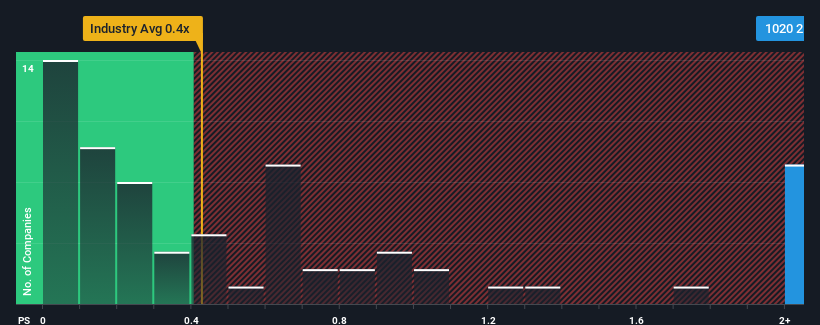

When you see that almost half of the companies in the Specialty Retail industry in Hong Kong have price-to-sales ratios (or "P/S") below 0.4x, Cybernaut International Holdings Company Limited (HKG:1020) looks to be giving off some sell signals with its 2.4x P/S ratio. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for Cybernaut International Holdings

How Has Cybernaut International Holdings Performed Recently?

Cybernaut International Holdings certainly has been doing a great job lately as it's been growing its revenue at a really rapid pace. Perhaps the market is expecting future revenue performance to outperform the wider market, which has seemingly got people interested in the stock. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Although there are no analyst estimates available for Cybernaut International Holdings, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.Is There Enough Revenue Growth Forecasted For Cybernaut International Holdings?

The only time you'd be truly comfortable seeing a P/S as high as Cybernaut International Holdings' is when the company's growth is on track to outshine the industry.

Retrospectively, the last year delivered an exceptional 76% gain to the company's top line. However, this wasn't enough as the latest three year period has seen the company endure a nasty 44% drop in revenue in aggregate. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

In contrast to the company, the rest of the industry is expected to grow by 32% over the next year, which really puts the company's recent medium-term revenue decline into perspective.

With this in mind, we find it worrying that Cybernaut International Holdings' P/S exceeds that of its industry peers. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. There's a very good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the recent negative growth rates.

What We Can Learn From Cybernaut International Holdings' P/S?

We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of Cybernaut International Holdings revealed its shrinking revenue over the medium-term isn't resulting in a P/S as low as we expected, given the industry is set to grow. With a revenue decline on investors' minds, the likelihood of a souring sentiment is quite high which could send the P/S back in line with what we'd expect. If recent medium-term revenue trends continue, it will place shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

Before you take the next step, you should know about the 1 warning sign for Cybernaut International Holdings that we have uncovered.

If these risks are making you reconsider your opinion on Cybernaut International Holdings, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1020

Cybernaut International Holdings

An investment holding company, provides e-commerce solutions and related support services in the People’s Republic of China, Europe, North America, and Hong Kong.

Adequate balance sheet minimal.

Similar Companies

Market Insights

Community Narratives